Strategies with inherent tax efficiencies may help investors diversify sources of income and potentially keep more of what they earn.

KEY TAKEAWAYS

- Income-efficient asset classes can offer solutions for tax-conscious investors

REITs and preferred securities both offer the potential for attractive income, with their generally above-average yields enhanced by inherent tax advantages. - REITs offer three aspects of tax-advantaged income

REITs have a history of attractive distributions before and after taxes, benefiting from a 20% tax deduction on REIT income and favorable tax treatment of capital gains and return of capital. - Preferred securities offer high current income with qualified dividend income (QDI) benefits

Preferreds tend to pay high income rates due to subordination, with most distributions treated as dividends rather than interest, taxed at a top rate of 20%.

Introduction

REITs and preferred securities answer the call for attractive, tax-efficient income

Investment solutions for tax-conscious investors

As investors consider solutions to their income needs, identifying asset classes that offer tax advantages can be a powerful part of the equation.

Cohen & Steers provides access to specialized asset classes that offer the potential for attractive income, with inherent tax advantages to help investors keep more of the income they earn—both today and under any changes in tax policy that could occur in the next few years.

REITs

- Designed for efficient delivery of rental income to investors, taxed only once (at the shareholder level)

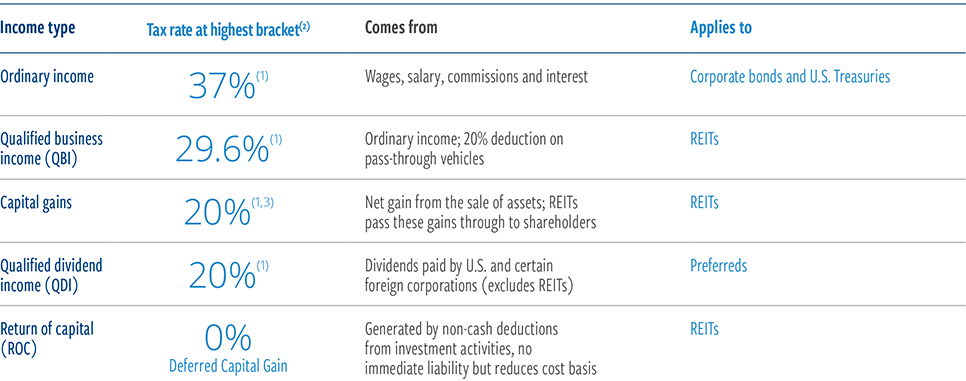

- 20% deduction on ordinary income distributions from REITs as qualified business income (QBI), reducing the top tax rate from 37% to 29.6%(1)

- Three aspects of tax-advantaged income: QBI, capital gains and return of capital

Preferred Securities

- Historically offer some of the highest income rates within investment- grade fixed income, from generally high-quality issuers

- Distributions mostly treated as qualified dividend income (QDI) rather than interest, taxed at a top rate of 20% vs. 37%(1)

- A wide range of security structures, including many with low durations, that may reduce sensitivity to changing interest rates

At December 31, 2024. Source: Internal Revenue Service, Cohen & Steers.

(1) Additional 3.8% Medicare surcharge applies for certain U.S. taxpayers. (2) As of 2024 tax year, taxable income of more than $609,350 (individuals) or $731,200 (married filing jointly). (3) A portion may be taxed at 25%. See page 7 for additional disclosures.

REITs offer three aspects of tax-advantaged income

REITs’ above-average dividend yields have come with tax advantages unavailable to broader equities

Single taxation and a history of high dividends

U.S. REITs are required to distribute at least 90% of their taxable income to shareholders and are exempt from paying corporate taxes if they distribute 100% of their taxable income. This single taxation and distribution requirement is why REITs have historically paid higher dividends than most other companies.

REIT income distributions get a 20% tax break

REIT income is generated mostly from property rents and historically makes up about 60% of overall U.S. REIT distributions. The income is considered qualified business income (QBI) and is entitled to a 20% deduction. This means that for every dollar of income, investors pay tax on only 80 cents of income, reducing the top tax rate from 37% to 29.6%.

Complementary tax-efficient income streams

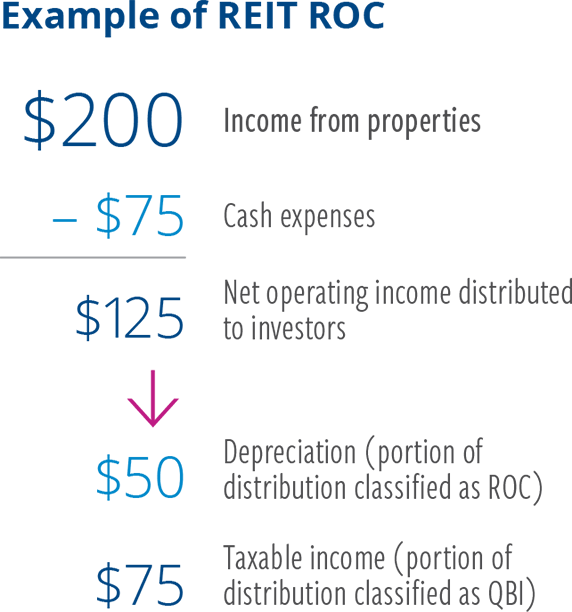

In addition to QBI, REITs typically distribute the net gains from property sales as capital gains, taxed mostly at a top rate of 20%, while a portion is taxed at a top rate of 25%. Most REITs pay out all their net operating income to shareholders. However, they generally claim investment-related non-cash expenses, such as depreciation and amortization on their real estate assets, which reduces their taxable income. This difference in a REIT’s distributions between net operating and taxable income is considered return of capital (ROC). Any tax liability from ROC is deferred until the time of sale, when it lowers the investor’s cost basis in the investment.

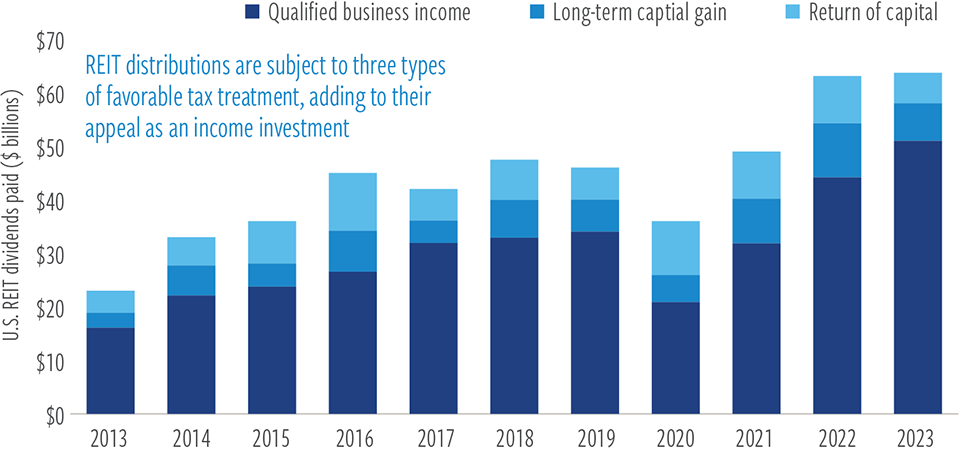

EXHIBIT 1

REIT dividends have been tied to underlying cash flows

Aggregate taxation of REIT common share dividends

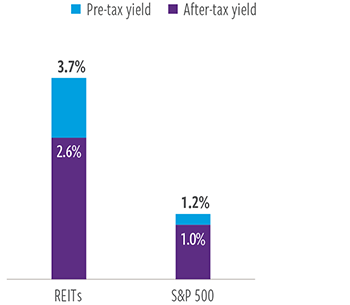

EXHIBIT 2

REITs maintain their tax-advantaged status with high payouts

% Current yield

At March 31, 2025. Source: REIT.com, Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. The information presented above does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. An investor cannot invest directly in an index and index performance does not reflect the deductions of any fees, expenses or taxes. The views and opinions are as of the date of publication and are subject to change without notice. See page 7 for index associations, definitions and additional disclosures.

Potential impact of policy changes on REITs

Example of REIT ROC

REITs likely to benefit from stimulus. We believe the vast amount of stimulus spending implemented in recent years stands to support economic growth and, by extension, real estate demand. Stimulus can provide a lift for the economy, small businesses and consumers, and potentially benefit a range of REIT sectors, particularly industrial, retail and self storage. Infrastructure spending, meanwhile, could have a meaningful impact on demand for most property types.

Higher corporate taxes a non-event. Just as lower corporate tax rates in 2017 had no impact on REITs (which are not subject to taxes), higher corporate rates would likely have little or no effect on the asset class.

Increased individual tax rates would be modestly negative. REIT shareholders pay taxes on income distributions according to their individual tax rate, which at some point could rise for top earners from 37%. Additionally, the 20% pass-through deduction on QBI, which applies to REIT dividend income, could be adjusted to create parity with a higher corporate tax rate, and could be modified or eliminated for high-income taxpayers.

“Like-kind” tax exchanges may be eliminated. Should real estate investors no longer be allowed to defer capital gains if proceeds of property sales are reinvested in other assets, it could negatively impact transaction volumes, reducing REITs’ ability to improve their portfolios. However, we expect significant pushback from industry groups on such a proposal, and previous attempts have been unsuccessful.

Preferred securities offer high current income potential with QDI benefits, including low-duration preferreds with less rate risk

Preferreds offer higher yields than comparable fixed income categories, along with the potential for reduced interest-rate risk

High, tax-advantaged income

Preferred securities are issued mostly by high-quality issuers, but due to their subordinated position in the capital structure, they often pay higher income rates than similarly rated bonds. Many of these distributions are classified as qualified dividend income (QDI) and taxed at a top rate of 20%, compared to 37% for ordinary interest income (plus a 3.8% Medicare surcharge). This combination of high coupons and tax-advantaged treatment creates the potential for attractive after-tax income relative to other fixed income categories. It also makes preferreds a compelling complement to municipal bonds.

Using current index yields as proxies, a hypothetical $1 million investment in preferreds would potentially generate $66,000 per year in pre-tax income. Assuming that 65% of the income generated is QDI eligible, that translates to $46,700 per year after taxes for investors in the top tax bracket—saving $7,300 in taxes, compared to the same income fully treated as interest.

The current relative yield advantage of preferreds partly reflects ample QDI available in the asset class

Low-duration preferreds may help to negotiate interest-rate cycles

Recent rate increases in money markets and short-term Treasurys have drawn interest from investors, many of whom fail to anticipate the taxable nature of that income. Short-duration preferreds, while not a cash equivalent, are often thought of as a conservative step into the low-duration market with tax advantaged benefits.

Beyond that, the fixed-to-floating rate structures of many preferreds typically reset with changes in short-term rates, mitigating investors’ exposure to changes in interest rates. Thanks to these reset structures, more than 75% of the preferred market has durations under five years. Low-duration preferreds also typically represent different sectors than what investors get from other low-duration fixed income securities, helping to diversify investors’ portfolios.

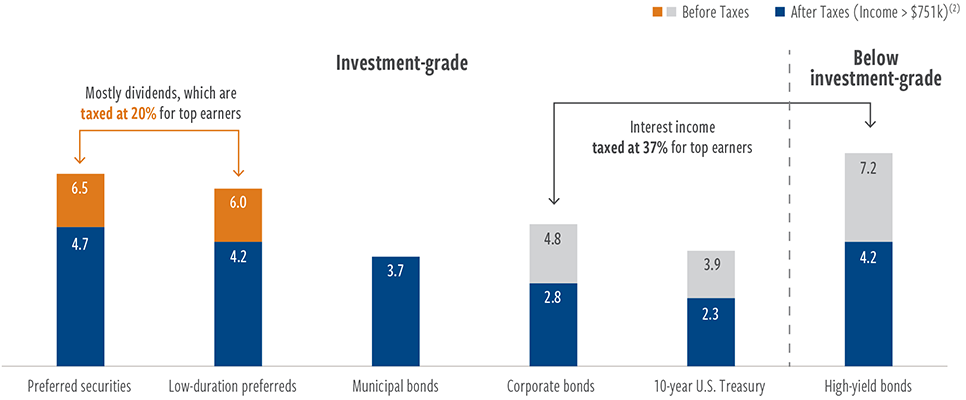

EXHIBIT 3

Preferreds can offer tax-advantaged income for U.S. investors

Fixed income yields(1)

At March 31, 2025. Source: Cohen & Steers, ICE BofA.

Data represents past performance, which is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes. Debt securities including preferred securities, corporate bonds, municipal bonds and high yield bonds generally present various risks, including interest rate risk, credit risk, call risk, prepayment and extension risk, convertible securities risk, and liquidity risk. Index comparisons have limitations as volatility and other characteristics may differ from a particular investment. The above is not intended to serve as tax advice. Investors should consult with their respective tax advisors prior to making an investment. (1) Yields shown on a yield-to-maturity basis. (2) Assumes taxation at the highest marginal U.S. Federal income tax rates of 37% for taxable interest income and 20% for QDI, with an additional 3.8% Medicare surcharge on all tax rates. After tax calculations assumes preferred securities income is taxed at the respective qualified dividend rate and marginal tax rate on a 65/35 blended basis. All other securities reflect full taxation at the respective marginal rates based on income. Note: State and local taxes are not included in these calculations. See page 7 for index associations and definitions and additional disclosures, including after-tax assumptions.

Conclusion

Asset classes with inherent tax efficiencies, such as REITs and preferred securities, have the potential to produce higher-than-average income and returns compared to the broad equities market and traditional fixed income securities, respectively. They can also expand portfolio diversification to help enhance overall risk-adjusted return potential, thereby complementing investments such as municipal bonds in tax-efficient allocations for high after-tax income.

Cohen & Steers is a leading specialist in listed real assets and alternative income solutions, with a long track record of strong investment performance and an experienced, global team focused on delivering results for our clients. Contact your investment professional today to learn more about tax-smart income solutions from Cohen & Steers.

Index definitions / important disclosures

This material is for informational purposes, and reflects prevailing conditions and our judgment as of this date, which are subject to change. There is no guarantee that any market forecast set forth in this presentation will be realized.

This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this presentation to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment.

Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes. Corporate Bonds: ICE BofA Corporate Master Index (Credit quality: A-) tracks the performance of U.S. dollar-denominated investment-grade corporate debt publicly issued in the U.S. domestic market. Corporate bonds are taxed at 100% ordinary income. Equities: The S&P 500 Index is an unmanaged index of 500 large-capitalization stocks that is frequently used as a general measure of U.S. stock market performance. Equities’ after-tax calculations assume income is 100% QDI. High Yield Bonds: ICE BofA High Yield Master Index (Credit quality: B+) tracks the performance of U.S. dollar-denominated below-investment-grade corporate debt publicly issued in the U.S. domestic market. Low Duration Preferred Securities: ICE BofA 8% Constrained Developed Markets Low Duration Capital Securities Custom Index (Credit quality: BBB-) tracks the performance of select U.S. dollar-denominated fixed and floating-rate preferred, corporate and contingent capital securities, with a remaining term to final maturity of one year or more, but less than five years. Preferred Securities after-tax calculations assume preferred securities income is taxed at the respective qualified dividend rate and marginal tax rate on a 65/35 blended basis. Municipal Bonds: ICE BofA Municipal Master Index (Credit quality: AA-) tracks the performance of U.S. dollar-denominated investment-grade tax-exempt debt publicly issued by U.S. states and territories, and their political subdivisions, in the U.S. domestic market. Municipal Bonds’ income is exempt from federal taxation. Preferred Securities: ICE BofA Fixed Rate Preferred Securities Index (Credit quality: BBB) tracks the performance of fixed-rate U.S. dollar-denominated preferred securities issued in the U.S. domestic market. Preferred Securities after-tax calculations assume preferred securities income is taxed at the respective qualified dividend rate and marginal tax rate on a 65/35 blended basis. U.S. REITs: The FTSE NAREIT All Equity REITs Index contains all tax-qualified REITs with more than 50% of total assets in qualifying real estate assets other than mortgages secured by real property that also meet minimum size and liquidity criteria. U.S. REITs’ after-tax calculations assume income is 60% QBI, 20% capital gains, 20% ROC. 10-year U.S. Treasury: The 10-Year Treasury note is a debt obligation issued by the United States government that matures in 10 years. Treasury bonds are fully taxable at the federal level at the taxable interest income rate of 37%.

Risks of investing in real estate securities. The risks of investing in real estate securities are similar to those associated with direct investments in real estate, including falling property values due to increasing vacancies or declining rents resulting from economic, legal, political or technological developments, lack of liquidity, limited diversification and sensitivity to certain economic factors such as interest rate changes and market recessions. Foreign securities involve special risks, including currency fluctuations, lower liquidity, political and economic uncertainties, and differences in accounting standards. Some international securities may represent small- and medium-sized companies, which may be more susceptible to price volatility and less liquidity than larger companies.

Risks of investing in preferred securities. An investment in a preferred strategy is subject to investment risk, including the possible loss of the entire principal amount that you invest. The value of these securities, like other investments, may move up or down, sometimes rapidly and unpredictably. Our preferred strategies may invest in below-investment-grade securities and unrated securities judged to be below investment-grade by the Advisor. Below- investment-grade securities or equivalent unrated securities generally involve greater volatility of price and risk of loss of income and principal, and may be more susceptible to real or perceived adverse economic and competitive industry conditions than higher-grade securities. The strategies’ benchmarks do not contain below investment-grade securities.

Duration Risk. Duration is a mathematical calculation of the average life of a fixed-income or preferred security that serves as a measure of the security’s price risk to changes in interest rates (or yields). Securities with longer durations tend to be more sensitive to interest rate (or yield) changes than securities with shorter durations. Duration differs from maturity in that it considers potential changes to interest rates, and a security’s coupon payments, yield, price and par value and call features, in addition to the amount of time until the security matures. Various techniques may be used to shorten or lengthen the Fund’s duration. The duration of a security will be expected to change over time with changes in market factors and time to maturity.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority of the United Kingdom (FRN 458459). Cohen & Steers Asia Limited is authorized and registered with the Hong Kong Securities and Futures Commission (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319).