Preferred securities and private real estate are two allocations to consider, in our view.

KEY TAKEAWAYS:

- Private credit is beginning to show some cracks, with concerns surfacing about deteriorating underwriting standards, liquidity constraints, loan extensions or adjustments, and several high-profile defaults.

- As total returns drop in private credit, investors may question whether they are being compensated for the risks of the asset class, especially compared with allocations that have already repriced or where yields have normalized.

- Investors seeking tax-advantaged income can consider preferred securities, which offer high yield from quality issuers, while private real estate prices have bottomed, creating an unusual opportunity to access the long-term benefits of private real estate.

Private credit—now valued at more than $3 trillion, ten times its 2009 size—is beginning to show some cracks.

Concerns are surfacing about deteriorating underwriting standards, liquidity constraints, loan extensions or adjustments, and several high-profile defaults that investors worry are canaries in the coal mine.

One of the industry’s largest public funds that invests in private credit recently cut its net asset value by 19%. It’s estimated that around one of every ten private credit loans is being paid by payments in kind (PIK), which allows a borrower to skip a payment and instead add the unpaid interest to the principal balance. And investor redemptions climbed in the fourth quarter last year.

As total returns drop in private credit, investors may question whether they are being compensated for the risks of the asset class, especially compared with allocations that have already repriced or where yields have normalized.

Preferred securities and private real estate are two allocations to consider, in our view, as investors seek tax-efficient income, total returns and asset classes well positioned for the current market cycle.

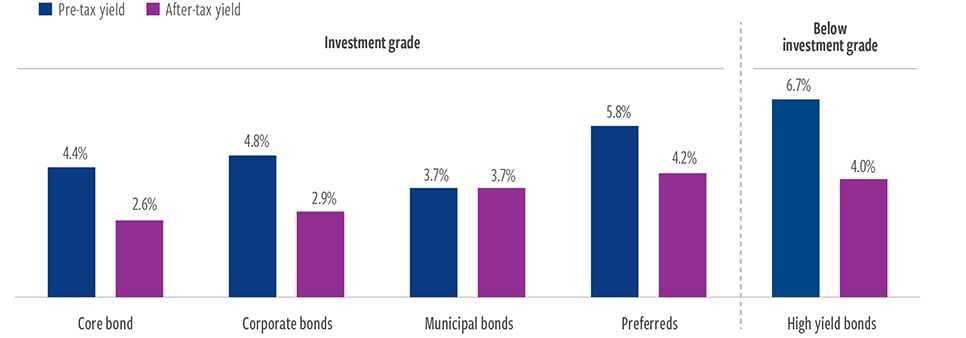

Preferred securities are an often underutilized investment choice for fixed income allocations, but they can be a valuable tool, potentially contributing higher income, solid risk-adjusted returns, and broader portfolio diversification from high quality issuers. Preferred securities were the top-performing fixed income category in 2025 and currently offer 6–7% yields from investment-grade issuers.

And while private credit is still adjusting to the higher-rate regime, commercial real estate prices are in the early stages of recovery. The bottoming that occurred in private real estate has created an entry point for investors into an asset class that has historically provided steady income, capital appreciation and tax efficiency—at a time when other allocations are becoming less and less attractive.

Private credit tested by new market regime

Private credit was buoyed by both supply and demand in the wake of the global financial crisis (GFC).

Demand was high for higher-yielding assets through the extended period of near- zero rates following the GFC. At the same time, banks, restricted by post-GFC regulations, pulled back from lending. Private credit stepped in to fill the supply gap for loans deemed too large, too risky or overly complex for banks or too small for other lenders while offering faster, less stringent underwriting.

Market dynamics have now shifted, however. Following the 10 rate hikes in 2022 and 2023, fixed income yields normalized for traditional fixed income (Treasuries, investment-grade bonds, high-yield debt, preferred securities). Fixed income spreads have tightened across the board, but they’ve notably compressed for private credit with more capital chasing fewer deals and more competition from public markets.

The result is that spreads have narrowed while risks have risen.

The Wall Street Journal (WSJ) reports that total returns for the largest private credit funds averaged 6.2% in the first nine months of 2025, down from same-period total returns of 8.8% and 11.4% in 2024 and 2023, respectively.

The headlines raising alarms on private credit are piling up: “When you see one cockroach, there are probably more” (Jamie Dimon); “The private credit party turns ugly” (WSJ); “Wall Street braced for a private credit meltdown” (CNBC).

Media may lean toward hyperbole, but these headlines are grounded in documented developments. Any doubt on the asset class directly undermines confidence, particularly given that private credit was marketed as a stable, high- yielding alternative to public markets.

Private credit at its current scale has also never been tested over a full market cycle.

Outflows are increasing as risks rise and spreads tighten. Further, with the democratization of private credit through new vehicles for retail investors, assets in private credit will be less sticky.

Institutional investors have historically invested in credit through funds without liquidity options, which created more stable pools of capital. Retail investors by contrast tend to flee in the face of negative headlines. Continued outflows will exacerbate the operational challenges these funds face.

Preferred securities offer high yield from quality issuers

Preferred securities can help bridge the gap between investment-grade bonds and high yield debt—often delivering much of the return boost of high yield, but with historically lower volatility due to issuance concentrated in regulated, investment- grade sectors such as banks, insurers and defensive utilities.

As the Federal Reserve continues its rate-cutting cycle, preferred performance should benefit from renewed demand for quality, duration and higher-yielding fixed income alternatives. And since preferred dividends are often tax advantaged, investors keep more of their earnings (Exhibit 1).

Issuers of preferred securities are mainly large, highly regulated institutions and/or companies with high, stable and transparent cash flows—such as banks, insurance companies, utilities, pipeline companies and real estate investment trusts (REITs).

Preferreds have also been tested across full market cycles and have proven resilient. One 40-year study from S&P Global found that BBB/BB+ rated securities from global financial services companies (the typical ratings and the main issuers of preferreds) historically have had default rates under 1%.

EXHIBIT 1

Preferreds yields are among the highest in fixed income

Pre-and post-tax yields of fixed income asset classes

At September 30, 2025. Source: ICE BofA, Bloomberg, Cohen & Steers.

Past performance is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. After-tax yields assumes taxation at the highest marginal U.S. Federal income tax rate of 37% for taxable interest income and 20% for qualified dividend income (QDI), with an additional 3.8% Medicare surcharge on all tax rates. After tax calculation assumes preferred securities income is taxed at the respective qualified dividend rate and marginal tax rate on a 75/25 blended basis; all other securities reflect full taxation at the respective marginal rates based on income. Core bonds represented by the Bloomberg U.S. Aggregate Bond Index. Corporate bonds represented by the ICE BofA U.S. Corporate Index. Municipal bonds represented by the ICE BofA U.S. Municipal Securities Index. High yield bonds represented by the ICE BofA U.S. High Yield Index. Preferreds represented by ICE BofA U.S. Institutional Capital Securities Index. See endnotes for index definitions and additional disclosures.

Banks, the largest preferred issuer segment, have perhaps never been in better shape: Capital reached record levels in 2025, supported by solid earnings, which we believe provides a cushion against future loan losses and may provide a credit tailwind for the industry.

Preferred securities have shown diversifying correlations with both equities and other fixed income asset classes, which is important in today’s markets because stocks and bonds have grown increasingly correlated. This is partly because banks and insurance companies are typically not well represented in other fixed income strategies (such as high-yield bonds). Low correlations with other asset classes provide strong support for preferred securities as a portfolio diversifier.

Private real estate prices have bottomed

The higher-rate regime and a high cost of capital have been priced into private real estate, which declined an average of 20%, peak to trough, alongside the rate increases that began in 2022. That stands in contrast to private credit and private equity.

U.S. private real estate, as measured by the NCREIF-ODCE index, has now posted five consecutive quarters of positive returns. This followed negative returns for seven straight quarters, dating back to the end of 2022.

At the same time, inflation on materials and labor, combined with higher borrowing costs, has slowed new construction, which should lead to accelerating rent growth for existing properties. Income from in-place rents that are poised to grow due to lack of new construction may offer an attractive alternative to investors worried about risks in private credit.

The reset in prices, supply/demand dynamics, and the relatively favorable profile of commercial real estate (compared with alternative allocations) are compelling. And that creates an unusual opportunity to access the long-term benefits of private real estate, in our view.

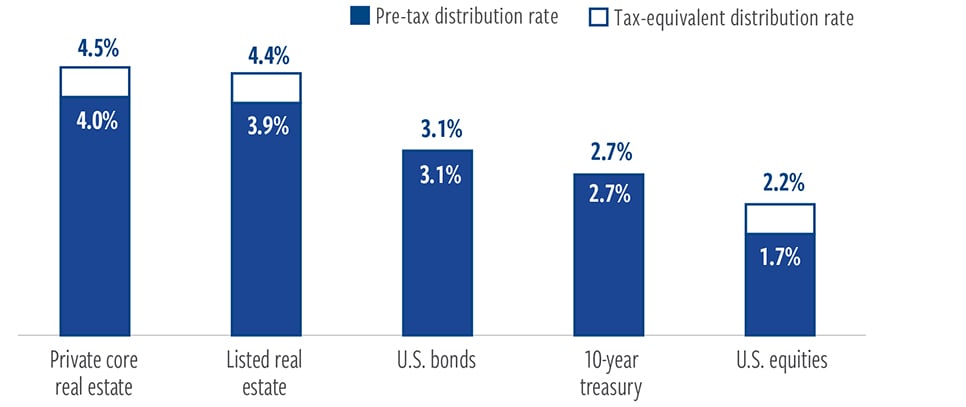

Private real estate, especially when combined with listed real estate allocations, can and should help investors diversify, create more resilient portfolios, and improve Sharpe ratios given more attractive valuations and greater inflation sensitivity. The asset class gives investors the opportunity for high tax-efficient yields driven by REIT taxation, pass-through depreciation deemed return of capital, and potential estate tax benefits (Exhibit 2).

Private real estate also has historically had low correlations to traditional asset classes, which matters at a time when investors are seeking greater diversification, and given that stock and bond valuations are historically high.

EXHIBIT 2

Reliable source of income with potential tax advantages

Average 10-year distribution rates(a)

At December 31, 2025. Source: Cohen & Steers, Morningstar.

Data quoted represents past performance, which is no guarantee of future results. Private core real estate: NCREIF Fund Index –Open End Diversified Core Equity (NFI-ODCE); Listed real estate: FTSE Nareit All Equity REITs Index; U.S. equities: S&P 500 Index; U.S. bonds: Barclays U.S. Aggregate Bond Index; 10-year treasury: Barclays U.S. Treasury 5-7 Yr Index. (a) Average distribution rate calculated on a quarterly frequency for the trailing 10-year period ending December 31, 2022. After-tax calculation assumes taxation at the highest marginal tax rate for each security income type. Assumes all real estate securities yield is eligible for the 20% Qualified Business Income deduction. Does not include the Medicare surcharge of 3.8% nor state and local taxes.

ABOUT THE AUTHORS

Joseph Harvey, Chief Executive Officer of Cohen & Steers and a director for the firm and its mutual funds.

Index definitions and important disclosures

Data quoted represents past performance, which is no guarantee of future results. The information presented does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this video will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

This material should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this video to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Risks of investing in private real estate. Private real estate investments are illiquid and susceptible to economic slowdowns or recessions and industry cycles, which could lead to financial losses and a decrease in revenues, net income and assets. Lack of liquidity in the private real estate market makes valuing underlying assets difficult. Appraisal values may vary substantially from a price at which an investment in real estate may actually be sold.

Risks of investing in real estate securities. The risks of investing in real estate securities are similar to those associated with direct investments in real estate, including falling property values due to increasing vacancies; declining rents resulting from economic, legal, political or technological developments; lack of liquidity; lack of availability of financing; limited diversification; sensitivity to certain economic factors, such as interest rate changes and market recessions; and changes in supply of or demand for similar properties in a given market. No representation or warranty is made as to the efficacy of any particular strategy or fund or the actual returns that may be achieved.

Risks of Investing in Preferred Securities. An investment in a preferred strategy is subject to investment risk, including the possible loss of the entire principal amount that you invest. The value of these securities, like other investments, may move up or down, sometimes rapidly and unpredictably. Our preferred strategies may invest in below-investment-grade securities and unrated securities judged to be below investment grade by the advisor. Below-investment-grade securities or equivalent unrated securities generally involve greater volatility of price and risk of loss of income and principal, and may be more susceptible to real or perceived adverse economic and competitive industry conditions than higher-grade securities.

Contingent capital securities (CoCos). CoCos are debt or preferred securities with loss absorption characteristics built into the terms of the security, for example a mandatory conversion into common stock of the issuer under certain circumstances, such as the issuer’s capital ratio falling below a certain level. Since the common stock of the issuer may not pay a dividend, investors in these instruments could experience a reduced income rate, potentially to zero, and conversion would deepen the subordination of the investor, hence worsening the investor’s standing in a bankruptcy. Some CoCos provide for a reduction in the value or principal amount of the security under such circumstances. In addition, most CoCos are considered to be high yield securities and are therefore subject to the risks of investing in below-investment-grade securities.

Duration risk. Duration is a mathematical calculation of the average life of a fixed-income or preferred security that serves as a measure of the security’s price risk to changes in interest rates (or yields). Securities with longer durations tend to be more sensitive to interest rate (or yield) changes than securities with shorter durations. Duration differs from maturity in that it considers potential changes to interest rates, and a security’s coupon payments, yield, price and par value and call features, in addition to the amount of time until the security matures. Various techniques may be used to shorten or lengthen a portfolio’s duration. The duration of a security will be expected to change over time with changes in market factors and time to maturity.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore. For recipients in the Middle East: This document is for informational purposes only. It does not constitute or form part of any marketing initiative or any offer to issue or sell (or any solicitation of any offer to subscribe or purchase) any products, strategies or other services, nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this document wishes to receive further information with regard to any products, strategies or other services, it shall specifically request the same in writing from us.