Investors’ search for diversification and inflation protection has put a spotlight on infrastructure, made brighter by massive public investment programs, accelerating power demand, and an increasingly digitalized economy.

KEY TAKEAWAYS

- A generational wave of capital investment opportunity

An estimated nearly $100 trillion in necessary infrastructure spending in the next 15 years will drive opportunities amid governments’ limited financial means to satisfy all the demand. - An asset class with compelling investment attributes

Listed infrastructure has delivered returns competitive with broad equities, but with attractive downside capture and lower volatility. - A diverse universe supported by structural growth trends

Infrastructure companies are poised to benefit from distinct long-term investment themes, foremost increasing power demand, digital transformation of economies, and deglobalization.

A growing asset class with a compelling track record

The need for and provision of critical, essential services can create potential return-generating investment opportunities—and the necessity for infrastructure investment is substantial and global. In developed markets, critical upgrades are urgently required to address deteriorating service quality, from dangerous lead levels in city water supplies to derailments of freight and passenger trains.

Meanwhile, emerging economies frequently need critical investment to support demographically fueled economic growth, expand urban capacity and meet the demand for higher standards of living.

Globally, governments have either proposed or enacted massive infrastructure investment programs to address these needs, while also seeking to drive a sustainable economic recovery and reduce carbon emissions.

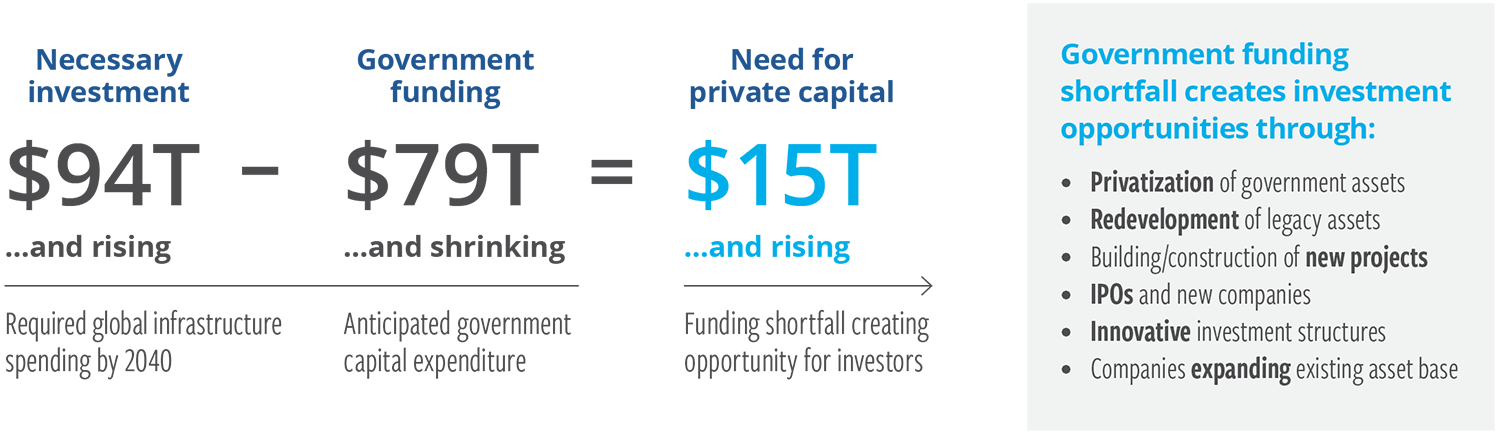

But governments around the world are not positioned to satisfy all the demand. All told, an estimated $15 trillion funding shortfall by 2040 is creating investment opportunities, ranging from privatization of government assets to existing companies expanding their asset bases (Exhibit 1).

EXHIBIT 1

A wave of capital is creating investment opportunities

At June 30, 2025. Source: World Economic Forum, World Bank Group, Cohen & Steers.

The views and opinions are as of the date of publication and are subject to change without notice. There is no guarantee that any market forecast set forth in this presentation will be realized. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin.

While historic public infrastructure spending programs have raised the public profile of infrastructure as an asset class, we see several fundamental factors driving demand for listed infrastructure allocations, including:

- Appetite for infrastructure’s attractive historical investment attributes, including the potential for strong total returns, reduced volatility and inflation protection

- Access to critical forces driving economic change, including power demand and decarbonization, digital transformation of economies, and deglobalization

- Appreciation that listed infrastructure may be an effective complement to private infrastructure investments, offering diversified exposure with access to assets and industries that may be less available to private investors

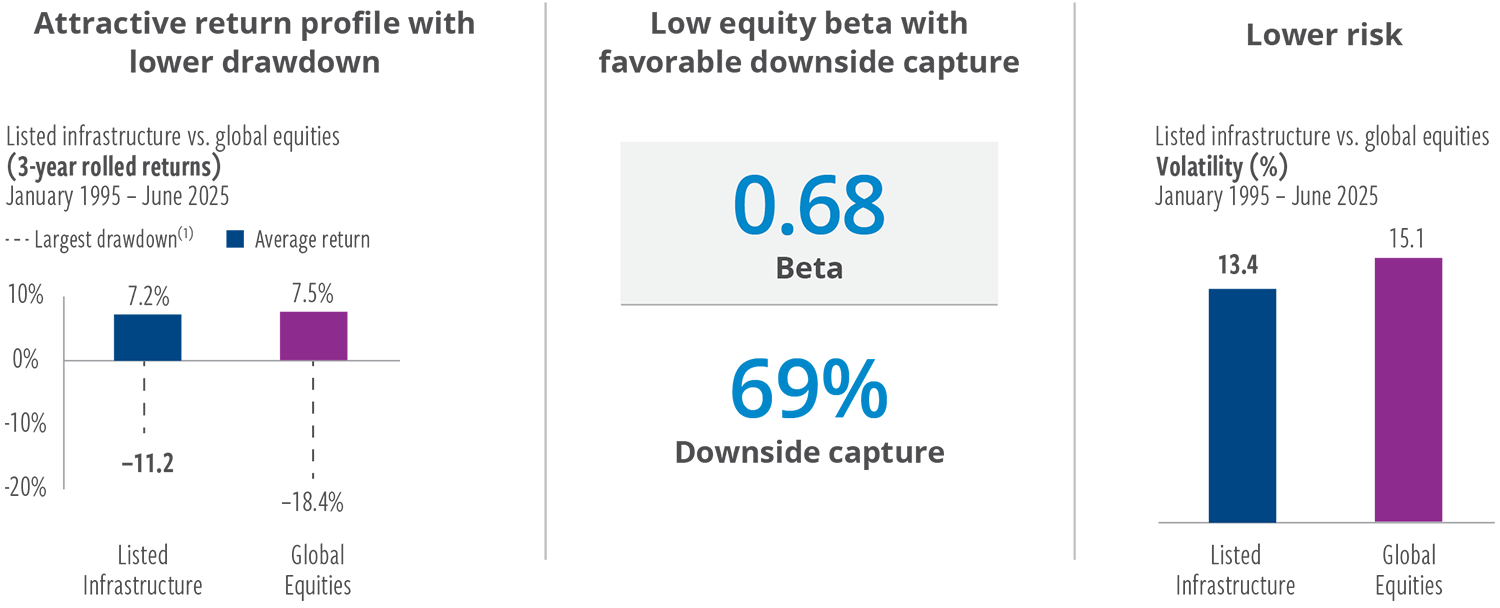

A historically attractive return profile

Listed infrastructure has little overlap with broad stocks, accounting for just 4% of the MSCI World Index, and provides access to subsectors and investment themes that are typically under-represented in equity market allocations.

Performance data over the past 30 years (Exhibit 2) indicates that listed infrastructure offers the potential for:

- Competitive performance relative to global equities, with three-year rolling total returns averaging 7.2%

- Resilience in down markets, with infrastructure historically experiencing 60–70% of the market’s decline, on average, in periods when global equities retreat

- Lower volatility, driven by the relatively predictable cash flows of infrastructure businesses

Listed infrastructure has delivered returns competitive with broad equities, but with attractive downside capture, low equity beta and lower volatility.

EXHIBIT 2

Listed infrastructure can provide return consistency and diversification

At June 30, 2025. Source: Bloomberg and Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. Beta is a measure of the volatility of a security or a portfolio in comparison to the market as a whole. Downside capture is a measure of an investment’s average relative performance in periods of negative returns for broader markets. Volatility as measured by standard deviation of returns around an investment’s average return. Listed infrastructure represented by Linked UBS Global 50/50 Net/FTSE Global 50/50 Net. Global equities is represented by the MSCI World Index Net. (1) Largest drawdown refers to the rolled 3-year period with the lowest return over the course of the stated time period.

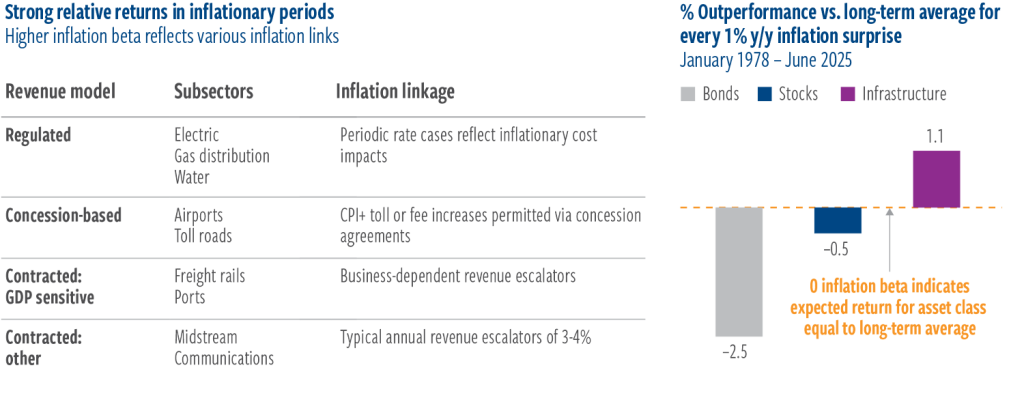

Beneficial inflation characteristics

Infrastructure has historically delivered strong relative returns during periods of higher-than-expected inflation, compared with modest or negative relative performance for stocks and bonds (Exhibit 3). This positive sensitivity has resulted from inflation-linked pricing mechanisms in many infrastructure revenue models, which provide for contractual adjustments to user fees. These adjustments may be based on fixed increases approximating inflation or on variable increases linked to consumer or producer price changes (see inset table).

EXHIBIT 3

At June 30, 2025. Source: Bloomberg and Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. Inflation beta was determined by calculating the multivariate regression beta of 1-year real returns to the difference between the year-over-year realized inflation rate and lagged 1-year ahead expected inflation, including the level of the lagged expected inflation rate. Expected inflation as measured reflects median inflation expectation from University of Michigan Survey of 1-Year Ahead Inflation Expectations. Stocks represented by S&P 500 Index. Bonds represented by ICE BofA U.S. 7-10 Year Treasury Index Infrastructure represented by 50/50 Blend of Datastream World Pipelines and Datastream World Gas, Water, & Multi-Utilities through December 2002; Dow Jones Brookfield Global Infrastructure Index thereafter.

Providing essential services

The historically compelling return profile is the result of fundamental characteristics of infrastructure businesses:

| Long-lived real assets | Infrastructure companies own physical assets with useful lives typically greater than 20 years. |

| High barriers to entry | Competition is often limited by strict zoning restrictions, large capital requirements and, in some cases, exclusivity rights, which make it difficult or prohibitive for new entrants. |

| Stable cash flows | Infrastructure businesses typically operate in regulated industries, potentially enhancing the predictability of cash flows and lowering financial risk. |

| Inelastic demand | The essential nature of infrastructure means demand tends to be relatively resilient in economic downturns (though this varies by sector). |

Through listed infrastructure companies, investors can gain access to a globally diversified portfolio of infrastructure assets with a market capitalization of roughly US$5.8 trillion, spread across the Americas, Europe and Asia Pacific. The investment universe contains a broad range of subsectors spanning four main categories:

| Utilities | Communications | Transportation | Energy |

|---|---|---|---|

| Electric | Data centers | Airports | Midstream |

| Gas | Satellites | Marine ports | |

| Renewables | Towers | Railways | |

| Water | Toll roads |

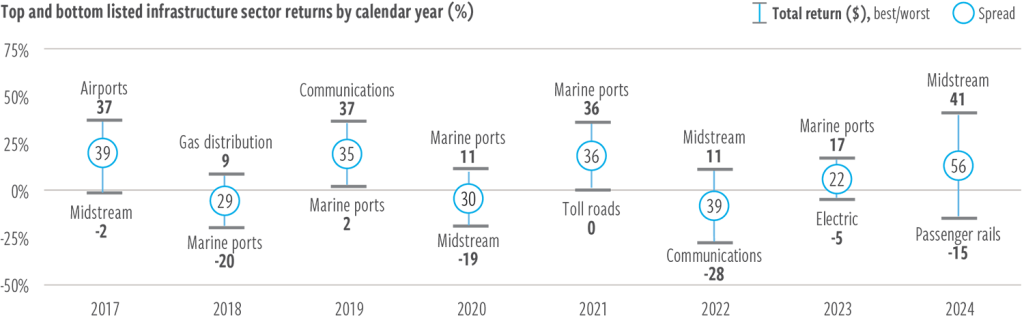

Active management opportunities

Each infrastructure subsector has distinct performance drivers, resulting in a wide dispersion in returns in a given period. In the past 30 years, the difference between the best and worst subsector calendar-year returns was generally higher than 30%, as exemplified in Exhibit 4. Differences in returns are typically even greater at the security level. This wide range in outcomes offers active listed infrastructure investment managers an opportunity to take subsector-level positions with high conviction—which may enhance the performance of portfolios.

EXHIBIT 4

Subsector return dispersion indicates potential for alpha generation

The spread between the year’s best- and worst-performing subsectors has averaged 35%

At June 30, 2025. Source: FactSet and Cohen & Steers.

Past performance is no guarantee of future results. The information above does not reflect information about any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes. See endnotes for index associations, definitions and additional disclosures.

A diverse universe supported by structural growth trends

We believe this asset class is positioned to benefit from three distinct long-term investment themes:

- Power demand and decarbonization driving a global “more of everything” energy approach

- Digital transformation of economies affecting nearly every industry

- Deglobalization and evolving global supply chains

Power demand and decarbonization

We believe that population growth, data processing led by artificial intelligence (AI), precision manufacturing, and other factors in the electrification of the economy will drive power demand growth not seen in a generation. This phenomenon is creating substantial opportunities for listed infrastructure companies. With a “more of everything” approach having become more accepted, we see opportunities related to both fossil fuel and renewable power generation.

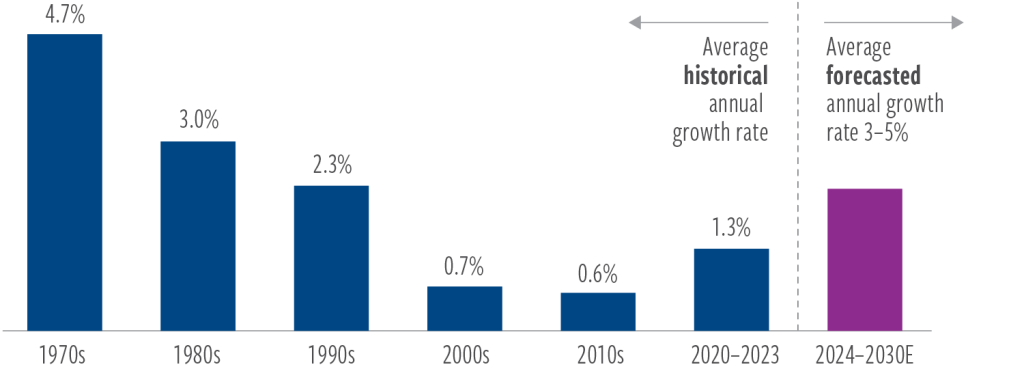

While power demand in the United States has been largely flat for nearly two decades, this trend is now reversing. We expect overall power demand to grow about 4% per year, on average, through 2030 (Exhibit 5). Some utilities are expected to see demand growth well above 5%.

We believe that many investors fail to appreciate that there will be both winners and losers in a world of higher power demand. We believe there will be opportunities for utilities, midstream energy (due to demand for natural gas) and nuclear power. However, there are regulatory nuances to navigate, as well as a need to separate hype from substance. We believe active managers that are acutely focused on infrastructure markets are well positioned to identify true beneficiaries.

EXHIBIT 5

Power demand growth rate

Average annual growth

At June 30, 2025. Source: U.S. Energy Information Administration, Cohen & Steers.

The chart is for illustrative purposes only and do not reflect information about any fund or other account managed or serviced by Cohen & Steers. There is no guarantee that any historical trend illustrated above will be repeated in the future and no way to predict precisely when such a trend will begin. The views and opinions are as of the date of publication and are subject to change without notice.

Digital transformation of economies

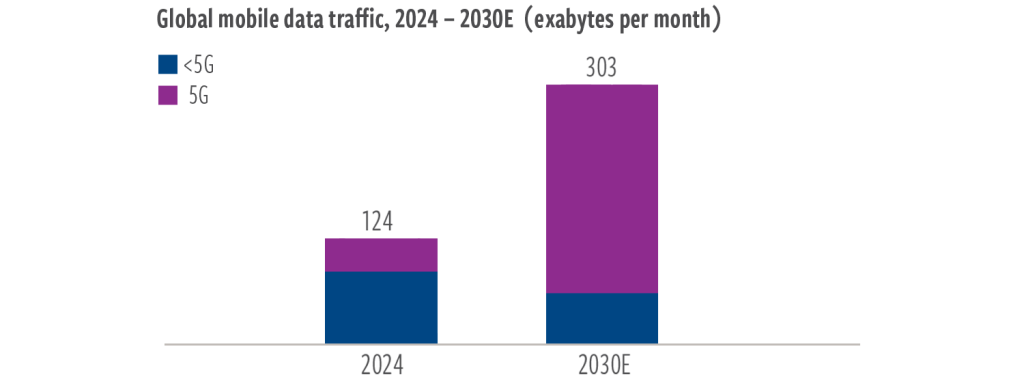

Virtually every industry is moving to build out digital platforms, and the expansion of artificial intelligence (AI), in its early innings, appears poised to be the next key long-term driver of this trend, on top of 5G demand. AI automation and broader enterprise and consumer adoption will likely require greater investment in wireless networks.

The rapid expansion in data usage in the late-4G environment, coupled with the expected urgent demands of the approaching 5G era, will likely require massive investments to expand communications infrastructure capacity over the next decade. Industry estimates show potential for a roughly 2.5x increase in global mobile data traffic by 2030, with 5G networks expected to carry more than half of all traffic (Exhibit 6). This growth will likely support demand for cell tower, satellite, and data center services assets for years to come.

EXHIBIT 6

Mobile data expected to more than double

Growing data intensity will require major investments in wireless networks and data centers

At June 30, 2025. Source Ericsson Mobility Report.

There is no guarantee that any market forecast or investment objective set forth in this presentation will be realized. See endnotes for additional disclosures.

Deglobalization and access to logistics assets

We are witnessing an ongoing evolution of global supply chains as a result of diverse geopolitical dynamics, deglobalization, and nearshoring. The infrastructure universe is well represented by companies with assets that help move people and goods around the globe—most specifically, railways, marine ports, airports and toll roads operators. They form a critical part of the global supply chain, facilitating the flow of products ranging from semiconductor chips and medical supplies to everyday household items.

Logistics operators stand to benefit over time from factors such as operational advancements, e-commerce trends, and the strategic onshoring of industrial activity. Freight railway owners, for example, appear poised to continue to see improvements in operations and higher capital returns, potentially increasing company free-cash-flow generation over the next several years.

Infrastructure companies that focus on people and goods logistics account for as much as 30% of leading infrastructure stock indexes.

A liquid complement to private infrastructure

Listed infrastructure is a compelling way to invest in a rapidly growing sector of the global economy, combining attributes of private infrastructure investments with additional potential benefits.

Liquidity and daily pricing

Private investment lock-up periods can exceed 10 years, while investors in listed infrastructure vehicles can adjust allocations at their discretion. Further, listed infrastructure securities trade on public markets in real time. This allows managers to potentially capitalize on dislocations that may occur in listed values, as well as to efficiently manage allocation changes.

Diversification

Private funds often invest in just a handful of assets concentrated within a few geographies and/or subsectors. According to Preqin, the average private fund, for instance, holds around eight investments, versus more than 60 in a listed infrastructure strategy. Listed investments offer greater diversification—even at the security level. For example, listed infrastructure companies often own dozens of assets, which may be spread across multiple geographies.

Corporate governance

Listed companies are subject to oversight by regulatory agencies, which require strict standards of corporate governance, financial reporting and information disclosure. In the U.S., the Securities and Exchange Commission requires quarterly statements as well as detailed supplementals. The adoption of best practices in corporate governance can align managers’ interests with those of shareholders.

A large opportunity set

The number and variety of infrastructure assets available for private investment are fairly low at any point in time. Moreover, some subsectors (notably airports, railroads and digital infrastructure) aren’t typically available to private buyers. A listed infrastructure portfolio can offer exposure across a wide range of sectors, geographic regions and market capitalizations.

A potentially attractive entry point for allocations

As awareness of listed infrastructure’s potential benefits has grown, so too have allocations from both institutional and retail investors. Further, while infrastructure has long appealed to those seeking diversification and stable income, the asset class’s positive inflation characteristics are now providing an additional incentive amid rising tariffs and deglobalization trends.

Given rising inflation risks, uncertain return prospects in fixed income, and growing concentration in equity markets, we believe this is an attractive opportunity to allocate to global listed infrastructure.

Reasons to consider listed infrastructure:

A differentiated performance profile

- History of strong relative performance in inflationary periods

- Potential to improve long-term risk-adjusted returns and reduce downside risk during equity market declines

- Potential for 3–4% dividend yield and 4–6% long-term cash flow growth(1)

Compelling investment themes

- Historical underinvestment in infrastructure leading to critical deterioration in service quality, requiring both public and private capital investment to modernize assets

- Digital transformation affecting nearly every industry, driving long-term growth for cell towers and data centers

- Utilities and renewables developers positioned to benefit from growing support and competitive costs for clean energy investments

- Transportation sectors such as freight rails and marine ports essential to solving the world’s evolving supply chain needs

An attractive complement to private infrastructure

- Ease of implementation at a time of record dry powder in private infrastructure funds

- Opportunities for global diversification within an infrastructure allocation

- Benefits of liquidity and the oversight of public markets

(1) Based on the current dividend yield of the FSE Global Core Infrastructure Index and Cohen & Steers proprietary estimate of long-term cash flow growth as of June 30, 2025.

ABOUT THE AUTHORS

Benjamin Morton, Executive Vice President, is Head of Global Infrastructure and a senior portfolio manager for Cohen & Steers’ infrastructure portfolios, including those focused on master limited partnerships.

Index definitions / important disclosures

An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes. Index comparisons have limitations as volatility and other characteristics may differ from a particular investment.

Global listed infrastructure: FTSE Developed Core Infrastructure 50/50 Index, a market-capitalization-weighted index of infrastructure and infrastructure-related securities in worldwide developed markets; constituent weights are adjusted semi-annually according to three broad industry sectors: 50% utilities, 30% transportation, and a 20% mix of other sectors, including pipelines, satellites, and telecommunication towers. Exhibit 4: 50/50 Blend of Datastream World Pipelines and Datastream World Gas, Water and Multi-Utilities through July 2008; Dow Jones Brookfield Global Infrastructure Index thereafter. The Dow Jones Brookfield Global Infrastructure Index is a float-adjusted market-capitalization-weighted index that measures performance of globally domiciled companies that derive more than 70% of their cash flows from infrastructure lines of business.

Global equities: MSCI World Index, a free-float-adjusted index that measures the performance of large- and mid-capitalization companies representing developed-market countries and is net of dividend withholding taxes.

U.S. Treasuries: ICE BofA U.S. 7-10 Year Treasury Index is composed of U.S. Treasury Notes with a 7-10-year maturity.

Data quoted represents past performance, which is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any market forecast made in this document will be realized. The views and opinions presented in this document are as of the date of publication and are subject to change without notice. This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or to account for the specific objectives or circumstances of any investor. We consider the information to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Cohen & Steers does not provide investment, tax or legal advice. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing. The views and opinions expressed are not necessarily those of any broker/dealer or its affiliates. Nothing discussed or suggested should be construed as permission to supersede or circumvent any broker/dealer policies, procedures, rules or guidelines.

Risks of investing in global infrastructure securities. Infrastructure issuers may be subject to regulation by various governmental authorities and may also be affected by governmental regulation of rates charged to customers, operational or other mishaps, tariffs, and changes in tax laws, regulatory policies, and accounting standards. Foreign securities involve special risks, including currency fluctuation and lower liquidity. Some global securities may represent small and medium- sized companies, which may be more susceptible to price volatility than larger companies. No representation or warranty is made as to the efficacy of any particular strategy or fund or to the actual returns that may be achieved.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority of the United Kingdom (FRN 458459). Cohen & Steers Asia Limited is authorized and registered with the Hong Kong Securities and Futures Commission (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No. C188319).

For readers in the Middle East: This document is for informational purposes only. It does not constitute or form part of any marketing initiative, any offer to issue or sell, or any solicitation of any offer to subscribe or purchase, any products, strategies or other services, nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event the recipient of this document wishes to receive further information with regard to any products, strategies or other services, it shall specifically request the same in writing from us.