The first quarter of 2026 reinforced the role of listed infrastructure as a differentiated asset class within diversified portfolios.

KEY TAKEAWAYS

- When global equities declined amid heightened volatility and geopolitical shocks, and bonds offered limited diversification benefits, global listed infrastructure delivered strong positive returns.

- Several features of listed infrastructure were reinforced during the first quarter: Infrastructure’s inflation linkage, its defensive, predictable earnings tied to essential services, and the contribution of income to infrastructure’s total returns.

- In that context, the quarter can be viewed as a real-time validation of the long-term case for infrastructure across market cycles.

The first quarter of 2026 reinforced the role of listed infrastructure as a differentiated asset class within diversified portfolios.

When global equities declined amid heightened volatility and geopolitical shocks, and bonds offered limited diversification benefits, global listed infrastructure delivered strong positive returns. As in prior periods of market stress, infrastructure’s essential service exposure, inflation linked revenues and income generation helped support portfolios when traditional assets faltered.

Markets entered 2026 on relatively firm footing, supported by solid earnings and continued investment tied to artificial intelligence. That optimism faded as geopolitical tensions escalated following the onset of the war in Iran, triggering an energy supply shock, renewed inflation concerns and a shift toward risk aversion and toward hard assets, otherwise known as HALO (hard assets, low obsolescence).

As the quarter progressed:

- Global equity markets declined amid rising uncertainty.

- Government bond yields moved higher, limiting the offset bonds have historically provided during equity drawdowns.

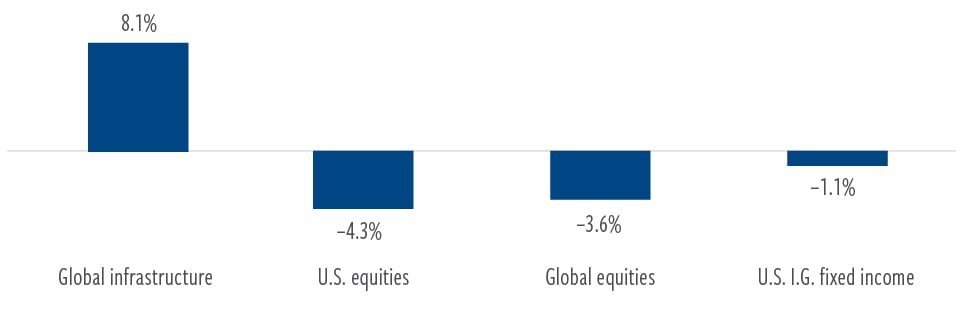

Against this backdrop, global listed infrastructure delivered materially different results. As represented by the FTSE Global Core 50/50 Net Tax Index, the asset class generated an 8.1% total return during the first quarter, outperforming broader equity markets.

Performance was not driven by a single outcome or subsector. Instead, it reflected the asset class’s structural characteristics.

EXHIBIT 1

Global Listed Infrastructure Resilience Q1 2026

At March 31, 2026.

Past performance is no guarantee of future results. Q1 performance represented by: U.S. equities: S&P 500 Total Return Index. Global equities: MSCI ACWI Total Return Index. U.S. equities: S&P 500 Total Return Index. Global equities: MSCI ACWI Total Return Index. U.S. I.G. fixed income: Bloomberg US Aggregate Bond Index. Global infrastructure: FTSE Global Core Infrastructure 50/50 Net Tax Index.

Several features of listed infrastructure were reinforced during the quarter:

Inflation linkage and pricing frameworks.

Energy infrastructure and regulated utilities benefit from contractual and regulatory mechanisms that allow revenues to adjust over time in higher inflation environments. Midstream energy, particularly crude oil focused operators and LNG exporters, performed strongly as energy prices rose following supply disruptions.

Defensive, predictable earnings tied to essential services.

Regulated utilities outperformed on resilient earnings and improved growth visibility. Continued strength in electric utilities reflected accelerating power demand

expectations, particularly from data centers, reinforcing the defensive yet growth oriented nature of many infrastructure businesses. Though consumers may be struggling because of the “slowflationary” shift brought about by tensions in the middle east, infrastructures bills still “get paid” each month.

Income contribution amid volatility.

With financial conditions tight and interest rates elevated, income accounted for a meaningful portion of total return, highlighting infrastructure’s potential role as a source of diversified income when market volatility increases.

A familiar pattern: Echoes of 2022

The quarter followed a pattern investors have seen before. In 2022, infrastructure similarly demonstrated resilience during a period marked by inflation shocks, rising interest rates and equity/credit declines. In both episodes, infrastructure performed largely as intended.

It helped to preserve capital and generate income during environments in which traditional 60/40 asset class correlations rose.

These periods offer a timely illustration of the long term investment case for listed infrastructure. As equity markets declined and bonds struggled to provide diversification, infrastructure performed in line with its historical characteristics, supported by regulated,

concession based and contracted revenue models that have typically delivered competitive returns with lower volatility and resilience during periods of elevated inflation.

Episodes like Q1 tend to highlight these attributes most clearly, reinforcing infrastructure’s role as a strategic portfolio allocation rather than a cyclical trade. And we have seen first hand the evidence of the interest with growing client allocations, after what was a record year for infrastructure inflows for Cohen & Steers in 2025.

Beyond its defensive profile, infrastructure’s durability is rooted in the essential nature of the services it provides and the scale of investment required to support them. Aging assets, modernization needs, decarbonization, digitalization and supply chain reconfiguration are driving a sustained demand for capital at a time when

governments alone cannot meet global infrastructure funding needs. Listed infrastructure offers investors liquid access to these essential assets, complementing private market exposure while retaining flexibility.

In that context, the quarter can be viewed as a real time validation of the long term case for infrastructure across market cycles.

Index definitions and important disclosures

Data quoted represents past performance, which is no guarantee of future results. The views and opinions presented are as of the date of publication and are subject to change. There is no guarantee that any market forecast set forth will be realized. This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or to account for the specific objectives or circumstances of any investor. We consider the information to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Cohen & Steers does not provide investment, tax or legal advice. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Risks of Investing in global infrastructure securities. Infrastructure issuers may be subject to regulation by various governmental authorities and may also be affected by governmental regulation of rates charged to customers, operational or other mishaps, tariffs, and changes in tax laws, regulatory policies, and accounting standards. Foreign securities involve special risks, including currency fluctuation and lower liquidity. Some global securities may represent small and medium-sized companies, which may be more susceptible to price volatility than larger companies. No representation or warranty is made as to the efficacy of any particular strategy or fund or to the actual returns that may be achieved. No representation or warranty is made as to the efficacy of any particular strategy or fund or the actual returns that may be achieved.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers U.S. registered open-end funds are distributed by Cohen & Steers Securities, LLC and are only available to U.S. residents. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367).

Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No. C188319). Cohen & Steers Singapore Limited is a private company limited by shares in the Republic of Singapore.

For recipients in the Middle East: This document is for information purposes only. It does not constitute or form part of any marketing initiative, any offer to issue or sell, or any solicitation of any offer to subscribe or purchase, any products, strategies or other services nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this document wishes to receive further information with regard to any products, strategies other services, it shall specifically request the same in writing from us.