With surging global power demand and continuing climate commitments, nuclear power is a growing pillar for reliable, clean electricity and future energy security.

KEY TAKEAWAYS

- The world is searching for clean and reliable baseload power

Traditional fossil fuels can provide predictable energy generation but often produce unwanted emissions. Renewable energy is cleaner, but it can be intermittent and variable. Nuclear is a technology that can satisfy both demands. - Nuclear policy momentum is building

The COP28 declaration to triple nuclear capacity by 2050, backed by a growing coalition of countries, signals unprecedented international commitment to nuclear expansion as governments prioritize reliable, clean baseload power. - Supply chain bottlenecks and technological innovation present both risks and opportunities

Critical shortages in uranium conversion, enrichment and specialized components create near-term challenges but also significant investment opportunities across the nuclear value chain.

The early stages of a global nuclear buildout

Nuclear power’s share of global electricity generation has declined from its 1980s peak of 17% to roughly 9% today, despite maintaining stronger resilience in markets like the United States, where it still provides approximately 18% of electricity generation. The period following the 2011 Fukushima disaster marked a particularly challenging phase, with new reactor starts barely offsetting shutdowns globally, leading to systematic underinvestment across the entire nuclear value chain. High-profile cost overruns like those at Plant Vogtle (a new-build reactor in Georgia) have further damaged nuclear’s reputation and deterred investment. The Georgia project’s doubling from $14 billion to over $30 billion, combined with decade- long delays, exemplifies the financial risks that make utilities and investors wary of new nuclear construction. These budget disasters create a vicious cycle: Fewer projects mean less learning and economies of scale, while regulatory uncertainty and construction inexperience drive costs even higher on future builds.

Yet today’s landscape tells a markedly different story. The current global fleet of approximately 440 reactors is projected to expand to about 500 by 2030, with over 400 additional reactors in various stages of planning and development. This growth trajectory reflects not just renewed confidence in nuclear technology, but a fundamental recognition that achieving deep decarbonization at scale requires dispatchable, baseload power sources that can complement the inherent intermittency of renewable energy.

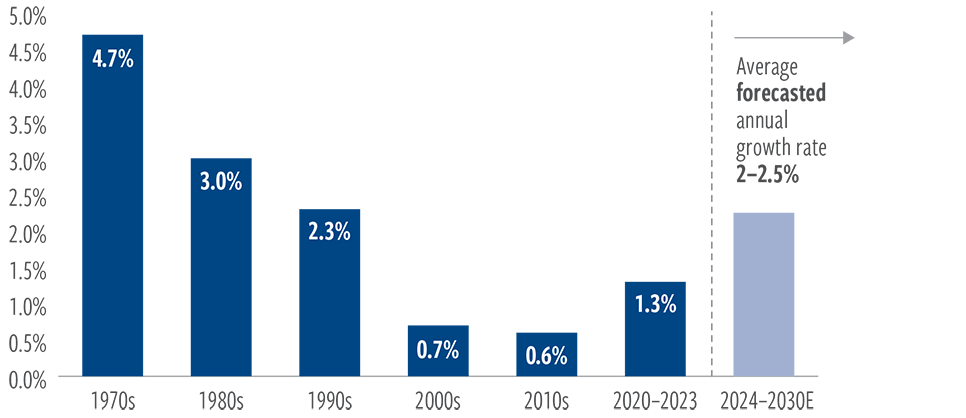

EXHIBIT 1

Back to the ‘80s: Power demand to climb

Average annual growth (%)

At August 31, 2024. Source: U.S. Energy Information Administration, Cohen & Steers.

The four-phase nuclear development strategy

We believe the path to nuclear expansion follows a pragmatic, phased approach that maximizes existing assets while building toward next-generation capabilities.

- Extending the operating lives of existing reactors, providing crucial bridging capacity until new construction comes online (2022–2026). With the global nuclear fleet having a median age of 32 years and 66% of reactors exceeding 31 years, license extensions represent the most immediate and cost- effective way to preserve nuclear capacity. For the past decade, the world has generally been decommissioning these reactors across Europe and North America. However, we have observed numerous extension agreements in recent years and expect this trend to continue.

- Reactivating previously suspended but still- operable facilities (2024–2028). Countries like the United States, Japan and India have reactors that have been shuttered but could potentially return to service safely in the near-to-medium term. These represent relatively quick wins in capacity restoration, without the lengthy timelines associated with new construction. The recently announced restart of Three Mile Island is an example of “turning back on” stagnant capacity.

- Leveraging brownfield development of existing or former nuclear sites for new reactor construction and capacity additions (2026–2035). This approach benefits from established infrastructure, regulatory familiarity and community acceptance while reducing development risks. We expect to begin to see announcement of new construction and development activity inside existing reactor sites in the coming years.

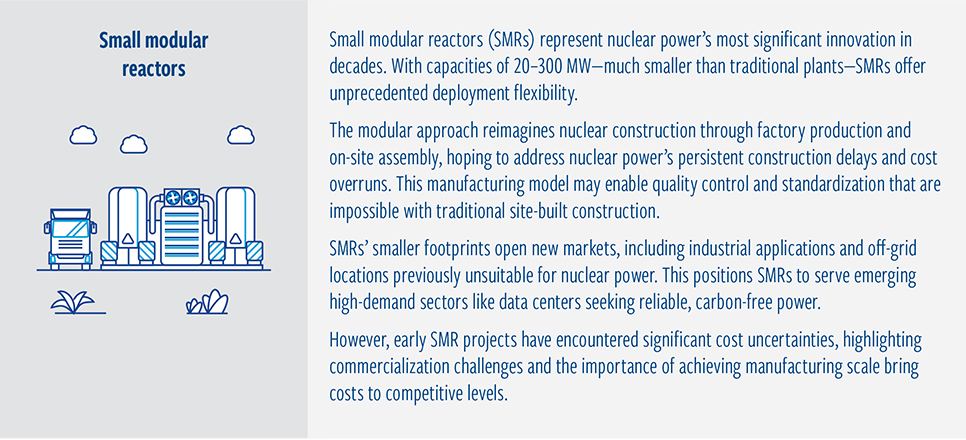

- New large-scale reactors, small modular reactors (SMRs) and future technologies (2030–2040). We do believe that the industry will see a wave of new development activity towards the end of this decade. This includes large-scale new nuclear developments as well as the scaling and installation of new technologies. Many of these will likely require government support and/or guarantees to greenlight projects.

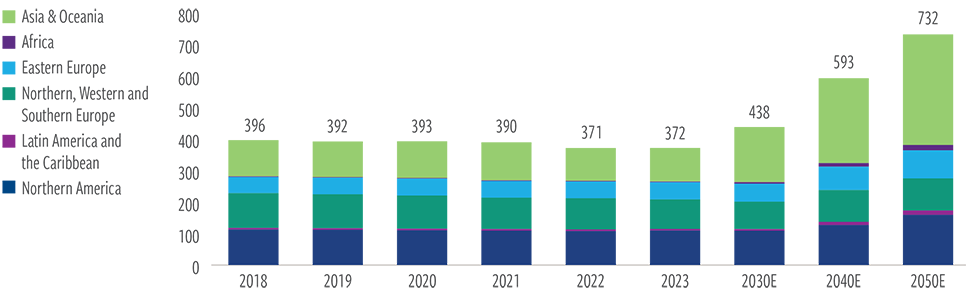

EXHIBIT 2

Nuclear electrical generation capacity forecasted to almost double by 2050

Nuclear plant capacity by geography, GW(e)

At March 31, 2025. Source: IAEA, “Energy, Electricity and Nuclear Power Estimates for the Period up to 2050.”

Years 2018–2023 represent actual nuclear electrical generating capacity levels. Future expected nuclear electrical generating capacity levels are low-high averages. Asia & Oceania represents the sum of Western Asia, Southeastern Asia, Central and Eastern Asia, and Oceania.

Critical success factors

The nuclear industry’s growth trajectory depends on addressing three fundamental challenges that have historically constrained expansion.

Continued technological development remains paramount. While traditional reactor designs will continue serving important roles, advanced reactor concepts—including SMRs, molten salt reactors, and eventually nuclear fusion—are essential for nuclear energy’s long-term competitiveness. Many of these advanced designs require different fuel types, particularly high- assay low-enriched uranium (HALEU), which presents both opportunities and challenges for the fuel supply chain.

Regulatory rationalization represents another critical enabler. The nuclear licensing process, particularly in the United States under Nuclear Regulatory Commission oversight, has historically been complex and time-consuming. The development of the Part 53 framework, mandated by the Nuclear Energy Innovation and Modernization Act, aims to create more efficient regulatory pathways for advanced reactors while maintaining rigorous safety standards. However, this framework remains in development, and successful implementation will be crucial for enabling timely SMR deployment. In addition, it is likely going to require government support and investment to catalyze large-scale investments by private industry, given the long construction cycles of nuclear assets.

Perhaps most importantly, the industry must rebuild supply chains weakened by decades of underinvestment. The nuclear fuel cycle encompasses multiple critical steps: uranium mining, conversion to UF6, enrichment, fuel fabrication, power generation and waste management. Each step presents potential bottlenecks that could constrain growth—but each may also present opportunities for investors.

The nuclear industry’s growth trajectory depends on addressing three fundamental challenges that have historically constrained expansion.

Uranium supply challenges and opportunities

Looking ahead, the industry faces a projected structural supply deficit in uranium by the 2030s, as growing demand outpaces production from existing and planned mines. This potential shortage could support higher uranium prices, benefiting mining companies while creating cost pressures for utilities. The contracting dynamics are important: Utilities typically secure most uranium through term contracts spanning 5–10 years, providing some price stability but also creating long-term supply certainty.

The nuclear fuel supply chain reveals both vulnerabilities and investment opportunities. Conversion of mined uranium to enriched fuel represents a notable bottleneck, with significant production capacity concentrated in Russia and China. Geopolitical tensions have highlighted the risks of over- reliance on potentially adversarial suppliers, creating urgent needs for domestic capacity development.

Enrichment capabilities present even more acute challenges. While the supply chain for low-enriched uranium used in existing reactors is reasonably well established, many advanced reactors require HALEU enriched to 5–20% U-235. Global HALEU supply is currently severely limited, with production at scale primarily controlled by Russian entities. Establishing reliable domestic HALEU supply chains faces a classic “chicken-and-egg” problem: High upfront investments are required without guaranteed demand from reactor developers, while reactor developers hesitate to commit without assured fuel supplies.

Investment opportunities across real assets sectors

The nuclear industry’s transformation presents a concentrated investment landscape where a limited number of key players dominate due to complex technology requirements, national security considerations and stringent regulatory frameworks. This concentration creates protective barriers that potentially enhance returns for well-positioned investors.

Uranium producers face compelling near-term fundamentals as rising demand from plant extensions, restarts and new construction converges with supply constraints from decades of underinvestment. This supply/demand imbalance supports higher uranium prices, with geopolitical factors adding upside as Western producers benefit from reduced reliance on Russian uranium supplies. Established producers are positioned to capitalize on this reshoring trend while new supply development remains limited.

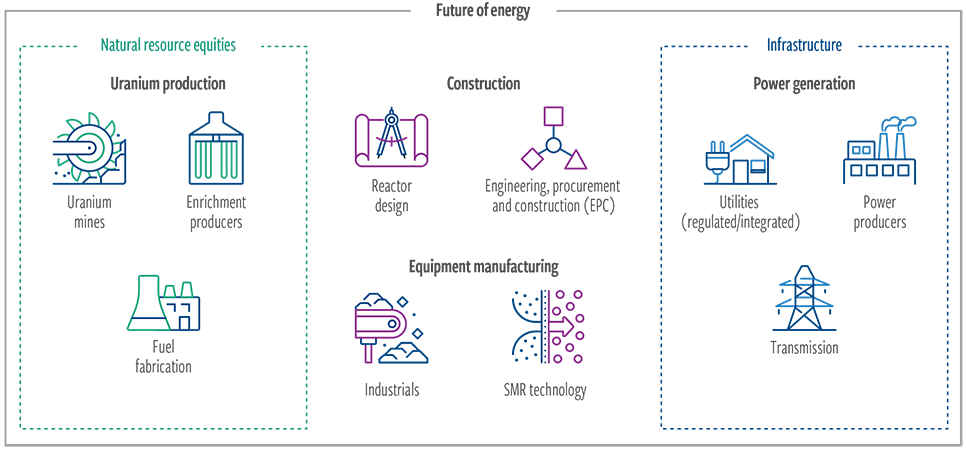

EXHIBIT 3

There are investment opportunities across the nuclear power value chain

Utility companies positioned to add nuclear capacity present opportunities, particularly those with existing nuclear expertise and brownfield development potential. Growing interest from hyperscale technology companies seeking reliable, carbon-free power for data centers is an unprecedented demand driver. Utilities with nuclear fleets benefit from life extension economics and potential capacity uprates.

Engineering and construction companies with nuclear expertise benefit from expanding project pipelines as the industry moves through its development strategy. The comprehensive nature of nuclear services creates opportunities for firms that can navigate demanding technical and regulatory requirements. High barriers to entry, including needs for specialized expertise and security clearances, limit competition and protect market positions.

Nuclear equipment manufacturers operate in concentrated markets where exacting requirements and safety standards allow only select companies to compete effectively. This segment benefits from both maintenance needs of the existing fleet and new construction demand.

Specialized components and reactor systems represent areas where technical expertise creates sustainable competitive advantages.

Looking toward the mid-2030s, small modular reactor developers represent the highest-risk, highest-potential-return segment. While SMR technologies remain in early development and have uncertain timelines, successful developers could capture significant value as standardized manufacturing scales. However, investors must evaluate risks, including untested designs, regulatory uncertainty and unproven cost structures.

High barriers create compelling opportunities for investors

The nuclear energy sector presents investors with a rare convergence of compelling fundamentals that demand serious consideration. Momentum is building across multiple dimensions simultaneously: Policymakers worldwide are reversing decades of anti-nuclear sentiment, hyperscale technology companies are signing multibillion-dollar power purchase agreements, and supply chain constraints are creating pricing power for positioned players.

This is not a theoretical opportunity requiring investors to time a distant inflection point, but rather an unfolding transformation in which we believe early positioning can capture significant value creation. The sector’s concentrated structure, high barriers to entry, and long project timelines create natural moats for incumbents while limiting new competition.

Leveraging our leadership and experience in infrastructure and natural resource investing, we are actively evaluating opportunities across the nuclear value chain, participating in what may prove to be one of the most significant industrial transformations of the coming decades.

ABOUT THE AUTHORS

Tyler Rosenlicht, Senior Vice President, is a portfolio manager for Global Listed Infrastructure and serves as Head of Natural Resource Equities.

Index Definitions and important disclosures

Data quoted represents past performance, which is no guarantee of future results. This material is for informational purposes and reflects prevailing conditions and our judgment as of this date, which are subject to change. There is no guarantee that any market forecast set forth in this presentation will be realized. This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment.

This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this presentation to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Active management does not ensure a profit or guarantee to protect against a loss and actively managed strategies may underperform passively managed strategies.

Risks of Investing in global infrastructure securities. Infrastructure issuers may be subject to regulation by various governmental authorities and may also be affected by governmental regulation of rates charged to customers, operational or other mishaps, tariffs, and changes in tax laws, regulatory policies, and accounting standards. Foreign securities involve special risks, including currency fluctuation and lower liquidity. Some global securities may represent small and medium- sized companies, which may be more susceptible to price volatility than larger companies. No representation or warranty is made as to the efficacy of any particular strategy or fund or to the actual returns that may be achieved.

Risks of Investing in Energy: Investing involves risk, including entire loss of capital invested. There can be no assurance that the investment strategy will meet its investment objectives. Diversification is not guaranteed to ensure a profit or protect against loss. The portfolio will be subject to more risks related to the energy sector than if the portfolio were more broadly diversified over numerous sectors of the economy. A downturn in the energy sector of the economy could have a larger impact on the portfolio than on an investment company that does not concentrate in the sector. Investments within the energy industry may be highly volatile due to significant fluctuation in the prices of energy commodities as well as political and regulatory developments.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association.

Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.

For recipients in the Middle East: This document is for informational purposes only. It does not constitute or form part of any marketing initiative or any offer to issue or sell (or any solicitation of any offer to subscribe or purchase) any products, strategies or other services, nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this document wishes to receive further information with regard to any products, strategies or other services, it shall specifically request the same in writing from us.