An analysis by Fred Reish of Faegre Drinker Biddle & Reath LLP, shows 401(k) plan sponsors should consider diversified real assets when selecting investment alternatives, historically a low-correlated asset class offering daily liquidity, inflation sensitivity and the prospect of enhanced risk-adjusted returns.

KEY TAKEAWAYS

- Best practices for DC plans demand a balanced investment lineup

Plan sponsors have a fiduciary obligation to provide participants with a broad range of investment alternatives. Real assets are an often-overlooked choice that can play an important role as a plan diversifier. - Real assets offers helpful investment characteristics

Real assets have historically generated strong full-cycle returns while reducing a portfolio’s overall volatility and offering a level of potential defense against unexpected inflation. - Diversified real asset funds can manage asset class tradeoffs

While single-strategy funds are an option, separate categories can be volatile on their own and require individual monitoring. We believe investors are better served by a bundled approach that invests in multiple real assets classes.

An analysis by Fred Reish, Faegre Drinker Biddle & Reath LLP

Executive summary

In selecting investment alternatives, 401(k) plan sponsors—acting as fiduciaries—must apply generally accepted investment theories and prevailing investment industry practices. This means, in part, selecting a 401(k) lineup that is diversified across a sufficient number of asset classes (e.g., stocks, bonds, international investments, cash equivalents and real assets) to allow participants to develop appropriate portfolios in their accounts that reasonably reflect their risk and return objectives.

Unfortunately, the guidance issued by the Department of Labor does not specify which, or how many, asset classes should be included. Instead, plan fiduciaries should look to the prevailing practices within the institutional investment industry. To be conservative, well-informed plan sponsors should consider including at least one investment from each of the major asset classes.

Some fiduciaries recognize that real estate is a major, or core, asset class. But fiduciaries and investors may want to consider a broader definition of real assets, including a blend of real estate, listed infrastructure, natural resource equities and commodities. Real assets investments can play an important role in diversification because their market value fluctuation is not highly correlated to that of stocks and bonds. Further, real assets offer the prospect of enhanced risk-adjusted returns and potential defense against inflation. While many target date fund suites have exposure to Treasury inflation-protected securities, few are sufficiently allocated to real assets, particularly commodities.

Products that invest in publicly traded (listed) markets offer a convenient way to access the global opportunity set of real assets. As a result, prudent plan sponsors should consider including diversified real assets as an investment alternative in their plans.

Best practices for DC plans demand a balanced investment lineup

Under ERISA, plan sponsors must engage in a prudent process to select investments for their retirement plans. This means that a plan sponsor—usually acting through a plan committee—must apply generally accepted investment theories and prevailing investment industry practices in selecting the plan investment lineup.

“Generally accepted investment theories” refers to the principles used to guide the selection of asset classes that balance expected return and the risk associated with that return, taking into account how different asset classes perform in relation to others in the market (i.e., the correlation among investments). This includes, for example, modern portfolio theory. “Prevailing investment industry practices” refers to both (i) the strategies and factors used by investment professionals in assessing risk compared to projected return, and (ii) the selection of investments to populate the asset classes.

A plan sponsor’s application of these theories and practices should result in the creation of a diversified investment lineup over a broad range of good quality and reasonably priced investment choices.

The U.S. Department of Labor (DOL) has identified the importance of diversification in several ERISA regulations.(1) This includes, for example, the requirements for a plan to be considered a “404(c) plan”: The plan sponsor must provide a broad range of investments that are internally diversified (i.e., not overly dependent on a limited number of holdings), and have materially different risk and return characteristics, to enable participants to put together prudent and appropriate investment portfolios in their accounts.

The qualified default investment alternative (QDIA) regulation requires that safe harbor default investments be “diversified so as to minimize the risk of large losses” and “designed to provide varying degrees of long-term appreciation and capital preservation through a mix of equity and fixed income exposures.”

While the DOL does not mandate a specific mix of equity and fixed income or dictate the asset classes to be included, the message is clear: diversification across different asset classes is required to fulfill the ERISA fiduciary duty for investments.

Why should real assets be included?

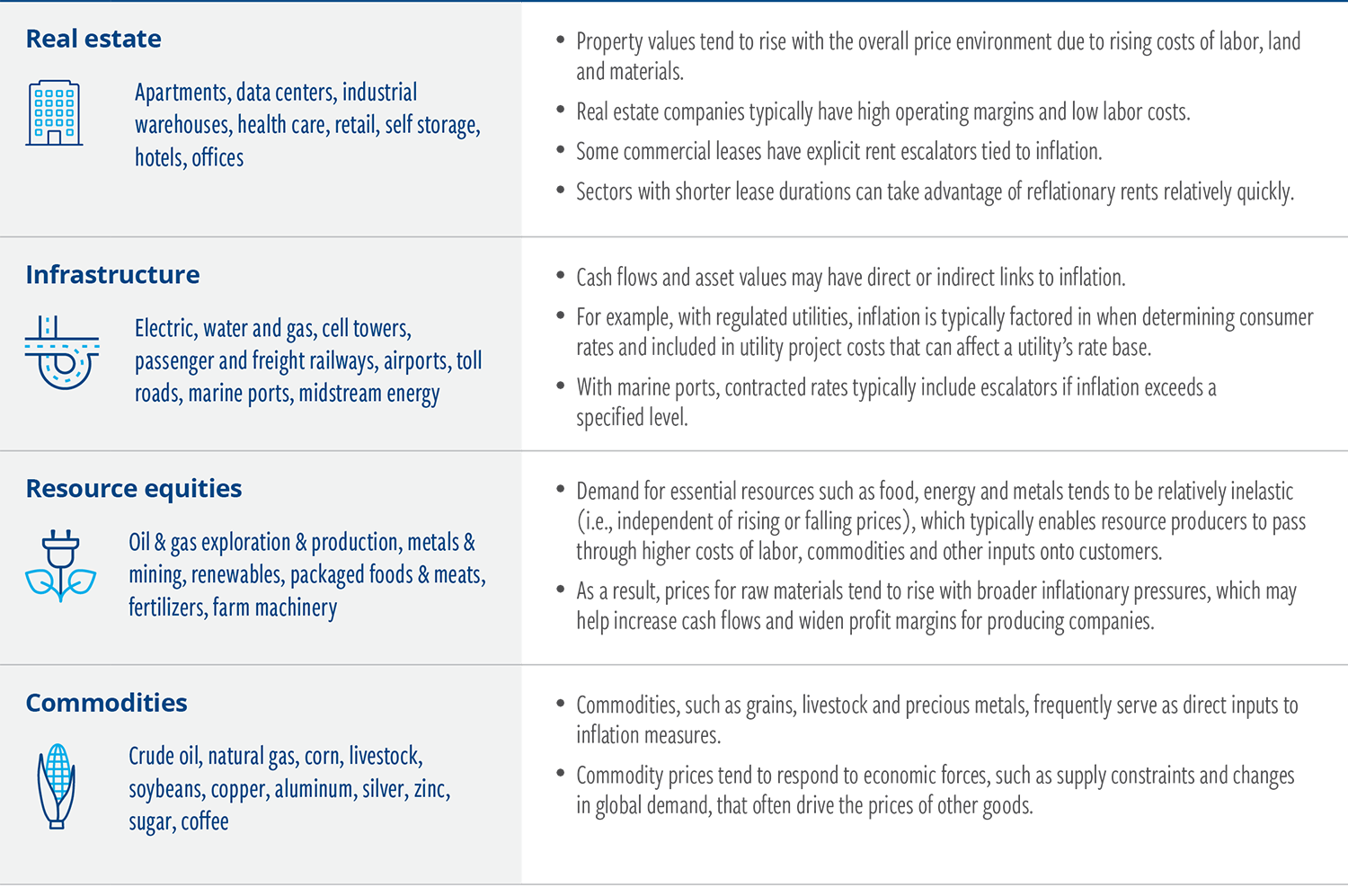

Real assets can be broad in scope; in this paper, the term refers to publicly traded investments in real estate investment trusts or REITs (the most liquid, transparent and efficient way of offering real estate), listed infrastructure, natural resource equities

and commodities.

There are several reasons real assets belong in plan lineups:

- Diversified real assets are a foundational asset class with high inflation sensitivity, diversification potential seeking to reduce portfolio volatility and improve risk-adjusted returns. They have historically delivered attractive full-cycle returns.

- Sophisticated institutional asset managers—including defined benefit plans, endowments and foundations— frequently allocate 10%–20% to diversifiers such as real assets.(2) This suggests that including real assets in a portfolio is a prudent practice.

- Real assets are increasingly recognized as a significant element of a well-diversified portfolio.

In a recent article in Pensions & Investments, Katie Hockenmaier, Mercer’s U.S. defined contribution director explained:

“Mercer believes that tying multiple asset classes together through a multi-asset, diversified inflation-protection fund can be beneficial because having these different asset classes work together can actually provide better results vs. having them on a stand-alone basis and having participants try to figure out how much to allocation to each one or where to allocate to all of them.”(3)

If real assets are to be included, the plan sponsor must use a prudent process to select them—that is, the same process they would use for the selection of all investments for the plan. Selecting real assets, then, should not present a unique challenge. Simply put, a prudent process entails gathering relevant information about the investment, assessing that information and making a decision. This is sometimes referred to as an “informed and reasoned” decision, since it should be informed by the information gathered and reasoned based on the prudent assessment of the information.

What information would be relevant in deciding to include real assets?

As with almost any asset, this would include, among other things, information about performance, volatility, cost, liquidity, daily valuation, tradability and diversification benefit.

Since 1991, a blend of real assets has delivered competitive returns relative to other major asset classes, with three of four categories (commodities were the exception) performing roughly in-line or better than global equities.(4) Further, publicly traded real assets are liquid and valued daily. This means that, like other mutual fund investments included in a plan lineup, both the plan and participants have the opportunity to buy or sell real assets on days when the markets are open. REITs, infrastructure and natural resource equities may also be diversified across industry sectors, as well as within specific sectors in their respective categories. This tends to mitigate the risk of a downturn in any one sector. As a lawyer, I am not able to give investment advice, but my point here is that a plan sponsor will need to gather information about each of these elements and other relevant factors and make its own assessment.

Another consideration is whether to select a real assets fund that follows an index and is passively managed or to consider actively managed real assets. While single- category passively managed real assets funds exist, active funds comprise nearly the entire market share of diversified real assets funds. Investing in real assets can be operationally complex and require additional resources and expertise to manage. As such, “lowest cost” should not be the primary factor in selecting a real assets fund for a plan. Moreover, market performance in the decade ending December 31, 2022, shows that most actively managed real assets funds outperform their benchmarks over longer periods.(5)

Real assets could be a valuable addition for participants. For example, with appropriate investment education and, possibly, the use of asset allocation models, participants could construct better-diversified portfolios in their accounts. Similarly, advisors and consultants could include real assets in model portfolios, custom target date funds and managed accounts.(6) The use of real assets investments in providing these services would be consistent with generally accepted investment theories.

While asset class statistics about performance and volatility may be useful in deciding whether to include real assets investments, they don’t address which investment. A plan sponsor will need to engage in a prudent process to evaluate a reasonable cross-section of funds that meet the plan’s overall investment objectives. In essence, this requires assessing the features of the alternatives using the same methodology employed for selecting other investments for the plan lineup.

In summary, neither the DOL nor the courts have defined what constitutes a broad range of investments or what asset classes should be included in a well-diversified lineup. However, modern portfolio theory is based on the concept that the inclusion of asset classes that are not highly correlated—that is, where the market value fluctuation tends to be different from that of many other asset classes and investments—will help protect participant accounts over the long term by better balancing return and volatility. This suggests that plan sponsors should include all of the major asset classes in their investment lineup rather than picking and choosing only certain classes. And this means that plan sponsors should consider real assets in establishing a well- diversified, balanced lineup of investment alternatives— both as a best practice and as good risk management.

Fiduciary requirements

Under ERISA, the sponsors of participant-directed plans owe the participants the duties of prudence and loyalty, and must act with the exclusive purpose of providing them with benefits.(7) In fulfilling these duties, they are required to engage in a prudent process in making decisions about the plan, including selecting the plan’s investment lineup. (For the sake of convenience, the term “plan sponsor” is used to refer to the fiduciary of a plan who is responsible for these decisions—sometimes, this is a committee appointed by the board of directors or designated officers of the sponsor.)

In the context of selecting investments, the Department of Labor (DOL) has described the prudent process in a regulation.(8) A plan sponsor must:

“…[give] appropriate consideration to those facts and circumstances that, given the scope of such fiduciary’s investment duties, the fiduciary knows or should know are relevant to the particular investment or investment course of action involved…”

The DOL goes on to explain in this regulation what constitutes “appropriate consideration,” noting that it includes, but is not necessarily limited to:

“(i) A determination by the fiduciary that the particular investment or investment course of action is reasonably designed, as part of the portfolio…to further the purposes of the plan, taking into consideration the risk of loss and the opportunity for gain (or other return) associated with the investment or investment course of action…”

In other words, the plan sponsor needs to evaluate how the proposed investment fits within the overall investment policy of the plan, applying modern portfolio theory. (When the DOL refers to a plan’s “portfolio” of investments, the term should be read to mean the plan’s investment lineup in a participant-directed plan.)

The DOL then explains specific factors a plan sponsor should consider:

“(ii) Consideration of the following factors as they relate to the portfolio:

“(A) The composition of the portfolio with regard to diversification;

“(B) The liquidity and current return of the portfolio relative to the anticipated cash flow requirements of the plan; and

“(C) The projected return of the portfolio relative to the funding objectives of the plan.”

While not the only relevant factors, the DOL lays out three key elements a plan sponsor needs to look at:

- Diversification: Diversification: How does each proposed investment fit within and aid in the creation of a diversified lineup that includes investments over multiple asset classes?

- Liquidity: Is the investment sufficiently liquid to enable the plan sponsor to eliminate the investment from the plan lineup if it is prudent to do so? In addition, in a participant-directed plan, are participants able to reasonably move out of the investment?

- Performance: Does the investment provide a reasonable return—both currently and on a projected basis—in relation to the plan’s cash flow needs and also in relation to the projected risk of the investment?

Other guidance also reflects the importance of analyzing the costs associated with investments, in addition to performance and liquidity.(9) In an analogous regulation on the selection of annuities for defined contribution plans, the DOL says that a plan sponsor must:

“Appropriately conclude that … the cost of the annuity contract is reasonable in relation to the benefits and services to be provided under the contract.”(10)

Even though this refers to cost in relation to an annuity contract, it reflects the general principle that plan sponsors need to take cost into account in selecting an investment for the plan.

The essence of this process is that the plan sponsor must:

- Gather relevant information about the investments,

- Assess that information, and

- Make an informed decision based on the assessment that it performed.

As part of the process, the plan sponsor has to perform two jobs simultaneously: (1) it must analyze whether the plan’s investment lineup is adequately and appropriately diversified, and (2) it must analyze information about each investment. In both cases, there is an emphasis on diversification in addition to performance and liquidity. And the analysis of diversification requires that sponsors apply generally accepted investment theories, such as modern portfolio theory.(11)

The DOL has described the importance of diversification in several specific contexts. For example, ERISA Section 404(c) gives protection to fiduciaries in a participant- directed plan by saying that if a participant combines the plan’s investment alternatives in a way that results in losses, the plan sponsor is not liable.(12) In order to obtain this relief, plan sponsors must provide a “broad range” of investment alternatives. The regulation under this section says that a plan offers a broad range:

“Only if the available investment alternatives are sufficient to provide the participant or beneficiary with a reasonable opportunity to:

“(A) Materially affect the potential return on amounts in his individual account with respect to which he is permitted to exercise control and the degree of risk to which such amounts are subject;

“(B) Choose from at least three investment alternatives:

“(1) Each of which is diversified;

“(2) Each of which has materially different risk and return characteristics;

“(3) Which in the aggregate enable the participant or beneficiary by choosing among them to achieve a portfolio with aggregate risk and return characteristics at any point within the range normally appropriate for the participant or beneficiary; and

“(4) Each of which, when combined with investments in the other alternatives, tends to minimize through diversification the overall risk of a participant’s or beneficiary’s portfolio;

“(C) Diversify the investment of that portion of his individual account with respect to which he is permitted to exercise control so as to minimize the risk of large losses, taking into account the nature of the plan and the size of participants’ or beneficiaries’ accounts.” [Emphasis added](13)

In essence, the 404(c) regulation describes the “broad range” in terms of diversification at two different levels. There must be diversification of the available investment alternatives within the plan. In addition, there must be diversification within each investment individually. The purpose is to enable participants to “minimize the risk of large losses.” While 404(c) provides fiduciary protection, it may also be viewed as a fiduciary requirement in that it is difficult to imagine a plan sponsor creating a lineup that does not meet the broad range test.

In another regulation, defining the requirements for a plan’s default investment alternative to be qualified (i.e., a QDIA), the DOL also mandates diversification. Each of the mandated QDIAs must be:

- An investment fund or model portfolio that “applies generally accepted investment theories [and] is diversified so as to minimize the risk of large losses”; or

- An investment management service “applying generally accepted investment theories, [that] allocates the assets of a participant’s individual account to achieve varying degrees of long-term appreciation and capital preservation through a mix of equity and fixed income exposures [i.e., diversified].” [Emphasis added](14)

When the DOL refers to diversification, it does not specify the asset classes or industry segments that must be included in a plan’s lineup. In fact, the DOL has acknowledged that “there is no single, complete, universally accepted theory of optimal investment.

Instead, there are competing and evolving theories which have much in common (what might be called ‘generally accepted’ theories).”(15)

Nevertheless, there is a generally recognized definition of diversification. It consists of:

“The act of investing in different industries, areas, countries, and types of financial instruments, to reduce the chance that all of the investments will drop in price at the same time.” (16)

It is commonly understood to mean “spreading the portfolio among different types of assets, including not only stocks but also bonds, real estate, international investments, and cash equivalents.”(17) Thus, a plan sponsor seeking to fulfill the fiduciary obligation to provide a broad range of investment alternatives for selection by its participants—to satisfy the diversification requirement.

However, each of the various real assets investment options available, such as REITs, infrastructure, natural resource equities and commodities, has unique characteristics. Sponsors should evaluate if individual real assets options align with their plan’s investment objectives. Individual real assets categories may also come with higher risk than traditional investments.

Plan sponsors should consider the risk tolerance of their participants when including separate real assets categories in plan lineups.

Real assets mutual funds that invest across multiple asset classes can reduce participants’ concentration risk exposure from investing in any one real assets category. Additionally, a diversified real assets option can simplify a plan’s investment lineup while potentially reducing costs associated with the individual category investments.

However, Morningstar does not have a “multi-strategy real assets” category presently. As a result, the funds are spread across roughly a dozen categories, often ranked against other funds with unrelated objectives and different asset bases. Comparing real asset funds against a “peer group” dominated by non-real asset funds can result in inconsistent rankings over the course of a market cycle. Given the outsized impact of composition differences, we believe such peer comparisons may not be reliable when selecting a diversified real assets fund.

Real assets offer helpful investment characteristics

This section discusses factors a plan sponsor should consider when deciding on a plan’s investment lineup. As a lawyer, I am unable to provide and have not undertaken to provide investment advice. Statistical and factual information about investments included below is based on information provided by Cohen & Steers, on which I have relied without independent investigation.

The term “real assets” here refers to publicly traded, actively managed investments in real estate investment trusts (REITs), global infrastructure, natural resource equities and commodities. Individual (non-publicly traded) properties or infrastructure assets may be prudent investments in some very large defined benefit plans since there is less need for liquidity to meet the plan’s benefit needs. However, for small to midsized participant-directed defined contribution plans, there is generally a need for two types of liquidity. The first is at the plan level so that a plan sponsor can remove and replace an investment alternative with relative ease if it is prudent to do so. The second is at the participant level to facilitate changes in the investment alternatives in a participant’s account, typically on a daily basis. Publicly traded real assets provide both types of liquidity.

A large investment universe

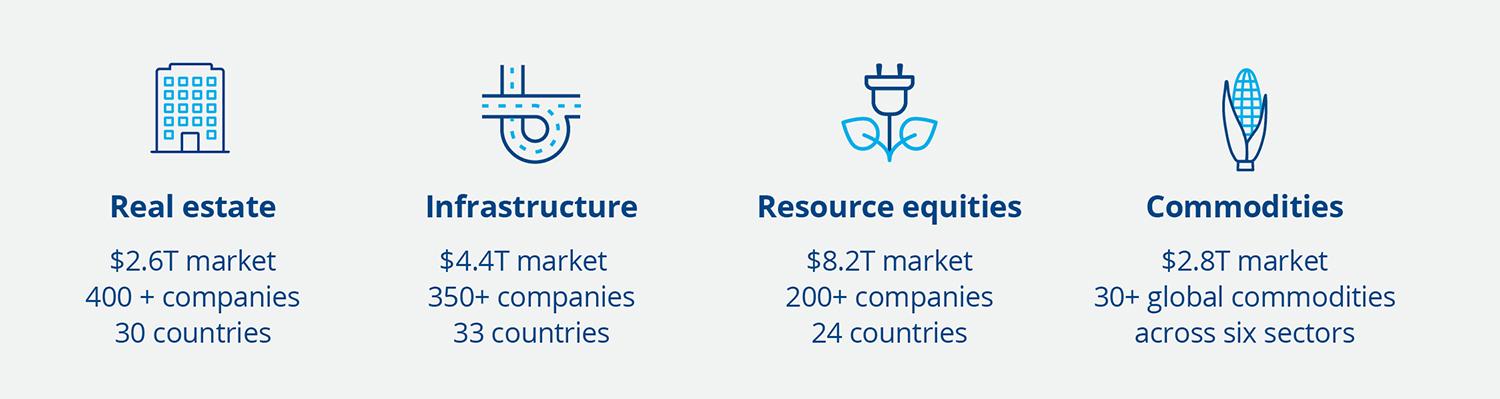

One reason for including listed real assets in a plan lineup is the market size as a core asset class. With a total capitalization of $18 trillion as of the end of 2022, listed real assets is the third-largest asset class behind fixed income and equities (Exhibit 1).

EXHIBIT 1

A broad global investment universe made up of diverse subsectors across different industry groups

Size and scope of the listed real assets market

At December 31, 2022. Source: Cohen & Steers.

An inflation-hedging portfolio solution

Listed real assets can serve as a strong defense against inflation. What sets the four core listed asset categories of real estate, infrastructure, resource equities and commodities apart more than any other attribute is that their returns have historically benefited from inflation surprises. In other words, real assets tend to outperform during periods of rising and unexpected inflation, in sharp contrast to the modest or negative inflation sensitivity of broad equities and bonds (Exhibit 2).

The economic drivers of real assets are often directly or indirectly tied to inflationary trends; this linkage historically has resulted in outsized returns when inflation exceeds expectations. An allocation to real assets may therefore help to preserve future purchasing power, potentially offsetting the vulnerability to unexpected inflation that is historically common to traditional portfolios of stocks and bonds.

EXHIBIT 2

Historical outperformance in inflationary environments

Average annual real returns in periods of rising and unexpected inflation (%) June 1991–June 2023

At June 30, 2023. Source: Barclays, Bloomberg, Dow Jones, FTSE, S&P, Refinitiv Datastream, Cohen & Steers.

Past performance is no guarantee of future results. Inflation measured as the year-over-year change in the Consumer Price Index for all urban consumers, published by the U.S. Bureau of Labor Statistics. Rising inflation is measured as a positive year-over-year increase in the 12-month inflation rate. Unexpected inflation measured as a positive difference between the year-over-year realized inflation rate and lagged 1-year-ahead expected inflation, as measured by the University of Michigan survey of 1-year-ahead inflation expectations. The real assets blend is not representative of an actual portfolio and is for illustrative purposes only. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. The mention of specific sectors is not a recommendation or solicitation to buy or hold securities in a particular sector and should not be relied upon as investment advice. See end notes for index associations, definitions and additional disclosures.

How real assets are tied to inflation

Market betas reflect diversification opportunity

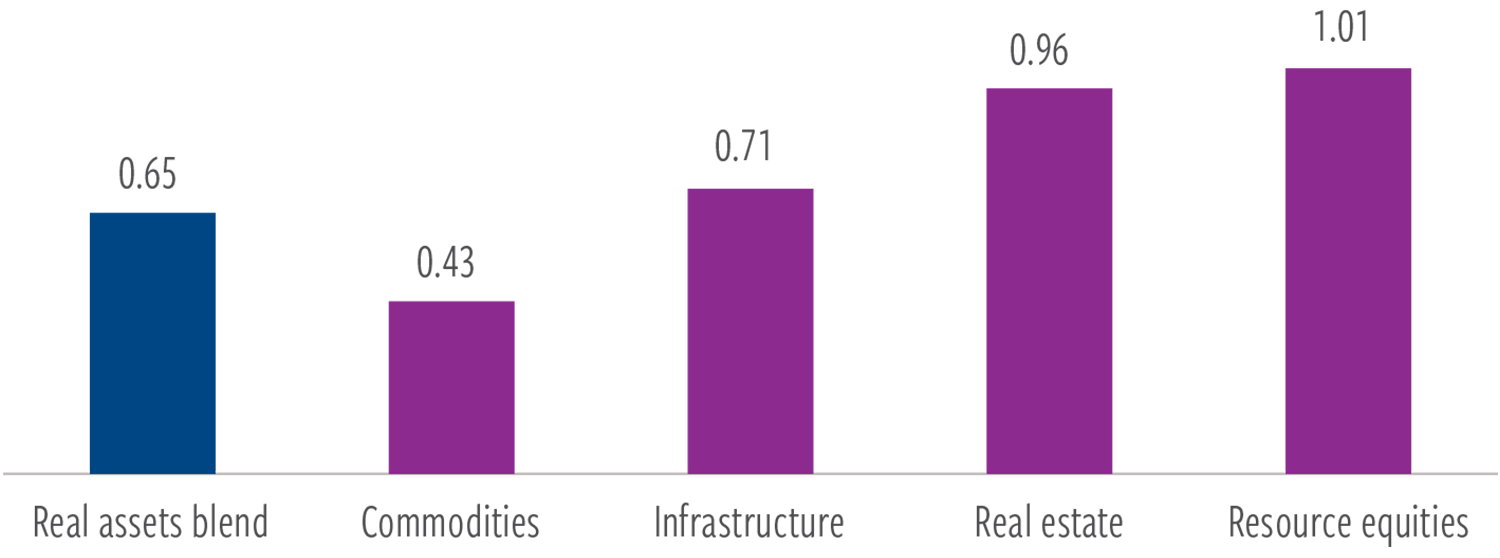

The historical benefits of real assets having differentiated economic drivers can be seen in their “beta,” which is their sensitivity to the broad global equity market (Exhibit 3). A beta of less than 1 indicates that the asset class tends to behave differently or be less volatile than the market. A beta greater than 1 indicates that the asset class exhibits more volatility than the broad equity market. In this case, the low market beta of real assets suggests significant diversification potential, which may help to reduce portfolio volatility—and, we believe, improve risk-adjusted returns.

Real assets represent investments in sectors that are underrepresented in broad equity markets. During periods when both equity and fixed income markets simultaneously underperform―historically not an infrequent occurrence―real assets have shown great resilience, outperforming bonds and equities.

EXHIBIT 3

Low market beta suggests significant diversification potential

Beta to global equities

June 1991–March 2023

At June 30, 2023. Source: Barclays, Bloomberg, Dow Jones, FTSE, S&P, Refinitiv Datastream and Cohen & Steers.

Past performance is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. Beta measures the relative volatility of an investment as compared to a standard market index. A market index will always be equal to 1.00. An investment with a higher/lower Beta, more/less than 1.00, is more/less volatile than the market index. The real assets blend is not representative of an actual portfolio and is for illustrative purposes only. See end notes for index associations, definitions and additional disclosures.

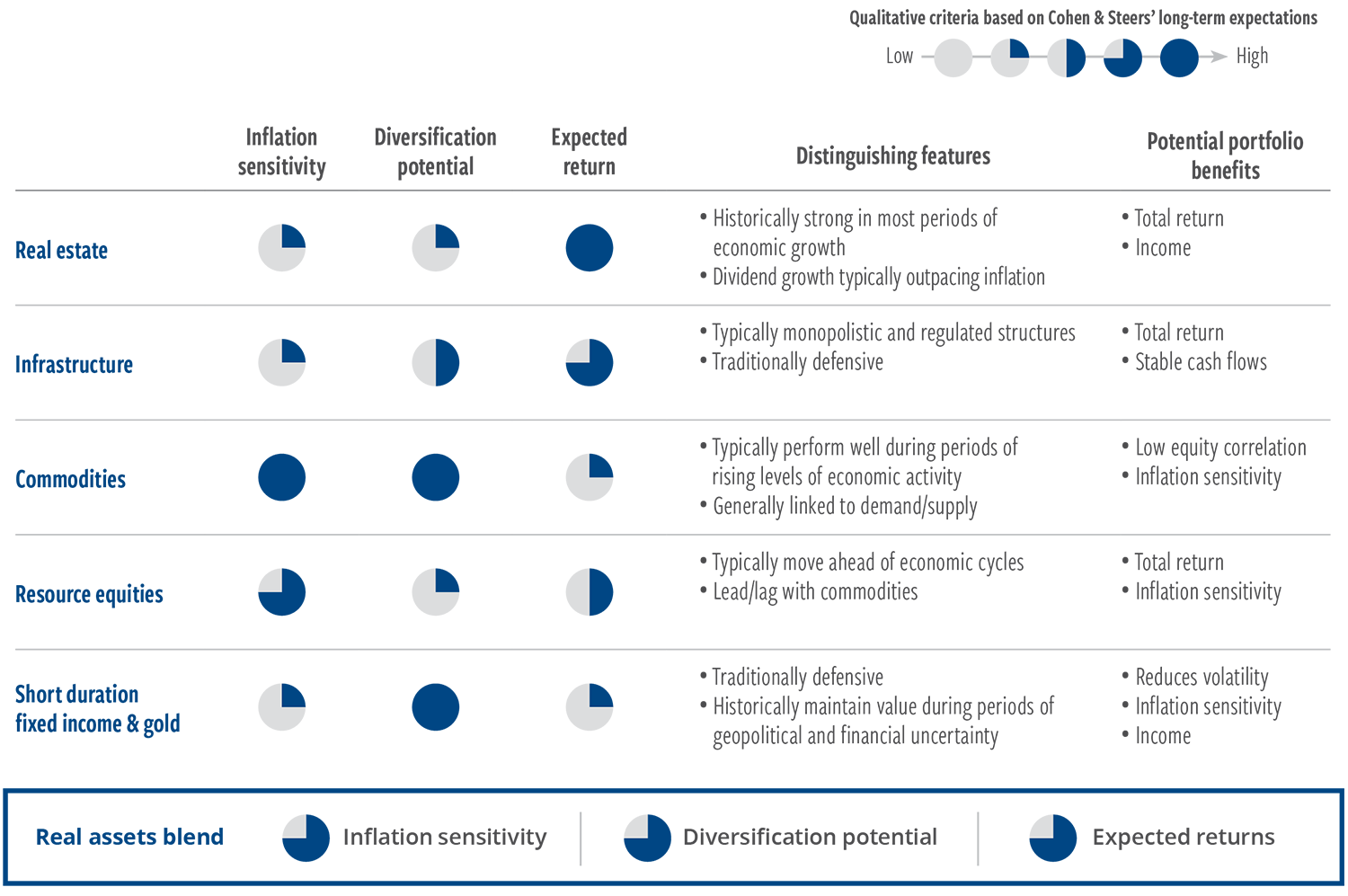

Approaching real assets as a single asset class

A diversified blend of real assets may offer an effective way for investors to target common objectives of a real assets allocation—such as boosting inflation sensitivity, enhancing diversification and improving the risk-return profile—while potentially dampening the swings that investors may experience with separate allocations to individual real assets classes (Exhibit 4).

EXHIBIT 4

Individual category tradeoffs can be managed in a diversified framework

At June 30, 2023. Based on Cohen & Steers’ analysis and expectations.

There is no guarantee that any market forecast set forth in this presentation will be realized. The mention of specific sectors is not a recommendation or solicitation to buy or hold securities in a particular sector and should not be relied upon as investment advice. The qualitative criteria in the above chart represent relative strengths across the real asset categories discussed in this presentation, based on realized historical data since June 1991 and Cohen & Steers’ expectations. See end notes for index associations, definitions and additional disclosures.

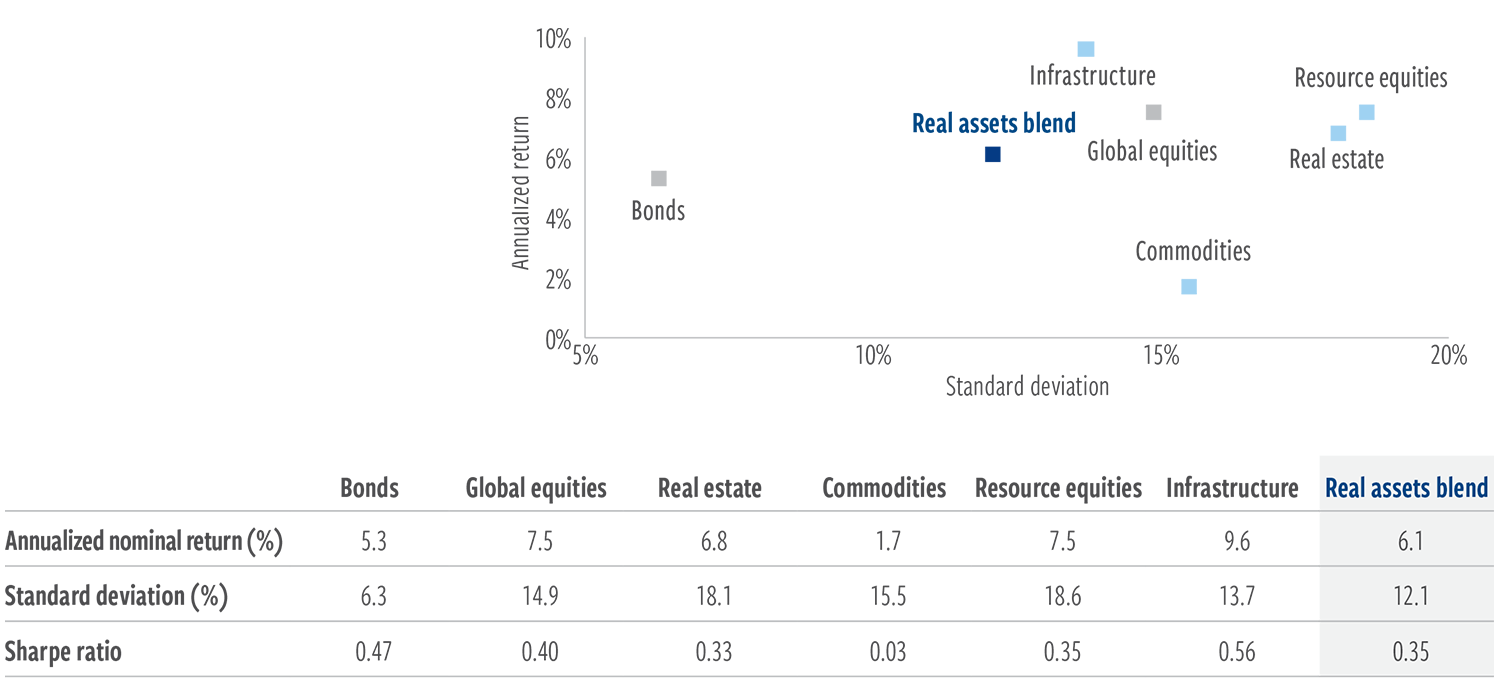

Attractive risk-adjusted returns

Real assets have historically delivered attractive full-cycle returns that can potentially improve risk-adjusted portfolio returns without sacrificing growth potential. Over the last 30+ years, a blend of real assets has exhibited returns competitive with global equities, but with lower volatility (Exhibit 5).

EXHIBIT 5

A real assets blend has exhibited favorable risk-adjusted returns

Risk/reward profile

June 1991–June 2023

At June 30, 2023. Source: Barclays, Bloomberg, Dow Jones, FTSE, S&P, Refinitiv Datastream and Cohen & Steers.

Past performance is no guarantee of future results. Return reflects compound annualized return. Risk reflects annualized standard deviation of monthly returns. Standard deviation, also known as historical volatility, measures the dispersion of a set of data from its mean and is used by investors to gauge the amount of expected volatility. Sharpe ratio is a measure of risk-adjusted return, calculated by subtracting the risk-free rate from a return and dividing that result by the standard deviation. The higher the Sharpe ratio, the higher the risk-adjusted return. The real assets blend is not representative of an actual portfolio and is for illustrative purposes only. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. See end notes for index associations, definitions and additional disclosures.

Implementing real assets in retirement plans

Given their attractive investment attributes, we believe adding real assets to plan investment lineups can be an effective way for fiduciaries to help plan participants diversify their portfolios and improve potential outcomes.

Historical analysis shows that including a blend of real assets in an illustrative stock and bond portfolio offers the potential to reduce volatility, improve risk-adjusted returns and increase sensitivity to inflation (Exhibit 6). We attribute these results to the distinct return drivers of the underlying assets and their individual sensitivities to the business cycle, which provide potential diversification benefits.

EXHIBIT 6

Real assets can potentially have a positive impact on a stock/bond portfolio

June 1991–March 2023

At June 30, 2023. Source: Barclays, Bloomberg, Dow Jones, FTSE, S&P, Refinitiv Datastream and Cohen & Steers.

Past performance is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. Return reflects compound annualized return. Volatility (risk) reflects annualized standard deviation of monthly returns. Sharpe ratio is a measure of risk-adjusted return, calculated by subtracting the risk-free rate from a return and dividing that result by the standard deviation. The higher the Sharpe ratio, the higher the risk-adjusted return. Inflation beta was determined by calculating the multivariate regression beta of 1-year real returns to the difference between the year-over-year realized inflation rate and lagged 1-year ahead expected inflation, including the level of the lagged expected inflation rate. Inflation is measured using the Consumer Price Index (CPI) for all urban consumers, published by the United States Department of Labor’s Bureau of Labor Statistics. Expected inflation as measured reflects median inflation expectation from the University of Michigan Survey of 1-Year Ahead Inflation Expectations. A real rate of return is the annual percentage return realized on an investment, which is adjusted for changes in prices due to inflation. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. Stocks represented by MSCI World Index. Bonds represented by ICE BofA U.S. 7-10 Year Treasury Index. Real assets blend comprised of 27.5% global real estate securities, 27.5% commodities, 15% natural resource equities, 15% global listed infrastructure, 10% short-duration fixed income and 5% gold. See end notes for index associations, definitions and additional disclosures.

Conclusion

In selecting investment alternatives, 401(k) plan sponsors must apply generally accepted investment theories—the principles used to guide the creation of an investment portfolio that balance expected return over the degree of risk associated with that return—and prevailing investment industry practices— the strategies and factors used by investment professionals in selecting investments. This means, in part, setting a 401(k) lineup that is diversified across major asset classes (i.e., stocks, bonds, international investments, cash equivalents and alternatives) and within each investment.

Real assets are now considered a core asset class and, as such, are used by institutional investors for diversification. These investments can play an important role in diversification because their market value fluctuation tends to differ from stocks and bonds (that is, they are not highly correlated). As a result, plan sponsors, acting as fiduciaries, should consider including real assets as an investment alternative in their plans.

While single-strategy funds for gaining exposure to real assets are an option, separate categories can be volatile on their own and require individual monitoring. We believe investors can benefit from a bundled approach that invests in multiple asset classes. A diversified real assets option can also simplify a plan’s investment lineup while potentially reducing costs associated with the individual category investments.

(1) See, e.g., ERISA Reg §§2550.404a-1, 404c-1 and 404c-5.

(2) Data compiled by Cohen & Steers, sourced from 1,000 private and public plans, endowments and foundations, as of September 20, 2022

(3) Pensions & Investments, “Sponsors mull new inflation fighting methods,” https://www.pionline.com/pi-1000-largest-retirement-plans/sponsors-mull-new-methods-fight-inflation.

(4) Source: Cohen & Steers; data quoted represents past performance, which is no guarantee of future results.

(5) Source: Cohen & Steers; data quoted represents past performance, which is no guarantee of future results.

(6) Target date funds that are generally available in the marketplace typically have little or no allocation to real estate. Morningstar, Cohen & Steers.

(7) ERISA Section 404(a).

(8) ERISA Regulation Section 2550.404a-1.5.

(9) See, e.g., ERISA Regulation Section 2550.404a-4.

(10) Id. at subsection (b)(4).

(11) See, e.g., ERISA Regulation Section 2550.404c-5.

(12) The section says that fiduciaries have a defense from liability for losses that result from a participant’s exercise of investment control over his or her account, so long as various requirements are met.

(13) ERISA Regulation Section 404c-1(b)(3).

(14) ERISA Regulation Section 2550.404c-5(e)(4).

(15) Preamble to proposed regulations on Investment Advice – Participants and Beneficiaries, 73 Fed. Reg. 49896 (August 22, 2008), at fn 59.

(16) Collins English Dictionary.

(17) Id.

Before investing in any Cohen & Steers fund, please consider the investment objectives, risks, charges, expenses and other information contained in the summary prospectus and prospectus, which can be obtained by visiting cohenandsteers.com or by calling 800 330 7348.

Index definitions and important disclosures

An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes. Index comparisons have limitations as volatility and other characteristics may differ from a particular investment.

Real assets blend: 27.5% real estate, 27.5% commodities, 15% infrastructure, 15% resource equities, 10% short-duration fixed income and 5% gold. Real estate: Datastream Developed Real Estate Index through 2/28/05; FTSE EPRA/NAREIT Developed Index thereafter. The Datastream Developed Real Estate Index encompasses listed real estate companies in developed markets and is compiled by Refinitiv Datastream. The FTSE EPRA Nareit Developed Index is an unmanaged market-weighted total return index consisting of many companies from developed markets that derive more than half of their revenue from property-related activities. Commodities: S&P GSCI Index through 7/31/98; the Bloomberg Commodity Total Return Index thereafter. The S&P GSCI Index is a composite index of commodity sector returns representing an unleveraged, long-only investment in commodity futures that is broadly diversified across the spectrum of commodities. The Bloomberg Commodity Total Return Index, formerly known as the Dow Jones-UBS Commodity Index, is a broadly diversified index that tracks the commodity markets through exchange-traded futures on physical commodities, which are weighted to account for economic significance and market liquidity. Infrastructure: 50/30/20 blend of Datastream World Gas, Water & Multi-Utilities, Datastream World Pipelines and Datastream World Railroads through 7/31/08; Dow Jones Brookfield Global Infrastructure Index thereafter. The Datastream World Index Series encompasses global indexes of companies in their respective sectors (World Gas, Water & Multi-Utilities; Materials; Oil & Gas; and Pipelines) and is compiled by Refinitiv Datastream. The Dow Jones Brookfield Global Infrastructure Index is a float-adjusted, market-capitalization-weighted index that measures the performance of globally domiciled companies that derive more than 70% of their cash flows from infrastructure lines of business. Resource equities: 50/50 Blend of Datastream World Oil & Gas and Datastream World Basic Materials through 5/31/08; S&P Global Natural Resources Index thereafter. The Datastream World Index Series encompasses global indexes of companies in their respective sectors (Datastream World Oil & Gas and Datastream World Basic Materials) and is compiled by Refinitiv Datastream. The S&P Global Natural Resources Index includes 90 of the largest publicly traded companies in natural resources and commodities businesses that meet specific investability requirements, offering investors a diversified, liquid and investable equity exposure across three primary commodity-related sectors: Agribusiness, Energy and Metals & Mining. Short-duration fixed income: The ICE BofA 1–3 Year U.S. Corporate Index tracks the performance of USD-denominated investment-grade corporate debt publicly issued in the U.S. domestic market with a remaining term to maturity of less than 3 years. Gold: Gold spot price in USD per Troy ounce. Global stocks: MSCI World Index, a market-capitalization-weighted index consisting of a wide selection of stocks traded in 24 developed markets. U.S. Treasury bonds: The ICE BofA

U.S. Treasury 7-10 Year Bond Index measures the performance of public obligations of the U.S. Treasury that have a remaining maturity of greater than 7 years and less than or equal to 10 years.

Data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated/referenced above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. There is no guarantee that any market forecast set forth in this commentary will be realized. The views and opinions in the preceding commentary are as of the date of publication and are subject to change. Diversification is not guaranteed to ensure a profit or protect against loss. There is no guarantee that actively managed investments will outperform the broader market.

This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment, and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this presentation to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing. The views and opinions expressed are not necessarily those of any broker/dealer or its affiliates. Nothing discussed or suggested should be construed as permission to supersede or circumvent any broker/dealer policies, procedures, rules or guidelines.

Real assets risks: A real assets strategy is subject to the risk that its asset allocations may not achieve the desired risk/return characteristic, may underperform other similar investment strategies, or may cause an investor to lose money. The risks of investing in REITs are similar to those associated with direct investments in real estate securities. Property values may fall due to increasing vacancies, declining rents resulting from economic, legal, tax, political or technological developments, lack of liquidity, limited diversification and sensitivity to certain economic factors such as interest rate changes and market recessions. The market value of securities of natural resource companies may be affected by numerous factors, including events occurring in nature, inflationary pressures and international politics. Global infrastructure securities may be subject to regulation by various governmental authorities, such as rates charged to customers, operational or other mishaps, tariffs and changes in tax laws, regulatory policies and accounting standards. Foreign securities involve special risks, including currency fluctuation and lower liquidity. An investment in commodity-linked derivative instruments may be subject to greater volatility than investments in traditional securities, particularly if the instruments involve leverage. The value of commodity-linked derivative instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. The use of derivatives presents risks different from, and possibly greater than, the risks associated with investing directly in traditional securities. Among the risks presented are market risk, credit risk, counterparty risk, leverage risk and liquidity risk. The use of derivatives can lead to losses because of adverse movements in the price or value of the underlying asset, index or rate, which may be magnified by certain features of the derivatives. No representation or warranty is made as to the efficacy of any particular strategy or fund or the actual returns that may be achieved. Futures trading is volatile and highly leveraged and may be illiquid. Investments in commodity futures contracts and options on commodity futures contracts have a high degree of price variability and are subject to rapid and substantial price changes. Such investments could incur significant losses. There can be no assurance that the options strategy will be successful. The use of options on commodity futures contracts is to enhance risk-adjusted total returns. However, the use of options may not provide any, or may provide only partial, protection from market declines. The return performance of the commodity futures contracts may not parallel the performance of the commodities or indexes that serve as the basis for the options they buy or sell; this basis risk may reduce overall returns.

No representation or warranty is made as to the efficacy of any particular strategy or fund, or the actual returns that may be achieved.

The discussion of the law in the paper was developed and drafted by Fred Reish, a partner in the Benefits & Executive Compensation Practice Group of Faegre Drinker Biddle & Reath LLP. He is not affiliated with Cohen & Steers but has been compensated by us to provide this discussion. Cohen & Steers has also provided factual descriptions, charts, and investment information for this analysis. The summary of law and analysis by the author contained in this white paper are current as of August 2023, are general in nature, and do not constitute a legal opinion of the author that may be relied on by third parties. Readers should consult their own legal counsel for information on how these issues apply to their individual circumstances and to determine if there have been any relevant developments since the date of this paper.

The discussion of investments and their attributes was drafted by Cohen & Steers Capital Management Inc. (and where based on the work, research or conclusions of others, properly attributed to those sources). Cohen & Steers Capital Management, Inc., (Cohen & Steers) is a registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers U.S. registered open-end funds are distributed by Cohen & Steers Securities, LLC, and are available only to U.S. residents.