Enduring structural trends and important portfolio benefits underscore the value of a dedicated diversified real assets allocation.

KEY TAKEAWAYS

- Real assets had a standout year in 2025, with all categories generating double-digit returns.

- Secular trends—such as AI-driven electricity demand, commodity scarcity, and rising government intervention—are creating a multi-decade opportunity for real assets.

- Given the supportive macro backdrop, real assets are positioned as a competitively valued alternative to broad equities, offering diversification, inflation sensitivity and return potential.

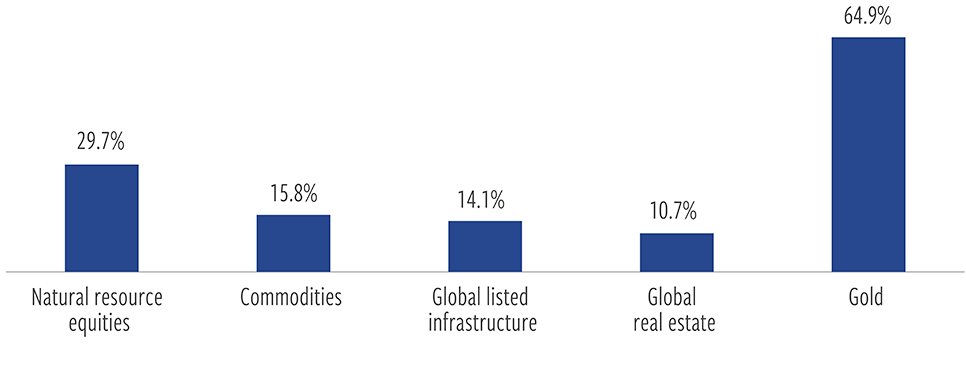

As we look back on 2025, it was clearly a defining year for real assets. While much of the market’s attention remained focused on the AI boom, real assets had a stand-out year, with virtually all categories generating double-digit returns. Natural resource equities led, rising nearly 30% in 2025, followed by commodities up almost 16%, global listed infrastructure up over 14%, and finally global real estate was up just shy of 10%. We also can’t forget about gold, which had a banner year, climbing 64% last year.

Overall, performance was driven by a supportive macro-economic environment, resilient end-market demand, and attractive industry fundamentals. With respect to Cohen & Steers’ real asset strategies, we’re pleased to report we outperformed our respective benchmarks on all fronts. Our real assets multi-strategy outperformed its blended benchmark, and each of the underlying real asset classes outperformed their respective benchmarks. A very strong year from both an absolute and relative return perspective.

Real assets enjoyed strong gains across the board

Category returns in 2025

At December 31, 2025. Source: Cohen & Steers.

Past performance is no guarantee of future returns. An investor cannot invest directly in an index. Index performance does not reflect the reinvestment of dividends and interest income and does not deduct any fees, expenses or taxes. Index comparisons have limitations as volatility and other characteristics may differ from a particular investment.

Compelling secular growth drivers and attractive valuations

Looking beneath the surface, several powerful secular forces continue to shape the opportunity set.

First, the AI-driven surge in electricity demand is emerging as a meaningful tailwind for infrastructure, energy, and natural resource equities. The rapid expansion of data centers and global electrification is driving incremental demand for critical commodities such as copper, uranium and natural gas.

Second, we are witnessing a structural shift from an era of abundance to an era of scarcity. Years of underinvestment in commodity supply, combined with rising global demand, particularly from the growing middle class in emerging markets, have tightened supply-demand balances across many resource markets. This scarcity dynamic underpins what we believe is a multi-decade valuation opportunity for real assets.

Finally, government activism continues to rise. In the U.S. and abroad, governments are increasingly taking direct stakes in critical minerals and strategic resource companies. This intervention is accelerating domestic investment and could provide an additional layer of support for real assets over time.

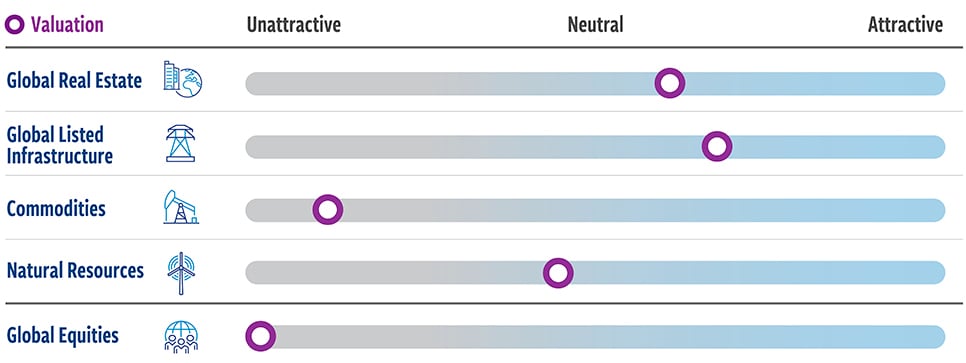

From a valuation standpoint, even with their stand-out performance in 2025, real assets are priced right. Relative to broad equities, many segments are trading at significant discounts, by some measures more than two standard deviations below long-term historical averages. This disconnect creates an attractive entry point for investors to capitalize on these long-term compelling themes taking place within real assets.

Core real asset valuations appear significantly more attractive than global equities

At December 31, 2025. Source: Bloomberg, S&P Xpressfeed and Cohen & Steers.

Valuations reflects the z-score of a proprietary set of valuation metrics, specific to each asset class.

The economic backdrop sets the stage for continued strength

In 2026, our macro-economic outlook remains constructive for real assets. We enter 2026 above consensus on global growth, inflation, and interest rates, and expect economic activity and market returns to broaden after several years of unusually concentrated gains.

We head into this year modestly above consensus on global growth, supported by strength in China and emerging markets, alongside continued resilience in the U.S., with a more accommodative monetary policy backdrop and the potential for incremental fiscal support.

Meanwhile, despite consensus expectations that inflation pressures will continue to moderate, risks remain. While it varies by country, in the U.S., headline inflation has exceeded market expectations by a staggering 220 basis points per year over the past five years and we expect this to continue. We remain above consensus U.S. inflation, with the gap widening by the second half of the year as policy easing and firm service prices keep inflation high even as shelter inflation cools.

On rates, we believe 10-year nominal yields will rise from resilient growth, sticky inflation, and elevated sovereign issuance. In our base case, the increase comes primarily from higher inflation expectations. With respect to real (inflation-adjusted) yields, we expect them to fall over the course of this year to our current year-end 2026 target of 1.75%.

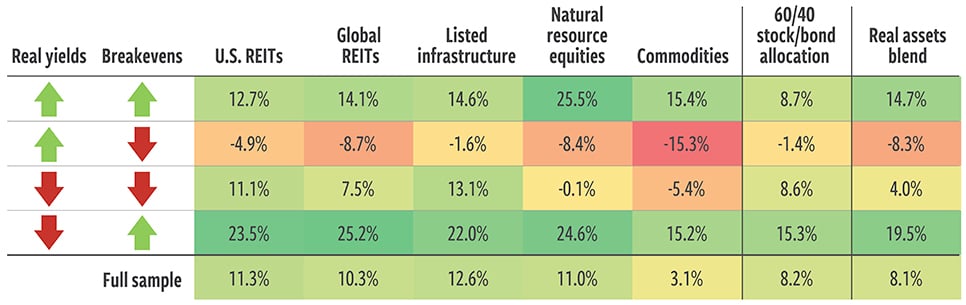

This all points to what we believe is a favorable backdrop for real assets. As you can see on the 4th or bottom row of this table, periods when real (inflation-adjusted) yields fall and inflation breakevens are rising (which is what we anticipate), have historically resulted in strong relative and absolute returns for real assets.

Average annualized 6m rolling total returns based on coincident change in 10yr real yields and breakevens

December 2002 – December 2025

At December 31, 2025. Source: Bloomberg, LSEG Datastream, Cohen & Steers.

Past performance is no guarantee of future returns. Total returns in USD for all assets.

Importantly, if enthusiasm around AI slows, real assets offer a competitively valued alternative—backed by durable secular demand and strong long-term fundamentals.

For investors, the takeaway is clear. Real assets, across resource equities, infrastructure, real estate and commodities, offer a compelling combination of inflation sensitivity, diversification and return potential. Maintaining a strategic allocation can help capture upside from long-term secular trends while providing diversified return levers in an evolving macro environment.

The multi-decade valuation opportunity is already taking shape, and signs of capital rotation into these sectors suggest this is an opportune time.

Thank you for your time. We look forward to navigating the opportunities and challenges of 2026 together.

Data quoted represents past performance, which is no guarantee of future results. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes. Index comparisons have limitations as volatility and other characteristics may differ from a particular investment.

The views and opinions presented are as of the date of publication and are subject to change. There is no guarantee that any market forecast set forth in this document will be realized. This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment.

This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or to account for the specific objectives or circumstances of any investor. We consider the information to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Cohen & Steers does not provide investment, tax or legal advice. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Index definitions

U.S. REITs: FTSE Nareit All Equity REITs Index. Global REITs: FTSE EPRA Nareit Developed Real Estate Index.

Infrastructure: 50/30/20 blend of Datastream World Gas, Water & Multi-Utilities, Datastream World Pipelines and Datastream World Railroads through 12/31/02; Dow Jones Brookfield Global Infrastructure Index thereafter.

Natural resource equities: 50/50 blend of Datastream World Oil & Gas and Datastream World Basic Materials through 12/31/02; S&P Global Natural Resources Index thereafter.

Commodities: Bloomberg Commodity Total Return Index. 60/40 stock/bond allocation: 60% MSCI World Index and 40% ICE BofA US Treasury 7-10 Year Bond Index.

Real assets blend: 27.5% real estate, 27.5% commodities, 15% natural resource equities, 15% infrastructure, 10% short-duration fixed income and 5% gold.

Short-duration fixed income represented by ICE BofA 13 Year U.S. Corporate Index.

Gold represented by the gold spot price in U.S. dollars per troy ounce.

The real assets blend is not representative of an actual portfolio and is for illustrative purposes only.

Risks of investing: Investing involves risk, including entire loss of capital invested. There can be no assurance that the investment strategy will meet its investment objectives. Diversification is not guaranteed to ensure a profit or protect against loss. A real assets strategy is subject to the risk that its asset allocations may not achieve the desired risk return characteristic, underperform other similar investment strategies or cause an investor to lose money. Risks of investing in REITs are similar to those associated with direct investments in real estate securities, including (i) property values may fall due to increasing vacancies, declining rents resulting from economic, legal, tax, political or technological developments, lack of liquidity, limited diversification and sensitivity to certain economic factors such as interest rate changes and market recessions. The value of commodity-linked derivative instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. The use of derivatives presents risks different from, and possibly greater than, the risks associated with investing directly in traditional securities, including market risk, credit risk, counterparty risk, leverage risk and liquidity risk and can lead to losses because of adverse movements in the price or value of the underlying asset, index or rate, which may be magnified by certain features of the derivatives. Securities of natural resource companies may be affected by events occurring in nature, inflationary pressures and international politics. Global infrastructure securities may be subject to regulation by various governmental authorities, such as rates charged to customers, operational or other mishaps, tariffs and changes in tax laws, regulatory policies and accounting standards. Foreign securities involve special risks, including currency fluctuation and lower liquidity.

Futures Trading Is Volatile, Highly Leveraged and May Be Illiquid. Investments in commodity futures contracts and options on commodity futures contracts have a high degree of price variability and are subject to rapid and substantial price changes. Such investments could incur significant losses. The use of options on commodity futures contracts is to enhance risk-adjusted total returns. The use of options, however, may not provide any, or only partial, protection for market declines. The return performance of the commodity futures contracts may not parallel the performance of the commodities or indexes that serve as the basis for the options it buys or sells; this basis risk may reduce overall returns.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, U.S. endowments, foundations and mutual funds. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.

For Investors in the Middle East: This is for information purposes only. It does not constitute or form part of any marketing initiative, any offer to issue or sell, or any solicitation of any offer to subscribe or purchase, any products, strategies or other services nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient wishes to receive further information with regard to any products, strategies other services, it shall specifically request the same in writing from us.