Active REIT managers have historically had success delivering excess returns, capitalizing on the diversity and complexity of the listed real estate universe.

KEY TAKEAWAYS

- Over the past decade, active REIT managers have delivered a measurable advantage over passive strategies, on average.

- Distinct characteristics across 17 property types and dozens of countries provide opportunities for active managers to potentially add value.

- Fundamental research is the foundation for active management, incorporating macro-economic, sector and security-level inputs into portfolio construction.

REITs have historically been fertile ground for active managers

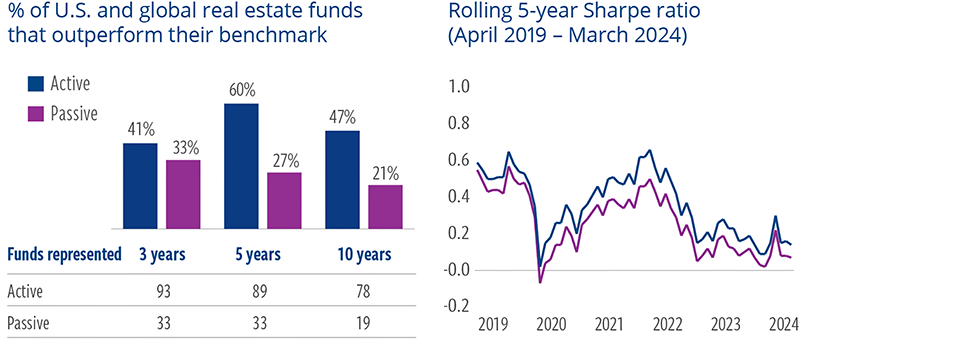

Index investing reached a milestone in early 2024, with assets in passive investment vehicles surpassing actively managed strategies for the first time. But passive isn’t necessarily better. Over the past 10 years, active real estate managers have outperformed their benchmarks at more than twice the rate of passive funds, and the magnitude of excess returns versus passive strategies has often been significant (Exhibit 1).

We believe this advantage stems from the time and resources REIT managers devote to understanding current real estate fundamentals and the factors that may affect listed equity performance. This focus creates the potential for better-quality information, more accurate forecasts and faster implementation of investment ideas, achieved simply because these managers are more attuned to shifting market trends. For example, in the five years ended March 31, 2024, the median U.S. REIT manager proved adept at helping to mitigate the challenging effects of Covid-19 and rising interest rates on certain types of real estate.

EXHIBIT 1

Active REIT managers have a track record of delivering value

At March 31, 2024. Source: eVestment Alliance, Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. There is no guarantee that investors will experience the type of performance reflected above. Data includes current managers with performance records spanning the full period in question. Sharpe ratio is an indication of risk-adjusted performance, represented here by dividing the annualized total return by the standard deviation. See endnotes for additional disclosures.

The modern REIT market offers a diverse opportunity set

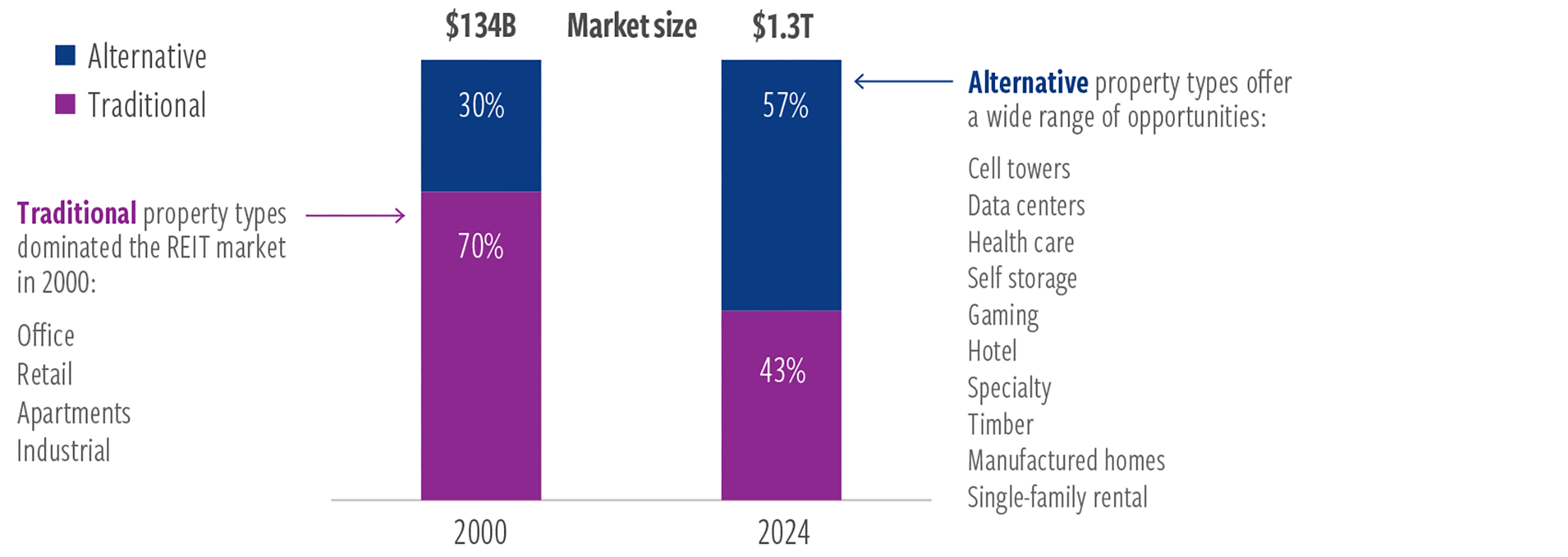

When investors think of commercial real estate, they may envision office buildings, malls, shopping centers and apartments. REIT ownership of these kinds of assets exists, of course. However, REITs have become increasingly specialized in new property types since 2000, shifting the REIT market’s composition away from traditional sectors (Exhibit 2).

For well-resourced managers, these new sectors provide a broad selection of REIT-owned assets for constructing portfolios, many of which have secular growth drivers. These include data centers where companies rent by the kilowatt to connect cloud servers; cell towers that lease space to wireless carriers for 5G networks; high-tech distribution hubs that facilitate next-day shipping on e-commerce orders; climate-controlled food storage facilities; biotech research labs; and senior living centers, just to name a few.

EXHIBIT 2

Alternative sectors make up over half of today’s U.S. REIT market

Size and composition of the modern REIT universe

At March 31, 2024. Source: FTSE Nareit, Cohen & Steers.

Sectors represented by the FTSE Nareit All Equity REITs Index. The information presented above does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. See endnotes for index associations, definitions and additional disclosures.

Active REIT managers can leverage economic and growth opportunities available in the wide array of listed real estate sectors.

Distinct characteristics often produce divergent returns

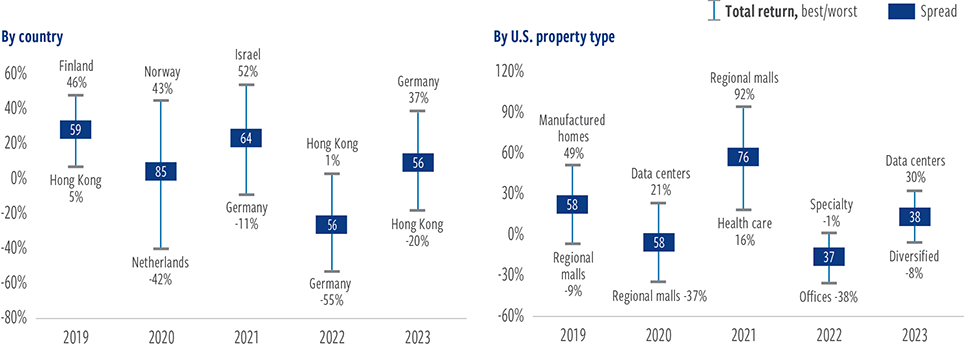

The listed real estate universe encompasses 17 major property types, spanning dozens of developed and emerging markets. Each sector has distinct characteristics, including lease durations, types of tenants, economic drivers and supply cycles. Countries and regions may also have different property cycles, monetary policies and business practices. These factors typically result in a wide dispersion of returns in any given period (Exhibit 3).

The average dispersion in returns between the best- and worst-performing U.S. REIT sectors over the last five years was more than 50% annually. An array of factors can potentially drive returns. Over a typical market cycle, for instance, more economically sensitive sectors with short lease terms, such as hotels or self storage, may outperform in periods of accelerating demand, as they can adjust rents relatively quickly. By contrast, longer- lease sectors like net lease and health care may be more resilient during economic downturns due to their more defensive cash flows.

By focusing on what’s occurring in different companies, property types and countries, active REIT fund managers can emphasize allocations in areas they believe can outperform (and underweight or avoid altogether areas they expect to underperform). By design, passive portfolios are not able to allocate assets to benefit from potential secular growth opportunities, nor can they sidestep potential sector calamities.

EXHIBIT 3

Performance dispersion creates potential for active managers to add value

Best/worst total return (US$)

At December 31, 2023. Source: FTSE Nareit, Cohen & Steers. Sector returns represented by the FTSE Nareit All Equity REITs Index.

Data quoted represents past performance, which is no guarantee of future results. The information presented above does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. See endnotes for index definitions and additional disclosures.

Identifying potential value through fundamental research

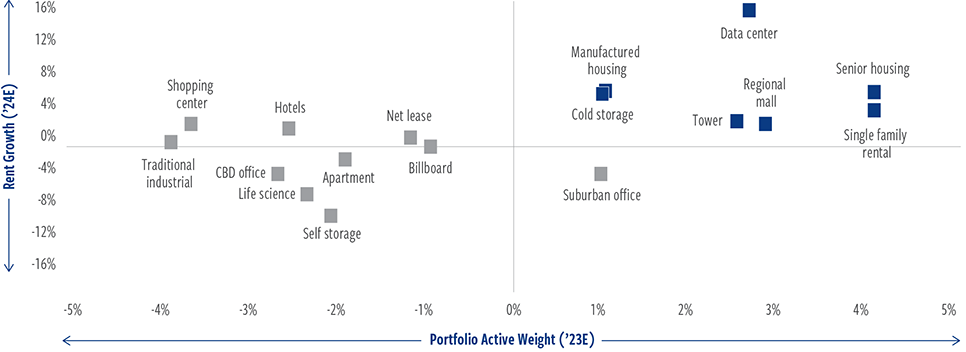

Understanding the many drivers that may affect a real estate company’s financial performance requires a commitment to fundamental research. For example, in a typical year, Cohen & Steers may conduct 300 property visits and 1,300 meetings with management teams, seek local perspectives from independent brokers, and leverage proprietary data sets, such as web scraping tools that provide unit pricing information in real time. Using inputs such as these, plus a view on future supply and demand, a REIT manager can often take a differentiated view of where cash flow and asset values are pointing to in the future. Using inputs such as these, we can often develop a differentiated view of the direction of property cash flows and asset values, identifying securities with upside potential that other equity investors may have underestimated (Exhibit 4).

The listed real estate market is historically inefficient, as generalist and passive investors can collectively dominate ownership. As such, specialist managers can seek to leverage the information advantage they hold—their deeper insights into factors that drive sector and company performance—to uncover unique opportunities.

EXHIBIT 4

Cohen & Steers currently favors sectors with strong pricing power

U.S. REIT sectors 2024E rent growth vs active weights

At March 31, 2024. Source: Morningstar.

Data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. Data is based on a list of representative companies by sector selected by Cohen & Steers as a representative of the market. 2024E rent growth represents Cohen & Steers estimated full-year market-level rent growth. Assumptions based on representative companies by sector. Rent growth assumptions are not guaranteed and actual results could vary materially. Active weights is represented by the Cohen & Steers U.S. Realty Total Return representative portfolio. We believe this is the most appropriate portfolio as it best represents the strategy’s composition and investment objective. See end notes for index associations, definitions and additional disclosures.

ABOUT THE AUTHORS

Jason A. Yablon, Executive Vice President, is Head of Listed Real Estate and a senior portfolio manager for listed real estate securities portfolios and oversees the research process for listed real estate securities.

Index definitions / important disclosures

An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes. Index comparisons have limitations as volatility and other characteristics may differ from a particular investment. Global real estate: The FTSE EPRA Nareit Developed Index is a capitalization-weighted, time-weighted index of companies domiciled in developed markets that derive more than half their revenue from property-related activities. Source: London Stock Exchange Group plc and its group undertakings, including FTSE International Limited (collectively, the “LSE Group”), European Public Real Estate Association (“EPRA”), and the National Association of Real Estate Investments Trusts (“Nareit”) (and together the “Licensor Parties”). © LSE Group 2021. FTSE Russell is a trading name of certain LSE Group companies. “FTSE®” and “Russell®” are a trademark(s) of the relevant LSE Group companies and are used by any other LSE Group company under license. “Nareit®” is a trademark of Nareit, “EPRA®” is a trademark of EPRA and all are used by the LSE Group under license. All rights in the FTSE EPRA Nareit Developed Index and FTSE Nareit All Equity REITs Index or data vest in the Licensor Parties. The Licensor Parties do not accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The Licensor Parties do not promote, sponsor or endorse the content of this communication. U.S. real estate: The FTSE Nareit All Equity REITs Index contains all tax-qualified REITs with more than 50% of total assets in qualifying real estate assets other than mortgages secured by real property that also meet minimum size and liquidity criteria. “FTSE®” is a trademark of the LSE Group and is used by FTSE International Limited (“FTSE”) under license. “NAREIT®” is a trademark of the Nareit. All rights in the FTSE Nareit All Equity REITs Index and FTSE EPRA Nareit Developed Index (the “Indexes”) vest in FTSE and Nareit. Neither

FTSE, nor the LSE Group, nor Nareit accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the FTSE or Nareit is permitted without the relevant FTSE’s express written consent. FTSE, the LSE Group, and Nareit do not promote, sponsor or endorse the content of this communication.

There is no guarantee that an actively managed investment strategy will outperform the broader market index. These materials are provided for informational purposes only and reflect the views of Cohen & Steers, Inc. and sources believed by us to be reliable as of the date hereof. No representation or warranty is made concerning the accuracy of any data compiled herein, and there can be no guarantee that any forecast or opinion in these materials will be realized. This is not investment advice and may not be construed as sales or marketing material for any financial product or service sponsored or provided by Cohen & Steers, Inc. or any of its affiliates or agents.

No representation or warranty is made as to the efficacy of any particular strategy or fund or the actual returns that may be achieved. Prospective investors in any Cohen & Steers fund should read its prospectus carefully for additional information including important risk considerations and details about fees and expenses.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority of the United Kingdom (FRN 458459). Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.

For readers in the Middle East: This document is for information purposes only. It does not constitute or form part of any marketing initiative, any offer to issue or sell, or any solicitation of any offer to subscribe or purchase, any products, strategies or other services nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. If the recipient of this document wishes to receive further information regarding any products, strategies or other services, it shall specifically request the same in writing from us.