Rising energy consumption is creating a broad and complex opportunity set for investors. No single fuel or technology can meet the world’s needs alone, elevating the importance of a diversified, flexible approach.

KEY TAKEAWAYS

- The energy buildout imperative

Surging global energy demand, driven by AI, population trends and economic growth, requires massive investment. Meeting these needs will require expanding both traditional and alternative energy sources. - 5 themes in scaling a resilient energy mix

Natural gas, nuclear power, oil sands, energy security and grid infrastructure each play distinct roles, supporting reliability and decarbonization as investment opportunities expand across the full energy value chain. - Better results via diversification and active management

A flexible, active strategy across traditional and alternative energy allows for dynamic allocation, helping to capture opportunities (amid wide return dispersion) while supporting stronger growth potential.

The energy buildout imperative

The global economy is entering a period of extraordinary energy usage. Meeting surging demand will require more energy from every viable source—not a trade-off between traditional and alternative fuels, but a simultaneous expansion of both.

Global energy consumption is rising at a pace rarely seen, with demand expected to reach unprecedented levels through at least mid century (Exhibit 1). While the rapid growth of artificial intelligence and need for data centers is a powerful contributor, this is not a single factor story. Population growth, economic expansion and accelerating electrification across households, industry and transportation are collectively driving a sustained increase in energy use across both developed and emerging markets.

Together, these forces underscore a central reality: Global energy demand is rising faster than any one fuel or technology can grow to meet it. Power systems must scale quickly while maintaining reliability, affordability and progress toward decarbonization objectives.

EXHIBIT 1

The need for power is growing faster than ever

Projected global electricity demand growth to 2050

At May 31, 2026. Source: International Energy Agency, Cohen & Steers.

Current estimate based on consumption data from 2024..

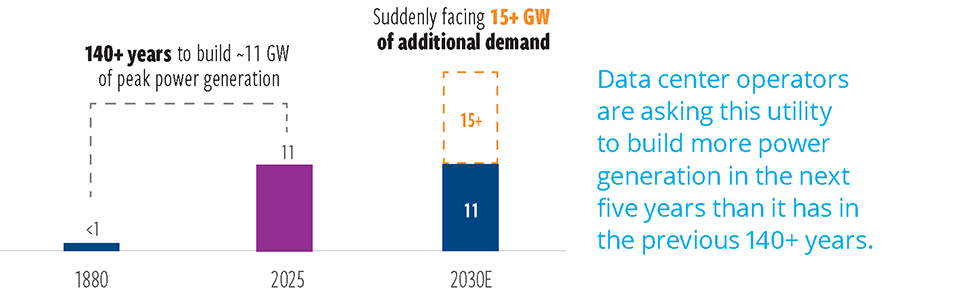

Meeting incremental electricity needs—particularly those associated with data centers will require additions to power generation capacity that far exceed historical build rates. In one illustrative case, a Midwestern utility is being asked to add more generation capacity before the end of the decade than it built over the prior century. This scale highlights a practical constraint: Relying on any single energy source is neither realistic nor sufficient (Exhibit 2).

EXHIBIT 2

Data centers will be a major contributor to power demand

Case study: Midwest utility serving Kansas and Missouri

At May 31, 2026. Source: Carbon Collective, Cohen & Steers.

The world will continue to adopt alternative forms of energy, but the transition toward alternatives does not mean the imminent obsolescence of traditional fuels. While solar, wind and nuclear power are expected to grow rapidly off a small base, oil and natural gas consumption will also continue to rise, in absolute terms, over the next few decades (Exhibit 3).

Alternatives are critical to decarbonization and long-term sustainability, but traditional energy remains essential for reliability, scale and baseload power, particularly as intermittent renewables expand. The central challenge ahead is mobilizing sufficient capital, infrastructure and innovation across the entire energy spectrum to support a more energy intensive global economy. The future of energy is less about replacement and more about expansion— adding every viable source to meet rapidly rising needs.

EXHIBIT 3

Rumors of traditional energy’s death have been greatly exaggerated

Total projected global energy consumption by fuel (2024–2035, in exajoules)

At May 31, 2026. Source: International Energy Agency.

Forecasts are inherently limited. There is no guarantee that any market forecast will be realized.

5 themes in scaling a resilient energy mix

Rising global demand is creating opportunities across the energy value chain. Below, we examine key investment themes spanning both traditional and emerging sources of supply.

1. Natural gas: The bridge to renewable energy

Natural gas plays a constructive role in the transition to a renewable energy economy by bridging today’s fossil fuel–dominated mix and a more renewable future. While wind and solar capacity are expanding rapidly, their growth remains constrained by intermittency, storage limitations and grid integration challenges. Natural gas helps offset these limitations, supporting system reliability as longer-term solutions continue to scale.

Natural gas is a cleaner-burning fuel than coal, and it is one of the most quickly deployable ways to lower the carbon intensity of electricity systems without sacrificing reliability or affordability. It also enhances grid stability. Gas fired power plants can ramp production up or down quickly to balance fluctuations in wind and solar output, helping utilities manage peak demand, reduce outage risk and limit price volatility. This operational flexibility makes it easier for grid operators to incorporate higher levels of renewable generation over time.

From an investment perspective, rising gas demand has implications well beyond producers. Gas distribution and midstream energy companies that operate pipelines, storage facilities and liquefied natural gas (LNG) infrastructure stand to benefit as gas volumes increase. Electric utilities that use gas-fired generation also play a central role, providing capacity that supports renewable integration while meeting growing electricity demand.

EXHIBIT 4

Natural gas will play a key role as renewables continue to scale

Total energy consumption by fuel type to 2040

At May 31, 2026. Source: Our World in Data, Cohen & Steers.

Past performance is no guarantee of future results. Forecasts are inherently limited. There is no guarantee that any market forecast will be realized. The forecasts above are based on policies currently in place. Renewables include wind, solar, hydropower, nuclear, biofuels and other sources.

2. The nuclear power renaissance is just getting started

Nuclear power represents another key supply source for baseload, low- emission energy. Unlike wind and solar power, whose output depends on weather conditions and daylight (and therefore requires extensive backup capacity and grid-scale storage), nuclear delivers continuous, around-the- clock electricity.

Although constructing traditional, large-scale nuclear plants is expensive, once built they have low operating costs and very long lifespans, delivering affordable electricity for decades. Fuel accounts for only a small share of generation cost (much lower than for natural gas or coal), helping keep nuclear power prices stable and insulated from commodity price volatility. By providing dependable capacity, nuclear power can also lower total system costs by reducing the need for costly storage, peaking resources and standby generation that a renewables–heavy system would otherwise require.

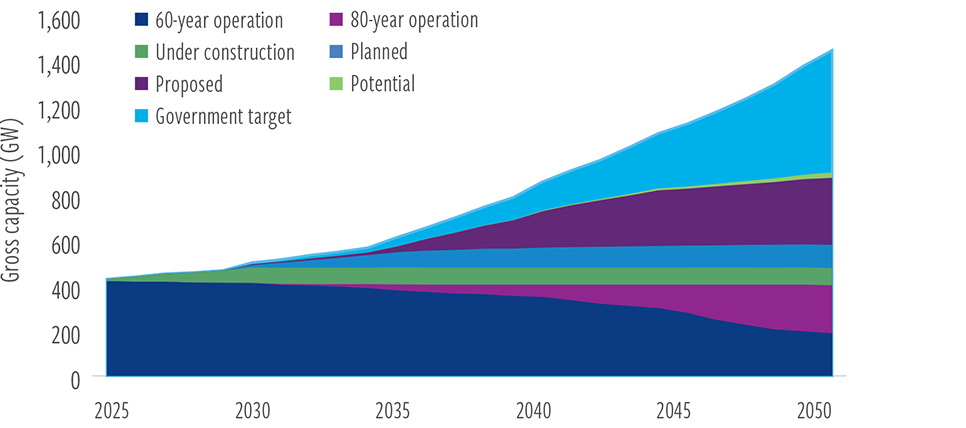

Public concerns—particularly about nuclear waste disposal—remain, but support for nuclear power is expanding, including for small modular reactors that may be built economically and fairly quickly. Approximately 440 reactors are currently in operation, totaling roughly 400 gigawatts (GW) of capacity and supplying about 9% of global electricity. Nuclear’s market share is likely to ramp up meaningfully over time. Another 76 GW of capacity is under construction, with more than 300 GW additional capacity announced or proposed—enough to more than than double nuclear generation capacity to roughly 880 GW by 2050, though still well short of government targets (Exhibit 5).

We see attractive opportunities in select nuclear-related companies, including uranium suppliers, manufacturers of nuclear fuel components and leading nuclear power-generating electric utilities.

EXHIBIT 5

The world is committing to new nuclear capacity

Estimated global nuclear capacity to 2050

At January 21, 2026. Source: World Nuclear Association.

Forecasts are inherently limited. There is no guarantee that any market forecast will be realized.

3. Oil sands: Long-lived reserves

For years, many investors have assumed that oil consumption will decline as the world turns to alternatives. As a result, Canadian oil sands producers were largely written off as essentially annuities with finite (15–20 year) lifespans.

In reality, however, oil sands companies stand out as attractive long-term investments.

Oil sands production involves extracting a thick, heavy substance known as bitumen, either through surface mining or by heating it underground so that it can be pumped to the surface where it is then upgraded into synthetic crude oil. Producers’ vast, long lived (100+ years) reserves enable decades of stable output without the capital-intensive “drilling treadmill” of shale fields, where first-year production decline rates are often greater than 40% (Exhibit 6). This gives oil sands producers a low-cost, “no-decline” production profile, which translates into strong free cash flow generation, high capital efficiency and healthy balance sheets supporting reliable shareholder returns.

Many oil sands operators are also vertically integrated, combining mining with on-site upgrading, allowing them to capture more value per barrel and operate at high utilization rates, a structure that bolsters resilience across commodity price cycles.

While oil sands investments are not without risks—notably, exposure to crude price volatility and evolving environmental policies—their durable, low- cost production base allows them to navigate these challenges. As investor perceptions continue to evolve, oil sands companies could see higher valuation multiples and enterprise values over time.

EXHIBIT 6

Oil sands require less ongoing drilling to sustain production

Illustrative crude oil production curves

At May 31, 2026. Source: Canadian Association of Petroleum Producers, Cohen & Steers..

Past performance is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. Decline rates represents how quickly production decreases, as a percentage of peak production, on a year-over-year basis.

4. The importance of energy security

In an era of rising geopolitical tension, energy security is no longer a background consideration but rather a central driver of risk and return. Concentrated supply chains and political instability can quickly ripple through energy markets, with broad consequences for inflation, growth and asset performance.

The Russia–Ukraine war disrupted natural gas flows to Europe, sending energy prices sharply higher and forcing governments into costly emergency responses. More recently, the U.S.–Iran war delivered a similar lesson on a global scale. The risk of disruption alone was enough to push oil and LNG prices higher. Higher prices feed inflation, strain trade balances and weigh on growth, even in the absence of outright shortages.

Investing in companies with operations in politically stable energy producing regions has taken on added importance (Exhibit 7). Oil from the U.S. and Canada, offshore production from Brazil, and LNG from Australia, for example, offer diversification away from higher risk regions. These supplies benefit from stable institutions, transparent regulation and well-established infrastructure, making them reliable foundations for long-term energy planning.

Energy security risks extend beyond fossil fuels. Just as gas and oil supply chains can be disrupted, nuclear energy introduces its own security dependencies. Nearly 40% of global uranium supply comes from a single country, Kazakhstan. This concentration creates another potential chokepoint, bolstering the appeal of Canadian and Australian producers.

Self-sufficiency is another part of the security story. We expect to see accelerating investment in domestic renewables such as wind and solar in Europe and other areas heavily reliant on energy imports. Locally sourced power can act as a buffer against future price and supply shocks.

EXHIBIT 7

Energy security concerns elevate the value of supply from politically stable regions

Oil & gas exporting countries with low conflict risk

At May 31, 2026. Source: Cohen & Steers.

Countries with widely recognized strong governance and low conflict risk (e.g., OECD members or high World Bank governance scores), and whose oil/gas exports do not depend on the Persian Gulf’s Strait of Hormuz.

5. The energy grid buildout

The U.S. electrical grid sits at the center of two powerful forces:

- Power demand surge—Data centers, electrified transportation and advanced manufacturing are driving a step change in electricity consumption.

- Supply complexity—Wind and solar penetration is increasingly reordering grid dynamics, requiring significant upgrades to manage variability and system efficiency.

Together, these trends are stretching the limits of an aging grid and driving a multi-year wave of capital spending.

Much of today’s transmission and distribution network was built decades ago to deliver one-way power from centralized plants. That model no longer fits. Renewable generation is often far from population centers and is intermittent by nature. Integrating these resources requires new transmission lines, grid-scale storage, advanced substations and digital controls to balance supply and demand. Utilities must also harden existing infrastructure to improve reliability and resilience as extreme weather events become more common.

Global annual grid capital expenditures alone are expected to nearly triple, increasing from around $270 billion in 2016–2022 to roughly $775 billion in the 2031–2040 period (Exhibit 8). This buildout creates a broad investment opportunity across regulated utilities, grid equipment manufacturers and infrastructure service firms. Equipment makers that supply power electronics and grid software stand to see sustained demand as utilities modernize their systems. Engineering, construction and services firms add another layer of exposure as projects move from planning to execution.

EXHIBIT 8

Record levels of capital are being committed to transmission, distribution and grid resilience

Average annual investment in grids and renewables ($ billions)

At September 30, 2023. Source: International Energy Agency, Cohen & Steers.

Forecasts are inherently limited. There is no guarantee that any market forecast will be realized.

Better results through diversification and active management

Traditional energy strategies focus primarily on oil, gas and consumable fuels companies, with smaller allocations to energy equipment and services. Alternative energy strategies, by contrast, typically concentrate on electrical equipment manufacturers, independent power and renewable electricity producers, electric utilities, and companies that make semiconductors and related equipment. These two universes are driven by fundamentally different forces. Historically, when one segment has outperformed, the other has often lagged.

Adopting an either/or approach, investing exclusively in traditional or alternative energy, can exclude companies benefiting from the world’s energy demands, potentially resulting in significant missed opportunities. We believe that allocating across the full energy value chain—spanning producers, enablers and developers shaping both traditional and alternative energy markets—can improve returns while helping to dampen volatility (Exhibit 9).

EXHIBIT 9

Investing across traditional and alternative energy creates a superior portfolio

10-year performance statistics

At March 31, 2026. Source: Cohen & Steers.

Past performance is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. An investor cannot invest directly in an index, and index performance does not reflect the deduction of any fees, expenses or taxes. Index comparisons have limitations, as volatility and other characteristics may differ from a particular investment. (1) Sector composition of the Energy Select Sector Index is represented by the passive ETF directly tracking the index. (2) Sector composition of the Global Clean Energy Transition Index is represented by the passive ETF directly tracking the index. Volatility is measured by standard deviation, which shows how much variation, or dispersion, exists from the average. Sharpe ratio is a measure of risk-adjusted return, calculated by subtracting the risk-free rate from a return and dividing that result by the standard deviation. The higher the Sharpe ratio, the higher the risk-adjusted return. Sector weights may not sum due to rounding.

At a broad level, traditional energy equities are often closely linked to movements in crude oil prices, while clean energy shares tend to be more sensitive to interest rates, capital costs and policy decisions. These differing return drivers contribute to wide performance dispersion across the full energy universe. At the company level, factors such as technological change, operational execution and balance sheet strength can also play a meaningful role in driving returns (Exhibit 10).

EXHIBIT 10

Return dispersion favors active management

Annual variation in stock returns for alternative and traditional energy

At March 31, 2026. Source: Morningstar, Cohen & Steers.

Past performance is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The information above does not reflect information about any fund or account managed or serviced by Cohen & Steers, and there is no guarantee investors will experience the type of performance reflected above. (1) Alternative energy represented by the largest passive ETF that tracks the S&P Global Clean Energy Transition Index. (2) Traditional energy represented by the largest passive ETF that tracks the S&P Energy Select Sector Index.

Why active management matters

Pairing passive traditional and alternative strategies is an imperfect solution to energy investing. Passive approaches are fairly static and typically track market capitalization–weighted indexes, meaning the largest constituents disproportionately shape performance, irrespective of underlying fundamentals. Additionally, attractive energy-related opportunities outside of those passive benchmarks may be overlooked.

Capturing the full opportunity requires adaptability. A dynamic, fundamentals-driven approach enables capital to be allocated toward areas offering more attractive valuations or stronger earnings prospects. Beyond sector positioning, disciplined stock selection across the capitalization spectrum can also be an important contributor to excess return.

In our view, a single, actively managed portfolio from a specialist manager provides a more effective way to navigate this complexity. Flexible, high-conviction investing across the full energy value chain can help investors pursue attractive returns while managing downside risk in a rapidly evolving market.

ABOUT THE AUTHORS

Tyler Rosenlicht, Senior Vice President, is a portfolio manager for Global Listed Infrastructure and serves as Head of Natural Resource Equities.

Index definitions and important disclosures

An investor cannot invest directly in an index, and index performance does not reflect the deduction of any fees, expenses or taxes.

Past performance is no guarantee of future results. There is no guarantee that any historical trend illustrated/referenced above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. There is no guarantee that any market forecast set forth in this commentary will be realized. The views and opinions in the preceding commentary are as of the date of publication and are subject to change.

Diversification does not ensure a profit or guarantee to protect against loss. There is no guarantee that actively managed investments will outperform the broader market.

This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment, and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this presentation to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing. The views and opinions expressed are not necessarily those of any broker/ dealer or its affiliates. Nothing discussed or suggested should be construed as permission to supersede or circumvent any broker/dealer policies, procedures, rules or guidelines.

Energy risk considerations: Investing involves risk, including entire loss of capital invested. There can be no assurance that the investment strategy will meet its investment objectives. Diversification does not ensure a profit nor guarantee protection against loss. An investment in the energy sector involves risks that differ from a similar investment in equity securities, such as common stock, of a corporation. Investors will be subject to more risks related to the energy sector than if the Fund were more broadly diversified over numerous sectors of the economy. A downturn in the energy sector of the economy could have a larger impact on the Fund than on an investment company that does not concentrate in the sector. At times, the performance of securities of companies in the sector has lagged the performance of other sectors or the broader market as a whole. Energy sector investments can be volatile due to fluctuations in commodity prices, availability of resources, slowdowns in construction, reduced demand for energy products, regulatory changes, extreme weather or natural disasters, rising interest rates

and geopolitical events. Special risks of investing in foreign securities include (i) currency fluctuations, (ii) lower liquidity, (iii) political and economic uncertainties, and (iv) differences in accounting standards. Certain foreign securities may represent small- and medium-sized companies, which may be more susceptible to price volatility and less liquid than larger companies. The Fund is classified as a “non-diversified” fund under the federal securities laws because it can invest in fewer individual companies than a diversified fund. However, the Fund must meet certain diversification requirements under the U.S. tax laws.

No representation or warranty is made as to the efficacy of any particular strategy or the actual returns that may be achieved.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.

For recipients in the Middle East: This document is for informational purposes only. It does not constitute or form part of any marketing initiative or any offer to issue or sell (or any solicitation of any offer to subscribe or purchase) any products, strategies or other services, nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this document wishes to receive further information with regard to any products, strategies or other services, it shall specifically request the same in writing from us.

All investing involves risk. Loss of principal is possible.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus or summary prospectus with this and other information about the Fund, please call (866) 737-6370. Read the prospectus or summary prospectus carefully before investing.

Foreside Fund Services, LLC, is the distributor of Cohen & Steers active ETFs. Cohen & Steers Securities, LLC is the distributor of Cohen & Steers mutual funds. Foreside Fund Services, LLC, is not affiliated with Cohen & Steers.