We believe a blended strategy has the potential to improve returns over core allocations.

Key takeaways:

- The current real estate cycle is following a familiar script; Listed real estate rebounded since its low 18 months ago, and private real estate is following suit with three consecutive quarters of positive returns.

- We believe combining listed and private real estate in one strategy to tactically allocate between the asset classes can lead to higher returns and reduced risk because of this lead-lag dynamic.

- Combining actively managed listed real estate and core private real estate can also provide investors with improved liquidity, greater diversification, and the potential for alpha from an allocation to an active listed REIT strategy.

Transcript

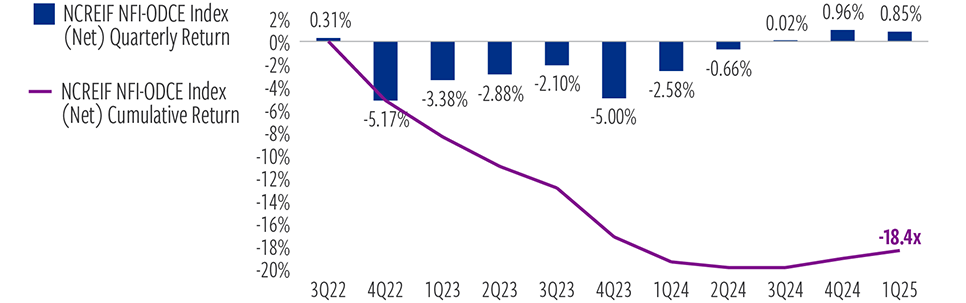

The current real estate cycle is following a familiar script.

After declining well ahead of private values, listed REITs have risen sharply from their October 2023 lows.

Meanwhile, unlevered private real estate values have notched three consecutive quarters of positive total returns after dropping around 20% over the prior seven quarters.

We believe the NFI-ODCE Index bottomed in 2Q 2024

At March 31, 2025. Source NCREIF, Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. There is no guarantee that any market forecast set forth in this presentation will be realized. (1) Private real estate represented by the NCREIF NFI-ODCE Index (Net).

This is not surprising. While listed REITs and private real estate generally move together over long periods of time, listed REITs historically lead private real estate repricing in both downturns and recoveries, particularly at market turning points.

This lead-lag dynamic in real estate investing because it creates pricing differential opportunities for investors.

As listed securities, REITs reflect changes in expected economic and capital cost trends on a more real-time basis.

In contrast, private real estate values adjust much more slowly as declining transaction volumes can limit transparency, while appraisal valuations are inherently lagged.

The challenge we see is that not enough investors optimize their allocations to listed and private real estate to take advantage of these tactical valuation mismatches.

Too often, investors view their listed and core real estate allocations in false silos.

However, blending listed and private real estate allocations can lead to higher returns, reduced risk and lower drawdowns over a full cycle when compared to core private real estate.

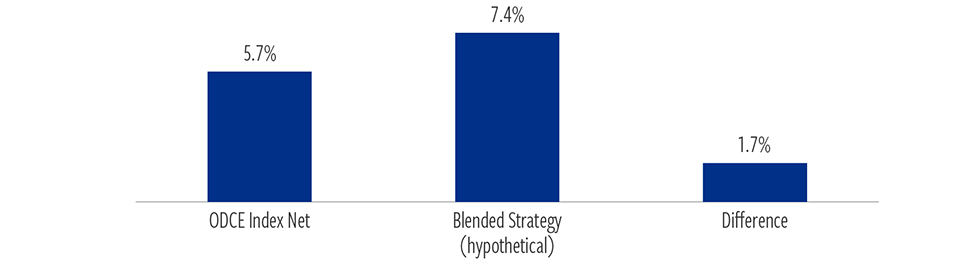

Let’s use a portfolio of 35% listed real estate and 65% private real estate as an example.

That blended portfolio returned 7.4% a year since 1989, while a core portfolio returned 5.7% over the same time period.

And that outperformance is not accounting for the alpha that we believe an actively managed REIT allocation and tactically allocating between listed and private can add to a blended portfolio.

Listed + private real estate has outperformed private real estate alone

At: 3/31/25. Source: Bloomberg, NCREIF, Cohen & Steers.Data quoted represents past performance, which is no guarantee of future results. Private Real Estate represented by the NCREIF Fund Index—Open-End Diversified Core Equity Index (NFI-ODCE) – Net Total Returns. Blended strategy represented by the Cohen & Steers U.S. Realty Total Return Composite – Net Returns.

There are other benefits, too.

Combining actively managed listed real estate and core private real estate can provide investors with improved portfolio-level liquidity.

Private and listed real estate together also offers greater diversification across sector and property types.

Listed REITs provide access to next-generation REIT sectors, such as data centers, cell towers and health care facilities.

Core offers exposure to traditional ODCE sectors, such as industrial and residential. This can provide better diversification, portfolio construction and positioning for future growth.

Overall, we believe a blended strategy has the potential to improve returns over core allocations for three reasons

1) The benefit of blending listed and private together

2) The potential for alpha from an allocation to an active listed REIT strategy

3) The ability to tactically allocate between the asset classes.

What’s more, consider that when it comes to portfoilios comprising just core allocations, liquidity has been constrained and tends to tighten at times of need. Legacy core/ODCE managers are materially overweight pressured property sectors

This recognition of the power of listed and private real estate is what prompted Cohen & Steers to partner with IDR Investment Management to launch a real estate strategy designed to tactically allocate to both listed real estate securities and core private real estate in a single portfolio.

Cohen & Steers has nearly four decades of leadership in listed real estate management.

IDR has a patented process to replicate the NCREIF ODCE Fund Index.

Investors want their private and listed allocations to be complementary.

This strategy recognizes the power of listed and private together.

ABOUT THE AUTHORS

Jon Cheigh, President & Chief Investment Officer, leads the investment department.

Data quoted represents past performance, which is no guarantee of future results.

Performance of blended portfolio measured from 12/31/1989 to 12/31/2024. Source: Bloomberg, NCREIF, Cohen & Steers. (1) Listed U.S. REITs represented by the FTSE Nareit All Equity REITs Index. (2) Private Real Estate represented by the NCREIF Fund Index—Open-End Diversified Core Equity Index (NFI-ODCE) – Net Total Returns (3) Blended portfolio represented by the Cohen & Steers U.S. Realty Total Return Composite – Net Returns.

There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend might begin. Index comparisons have limitations as volatility and other characteristics may differ from a particular investment. This material is for informational purposes and reflects prevailing conditions and our judgment as of this date, which are subject to change. There is no guarantee that any market forecast set forth in this presentation will be realized. This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment, and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or to take into account the specific objectives or circumstances of any investor. We consider the information in this presentation to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Risks of investing

Real estate securities: Risks of investing in real estate securities are similar to those associated with direct investments in real estate, including falling property values due to increasing vacancies or declining rents resulting from economic, legal, political or technological developments, lack of liquidity, limited diversification and sensitivity to certain economic factors such as interest rate changes and market recessions. Foreign securities involve special risks, including currency fluctuations, lower liquidity, political and economic uncertainties, and differences in accounting standards. Some international securities may represent small- and medium-sized companies, which may be more susceptible to price volatility and may be less liquid than larger companies. No representation or warranty is made as to the efficacy of any particular strategy or fund or the actual returns that may be achieved. Private real estate: Private real estate has historically experienced significant fluctuations and cycles in value. The marketability and value of direct real estate investments will depend on many factors, and the ultimate performance of private real estate investments will be subject to the varying degrees of risk generally incident to the ownership and management of real estate generally. For example, revenues and asset values may be adversely affected by changes in general or local economic conditions and/or securities markets, availability of credit, the quality of the management of each property, changing default and foreclosure rates, the financial condition of tenants, buyers and sellers of properties, competition from prospective buyers for, and sellers of, other similar properties, changes in interest rates and in the availability, cost and terms of financing, the impact of present or future environmental legislation and compliance with environmental laws, changes in tax rates and other operating expenses, adverse changes in governmental laws, regulations and fiscal policies, energy and supply shortages, changes in the relative popularity of properties as an investment, acts of God, acts of war, terrorism, epidemics and pandemics, vandalism or civil unrest, adverse changes in zoning laws, availability and costs of insurance, and other factors beyond the control of Cohen & Steers. No representation or warranty is made as to the efficacy of private real estate investing or the actual returns that may be achieved.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers