While market share will continue to grow for alternative energy, we remain in a “more of everything” environment, which is creating attractive investment opportunities across the energy landscape.

KEY TAKEAWAYS

- Energy demand estimates continue to rise

In 2024, we estimated that energy demand would grow well beyond consensus estimates. We were correct, and we underestimated how much growth is ahead. - Both traditional and alternative energy will play meaningful roles

Alternative energy market share is projected to double over the next two decades, but traditional energy will also see an increase in consumption, with traditional (ex-coal) volumes increasing 23% in aggregate, according to our forecasts. - Pairing traditional and alternatives creates superior investment outcomes

The energy industry is changing dramatically, with new technologies coming to market, old technologies facing obsolescence, and companies reacting to significant disruption. The old definition of energy is now obsolete.

Working together

When we first published this paper in 2024, conversations surrounding the world’s energy resources seemed exceptionally controversial. We believe that debate has largely ended, with a more common acceptance of an “energy addition” story—the need for both alternative and traditional forms of energy to meet the world’s growing demand. Market share will grow for alternative energy, but we remain in a “more of everything” environment.

Energy resources

Traditional

- Biomass

- Coal

- Crude oil

- Natural gas

Alternatives

- Hydrogen

- Nuclear

- Solar

- Wind

- Other clean forms of energy

Alternative energy, thanks to technology and global policy support, has taken center stage and will be the biggest growth driver going forward. Yet, traditional energy sources will continue to dominate market share over the next 20 years, given the benefits of in-place infrastructure and the reliability of these assets.

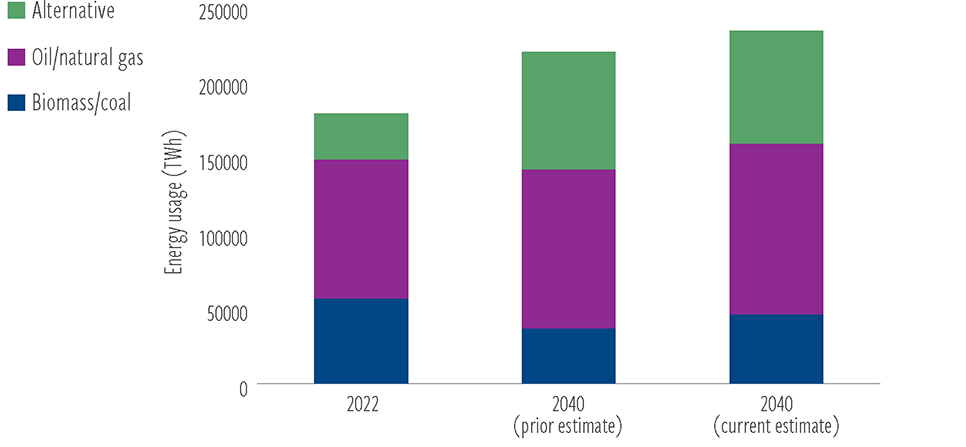

Global energy consumption is set to reach unprecedented levels in the coming years—with our estimates now significantly higher than even two years ago—driven by factors such as a growing and increasingly prosperous global population and the need to power the growth of artificial intelligence (AI). The world needs both traditional and alternative energy to meet this demand (Exhibit 1), and we believe this will create attractive opportunities across the investment landscape.

EXHIBIT 1

Traditional energy will continue to satisfy the bulk of energy

needs, while alternatives will see staggering growth

At March 31, 2026. Source: Energy Statistical Review of World Energy (2023), Vaclav Smil (2017), Our World in Data, Bloomberg and Cohen & Steers estimates.

There is no guarantee that any market forecast set forth in this presentation will be realized. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin.

For the market to satisfy growth requirements and offset desired declines in “dirtier” sources of energy, such as coal, it must continue to complement alternative energy with selected traditional energy sources. In fact, it is our belief that traditional energy will still need to make up ~65% of total energy usage in 2040.

To be clear, the marketplace cannot and will not be dependent on one energy source or the other. With the exception of coal, we are in a “more of everything” world for the next few decades.

The drivers of energy demand

Energy demand can be modeled by making three key assumptions:

- Population growth ➔ more people = more demand for energy, all else equal

- Economic growth ➔ bigger economy = more demand for energy, all else equal

- Energy intensity of the economy ➔ The efficiency of the global economy at converting energy inputs into economic growth.

Population growth

In our last report, our macroeconomic forecasts assumed a deceleration in global population growth from an average of 1.2% in the last two decades to an average of 0.7% in the next two decades. We currently assume 0.9% population growth through 2040 given changing global demographics, resulting in a global population of 9.4 billion people in 2040. All else equal, more people equals more energy demand.

Economic growth

We previously forecast a deceleration in global real GDP growth from 3.1% (2000–2021) to 2.7% through 2040. We maintain this long-term expectation. Though growth is slowing, the real economy will continue to rise, again requiring more energy.

Energy intensity of economic growth

The most difficult part of the equation to estimate is the energy intensity of economic growth. Or, said differently, how effective are we at converting a unit of energy input into a unit of economic output? The world has undergone a robust, long-term improvement in energy efficiency. In 1965, energy/GDP was 3.66, which improved to 1.93 in 2025. In the last 50 years, energy intensity has declined by almost 50%.

In our last publishing, we assumed that we would continue to improve our energy efficiency at an accelerating rate. New technologies, government mandates, and consumer preferences rewarding efficiency would drive us to 1.54 energy/GDP by 2040. Now, though we are still getting more energy efficient, we believe it is going to be a slower rate of improvement, ending 2040 at 1.58. Though this is only marginally worse than prior assumptions, it has a big impact on total energy demand.

The drivers of the change in energy intensity are major economic trends—AI, reindustrialization and the rebounding of the HALO economy (“heavy assets, low obsolescence”). Over the next several years, we believe data centers, which are key components of AI infrastructure, will a be larger source of U.S. power demand growth than commercial and residential activity combined. Globally, the International Energy Agency estimates that data center electricity consumption will more than double to around 945 terawatt-hours

(TWh) by 2030. For perspective, that is more than Japan’s total electricity consumption today. The economy is seeing energy intensity become more impactful than before.

Putting the demand picture together

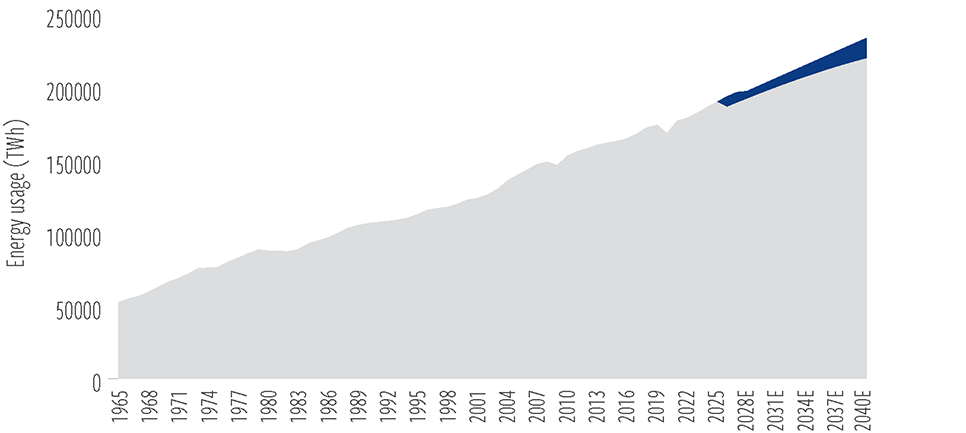

These assumptions point to one clear conclusion: Even as the world becomes more energy efficient, the absolute demand for energy will continue to rise for at least the next two decades (and likely well beyond). In 2024, we assumed 2040 energy demand would total 220,000 terawatt-hours, which we now upgrade to 234,000 (+6%), as indicated in Exhibit 2. This compares with a current demand of 186,400 in 2025.

EXHIBIT 2

The demand for energy is rising steadily

Annual usage is set to eclipse 200,000 TWh by early 2030s

At March 31, 2026. Source: Energy Institute Statistical Review of World Energy 2023, Vaclav Smil (2017), Our World in Data, Bloomberg, and Cohen & Steers estimates.

There is no guarantee that any market forecast or investment objective set forth in this presentation will be realized. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin.

Estimates for energy demand growth in coming years have continued to exceed previous expectations.

Our supply forecasts: How to satisfy the growing demand for energy

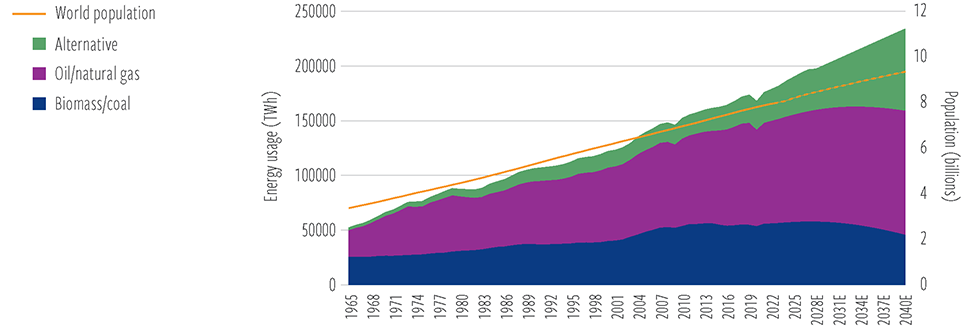

Despite the emergence of alternative resources, the demand for traditional energy will also increase meaningfully in the coming years to satisfy the growth in energy consumption (Exhibit 3).

EXHIBIT 3

The supply side of energy consumption will undergo marked changes in the coming two decades

We believe alternative energy will see significant market share gains

At March 31, 2026. Source: Bloomberg, Energy Institute Statistical Review of World Energy (2023); Vaclav Smil (2017), Our World in Data, Cohen & Steers estimates.

The views and opinions are as of the date of publication and are subject to change without notice. There is no guarantee that any market forecast set forth in this presentation will be realized.

The debate over the use of fossil fuels is unlikely to fade anytime soon, given ongoing concerns about climate change and other policy issues.

Governments and markets maintain concern around the use of carbon-intensive fossil fuels, with an eye on expanding into clean, alternative energy to support global growth.

Meanwhile, there are three main drivers speeding up the development of alternatives:

- Costs. Alternative energy costs are becoming more competitive and are expected to continue declining.

- Consumer preferences. Consumers are taking environmental considerations into account, with electric vehicle growth as a prime example.

- Government support. Policy approaches across the globe offer substantial support for alternative development.

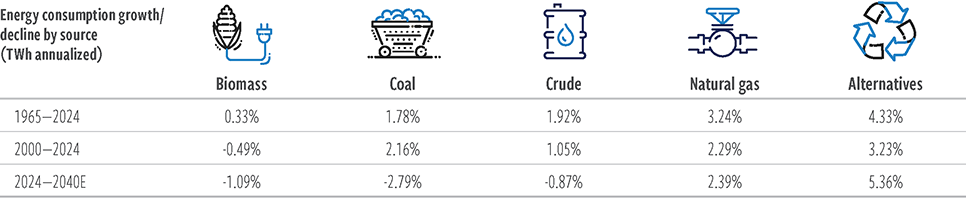

As we look to the future, we believe the global energy markets can reach a place where: (1) biomass and coal see significant declines (>50%); (2) crude oil demand grows through the 2020s, then plateaus and declines during the 2030s; and (3) all future growth comes from natural gas, nuclear and alternatives such as wind, solar and hydrogen (Exhibit 4).

EXHIBIT 4

The energy transition is occurring, albeit at a more moderate pace than many expected

Natural gas and alternatives will likely benefit the most

At December 31, 2025. Source: Our World in Data, Bloomberg, and Cohen & Steers estimates.

The views and opinions are as of the date of publication and are subject to change without notice. There is no guarantee that any market forecast set forth in this presentation will be realized.

We take a bottom-up view when we forecast crude oil demand and believe it will be difficult to substitute for it quickly. Exxon Mobil estimated in 2023 that if all car sales from that point on were electric vehicles, demand for liquid forms of energy would remain near 2010 levels into 2050. “Alternatively, a slowdown in fuel efficiency improvement of internal combustion engines could increase fuel demand by almost 3 million barrels per day by 2050.” (Source: Exxon Mobil global outlook, published September 2023.)

We believe natural gas represents a key bridge fuel as the world pursues the energy addition path. Natural gas has seen significant growth since 2000 and we see global markets continuing to invest in the critical infrastructure required to maintain this growth rate through 2040. Importantly, natural gas emits approximately 50% less CO2 than coal-fired generation. This transition from coal to natural gas is a step in the right direction for the world’s decarbonization efforts.

We estimate alternatives must boost energy output by about 40,000 TWh, more than doubling from today’s count of 35,000 TWh to 2040’s predicted need of 75,000 TWh. To put this into perspective, the entire oil industry stands at 56,000 TWh today. But with capital, technology and incentives, we believe this scenario is achievable and desirable relative to the status quo. To be clear, this will not be enough to achieve net zero goals—but it represents an outcome that is possible.

Supply growth needs to evolve

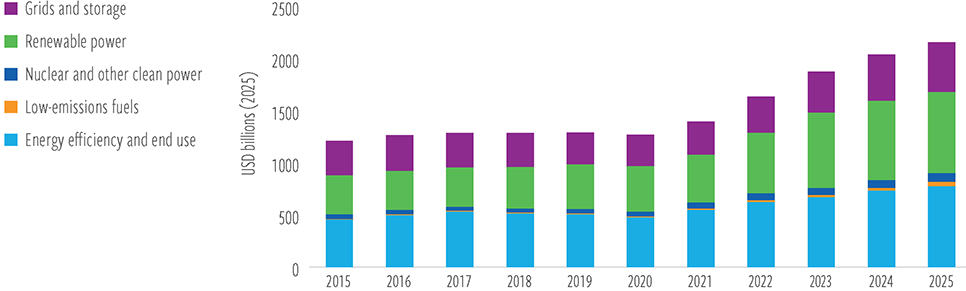

World economies are making progress on growing energy supply, but much work still needs to be done.

In fact, from 2015 through 2025, the global economy invested, on average, $1.5 trillion per year in alternative energy capex to produce approximately 1,000 TWh in annual generation capacity (Exhibit 5).

This needs to accelerate to approximately 2,600 TWh per year moving forward if we are to meet expected demand.

EXHIBIT 5

Alternative energy spending is rising

Investments in alternative power, grids and storage and energy efficiency are drivers of spending

At December 31, 2025. Source: International Energy Agency

The views and opinions are as of the date of publication and are subject to change without notice. There is no guarantee that any market forecast set forth in this presentation will be realized.

World of energy addition, not replacement

If the industry is to meet energy demand by 2040, record investments must be made. Plainly put, the marketplace needs all the reliable—and, ideally, clean—energy sources it can summon.

Technological advances must (and will) occur for alternative energy to be heavily relied upon, but it will take time. For example, energy produced by wind or solar cannot be stored for long periods of time due to limitations in battery storage technology, and production at any given moment is dependent on weather patterns. Conversely, one of the benefits of traditional resources, such as crude oil, is that they can be stored, transported and utilized on demand.

Further, a change in narrative is taking place as renewed attention is levied on domestic energy security, given the rise in geopolitical uncertainty and post Russia’s invasion of Ukraine. The need for dependable energy has never been more critical.

Investing in the overall energy picture

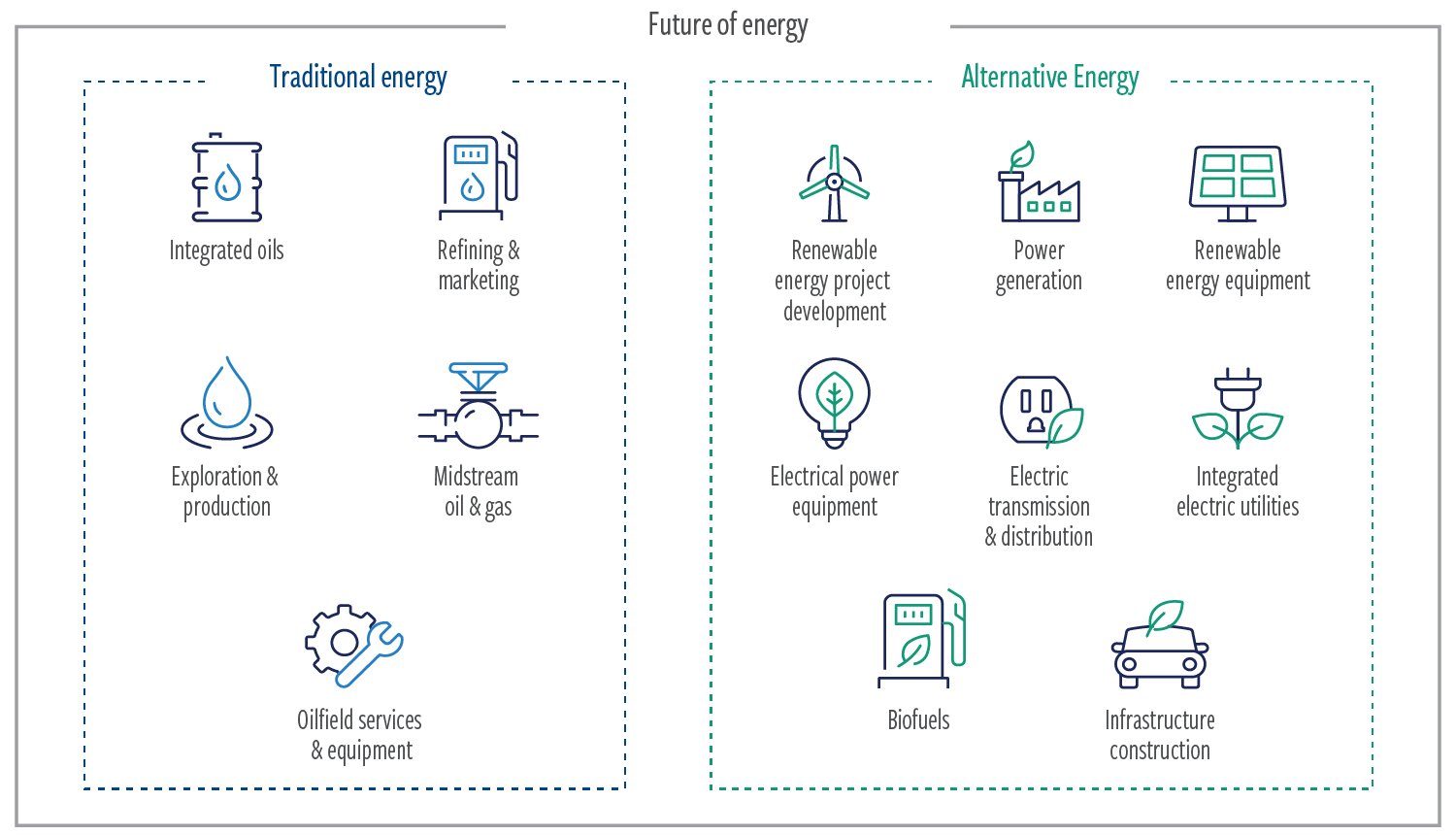

Looking ahead, we see attractive opportunities across the energy value chain in both traditional and alternative energy. However, most passive investment strategies, and many active ones, take a zero-sum view and limit their investment universes to either traditional energy companies or alternative opportunities. We believe this is suboptimal and the definition of “energy” needs to be expanded. As seen in Exhibit 6, the Bloomberg Industry Classification Standard segments the energy universe in a way that is more representative of where global energy markets are going.

EXHIBIT 6

How Bloomberg classifications segment the future of energy

Companies participating in the future of energy come from a broad array of sectors

Further, the line between clean and so-called “dirty” companies has blurred in recent years. Large, fossil-based companies are investing billions of dollars in research and development of cleaner energy forms. This includes lower-carbon hydrogen, carbon capture and storage and renewable facility investments by the world’s leading integrated energy companies.

We believe limited access to capital for conventional energy and a rising cost of capital will continue to constrain investment in traditional resources. This could lead to continued focus on capital efficiency and return on capital for businesses in the crude oil and natural gas value chain, which may lead to strong investment performance as the cycle continues.

Traditional energy companies’ woeful stock performance during 2014-2020, which was driven by poor capital allocation and value destruction, alienated investors. And the volatility of many alternative investments has fostered a “proceed with caution” mindset. However, disruption is afoot. Amid attractive valuations, improving fundamentals, better capital allocation and disruptive change, we believe active managers can provide superior returns to investors. And the opportunity is especially timely, given that many investors are under-allocated to energy today.

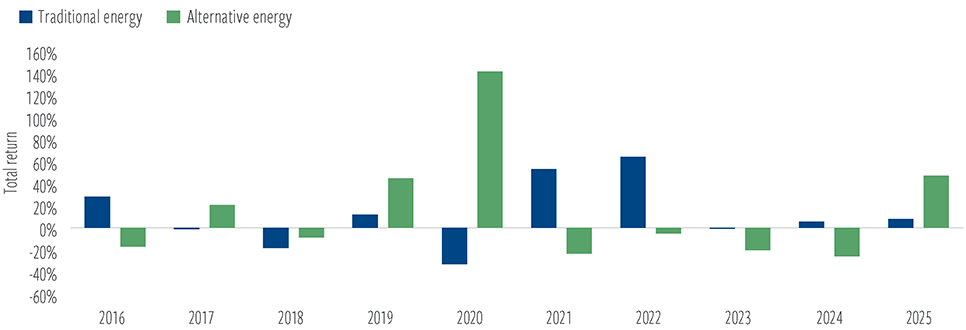

As seen in Exhibit 7, traditional and alternative energy have unique and differentiated performance profiles. Over the past 10 years, these two sectors have performed inversely (traditional up / alternative down and vice versa) more often than not. We believe combining the two helps to smooth volatility and will create superior risk-adjusted returns going forward. Dynamic structural change is accelerating in this new energy landscape. The menu of choices for investments continues to broaden, which enhances the return opportunity and potential for alpha, particularly for active managers adept at managing through disruption.

EXHIBIT 7

Traditional and alternative energy have experienced divergence in performance profiles

Calendar year returns

At December 31, 2025. Source: Morningstar.

The views and opinions are as of the date of publication and are subject to change without notice. There is no guarantee that any market forecast set forth in this presentation will be realized.

Traditional and alternative energy have historically had a

low correlation.

The complementary performance of traditional energy and alternative investments, when combined, creates attractive risk/return profiles for investors. We analyzed an illustrative blend of index performance,

representative of how we believe the global energy composition will look in 2033 (70% traditional / 30% alternative). This starting point delivered better returns at lower volatility, and with lower drawdowns, than an investment in traditional energy alone.

An illustrative blend of indices offers attractive risk/return profile

In our view, investors should be taking a much closer look at the energy sector, but they must do so with a wider aperture that recognizes the new energy world. This approach will help optimize portfolios and generate superior investment outcomes.

ABOUT THE AUTHORS

Tyler Rosenlicht, Senior Vice President, is a portfolio manager for Global Listed Infrastructure and serves as Head of Natural Resource Equities.

Index Definitions and important disclosures

Data quoted represents past performance, which is no guarantee of future results. This material is for informational purposes and reflects prevailing conditions and our judgment as of this date, which are subject to change. There is no guarantee that any market forecast set forth in this presentation will be realized. This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment.

This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this presentation to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing. Important risk considerations. There are several specific risks associated with investments in the energy sector, including: commodity price risk, depletion risk, supply and demand risk, regulatory risk, political risk, acquisition risk, weather risks, exploration risk, catastrophic-event risk, interest-rate transaction risk, affiliated-party risk and limited partner risk. S&P Energy Sector Index seeks to provide a representation of the energy sector of the S&P 500 Index. The Index includes companies from the following industries: oil, gas and consumable fuels; and energy equipment and services. S&P Global Clean Transition Energy Index measures the performance of 30 largest companies in global clean energy related businesses from both developed and emerging markets.

Energy Important Risk Considerations:

Investing involves risk, including entire loss of capital invested. There can be no assurance that the investment strategy will meet its investment objectives. Diversification is not guaranteed to ensure a profit or protect against loss. An investment in the energy sector involves risks that differ from a similar investment in equity securities, such as common stock, of a corporation. Investors will subject to more risks related to the energy sector than if an investment strategy were more broadly diversified over numerous sectors of the economy. A downturn in the energy sector of the economy could have a larger impact on the investment strategy than on an investment company that does not concentrate in the sector. At times, the performance of securities of companies in the sector has lagged the performance of other sectors or the broader market as a whole. Energy sector investments can be volatile due to fluctuations in commodity prices, availability of resources, slowdowns in construction, reduced demand for energy products, regulatory changes, extreme weather or natural disasters, rising interest rates and geopolitical events. Special risks of investing in foreign securities include (i) currency fluctuations,

(ii) lower liquidity, (iii) political and economic uncertainties, and (iv) differences in accounting standards. Certain foreign securities may represent small- and medium-sized companies, which may be more susceptible to price volatility and less liquid than larger companies.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, U.S. endowments, foundations and mutual funds. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.

For recipients in the Middle East: This document is for informational purposes only. It does not constitute or form part of any marketing initiative, any offer to issue or sell, or any solicitation of any offer to subscribe or purchase, any products, strategies or other services, nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this document wishes to receive further information with regard to any products, strategies or other services, it shall specifically request the same in writing from us.

All investing involves risk. Loss of principal is possible.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus or summary prospectus and other information about Cohen & Steers active ETFs, please call (866) 737-6370; for Cohen & Steers open-end funds, please call (800) 330-7348. Read the prospectus or summary prospectus carefully before investing.

Foreside Fund Services, LLC, is the distributor of Cohen & Steers active ETFs. Cohen & Steers Securities, LLC is the distributor of Cohen & Steers mutual funds. Foreside Fund Services, LLC is not affiliated with Cohen & Steers.