Private real estate is showing signs of a robust recovery, with improving returns, loosening lending standards, and rising transaction volumes—all pointing to a more favorable environment for capital deployment in the quarters ahead.

KEY TAKEAWAYS

- Private real estate, as measured by the NCREIF-ODCE index, has now posted four consecutive quarters of positive returns, the strongest recovery signal we’ve seen since the 2022 downturn.

- Lending standards for CRE acquisitions have loosened over recent quarters, reflecting growing confidence in real estate valuations and cash flow stability. Commercial real estate lending standards are loosening, with banks more willing to finance acquisitions. This, combined with slower supply growth, creates a supportive backdrop for existing properties.

- Transaction volume has now increased for five consecutive quarters on a year-over-year basis, marking a sustained period of activity growth.

Private real estate momentum continues to build. Lending standards are evolving favorably. And transaction volume is showing clear signs of recovery.

This month we are focusing on the private real estate cycle and the outlook for the coming quarters.

Welcome to the Real Estate Reel from Cohen & Steers.

First, we are looking at sustained momentum in private real estate returns. Private real estate, as measured by the NCREIF-ODCE index, has now posted four consecutive quarters of positive returns. This sustained performance represents the strongest recovery signal we’ve seen since the downturn began in late 2022.

EXHIBIT 1

We believe the NFI-ODCE Index bottomed in 2Q 2024

Quarterly returns of the NCREIF NFI-ODCE Index (Net) since 3Q22 (post-Covid peaky)(1)

At June 30, 2025. Source: NCREIF, Cohen & Steers. Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. There is no guarantee that any market forecast set forth in this presentation will be realized.

(1) Private real estate represented by the NCREIF NFI-ODCE Index (Net). (2) Q2 returns are preliminary.

The consistency of these positive returns suggests we’re not just seeing a temporary bounce, but rather a fundamental shift in the private real estate cycle. This aligns with our long-held view that once returns turn positive, they remain positive.

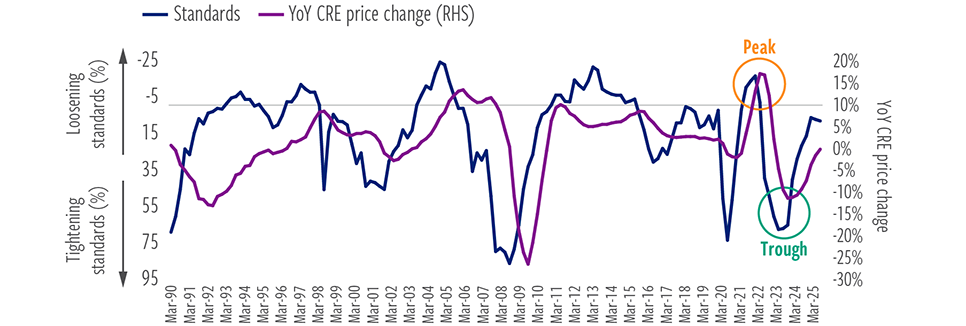

The second thing we are watching this month is commercial real estate lending standards.

The lending environment for commercial real estate is showing encouraging signs of normalization.

Lending standards for CRE acquisitions have loosened over recent quarters. Banks and other lenders are becoming more willing to finance property purchases, reflecting growing confidence in real estate valuations and cash flow stability.

EXHIBIT 2

Senior Loan Officer Opinion Survey showed 9% of net respondents reporting tighter standards

At June 30, 2025. Source: NCREIF, Senior Loan Officer Opinion Survey, Cohen & Steers. Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. There is no guarantee that any market forecast set forth in this presentation will be realized.

At the same time, supply growth is decelerating across most major property types. Lenders remain cautious about financing speculative construction, requiring higher equity commitments and stronger pre-leasing requirements.

Improving lending standards and muted supply growth creates a particularly favorable dynamic going forward.

The result is an environment where existing properties benefit from both improved capital availability and constrained competition from new construction.

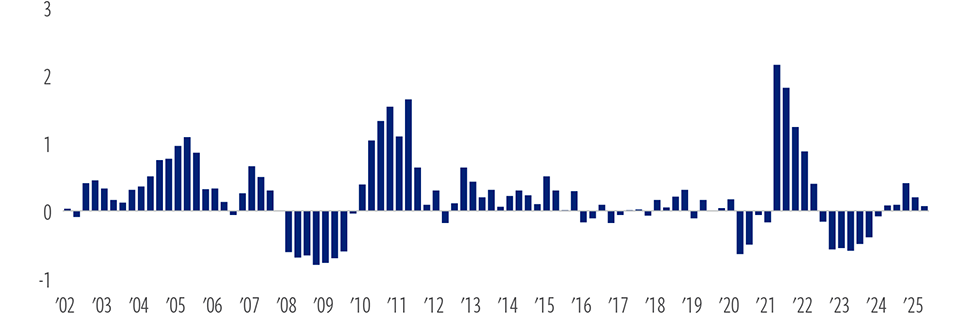

Finally, the third factor we’re monitoring is transactions volumes, evidence that capital is returning to the private real estate market.

EXHIBIT 3

US commercial real estate transaction volume

Year-Over-Year & Change

At July 31, 2025. Source: Real Capital Analytics, Cohen & Steers. Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. There is no guarantee that any market forecast set forth in this presentation will be realized.

Transaction volume has now increased for five consecutive quarters on a year over year basis, marking the most sustained period of activity growth since the market downturn began.

Institutional investors who had been sitting on the sidelines are increasingly finding opportunities. The combination of more reasonable valuations, clearer interest rate direction, and improving property fundamentals in certain sectors has created conditions that are bringing capital back to the market.

For investors who have been waiting for clear signals that the private real estate market has stabilized, these indicators provide compelling evidence that we’re entering a more favorable environment for deploying capital.

Subscribe to the Real Estate Reel via the link on screen and tune in next month to see what we’re watching.

Watch June 2025 The Real Estate Reel: Three Takeaways from REITweek

Watch all The Real Estate Reel videos.

Data quoted represents past performance, which is no guarantee of future results. The information presented does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this video will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

This video is for informational purposes and reflects prevailing conditions and our judgment as of August 2025, which are subject to change. This material should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this video to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Risks of Investing in Real Estate Securities. Risks of investing in real estate securities are similar to those associated with direct investments in real estate, including falling property values due to increasing vacancies or declining rents resulting from economic, legal, political or technological developments, lack of liquidity, limited diversification and sensitivity to certain economic factors such as interest rate changes and market recessions. Foreign securities involve special risks, including currency fluctuations, lower liquidity, political and economic uncertainties, and differences in accounting standards. Some international securities may represent small- and medium-sized companies, which may be more susceptible to price volatility and less liquidity than larger companies. No representation or warranty is made as to the efficacy of any particular strategy or fund or the actual returns that may be achieved.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, U.S. endowments, foundations and mutual funds. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.

For Investors in the Middle East: This document is for information purposes only. It does not constitute or form part of any marketing initiative, any offer to issue or sell, or any solicitation of any offer to subscribe or purchase, any products, strategies or other services nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this document wishes to receive further information with regard to any products, strategies other services, it shall specifically request the same in writing from us.