Global listed infrastructure offers a compelling investment opportunity through essential, long-lived assets that deliver stable, inflation-linked cash flows and portfolio diversification—especially in today’s uncertain market environment.

Infrastructure assets form the backbone systems that support essential services, enabling communities to function and economies to grow.

The $6.2 trillion global listed universe consists primarily of companies that own and operate these assets, grouped into four main categories.

These businesses have common characteristics that unite them as an asset class and make for attractive investments.

Long-lived assets: Infrastructure assets typically have useful lives of several decades, providing a long-term source of income.

High barriers to entry: Strict zoning restrictions, large capital requirements and, in some cases, exclusivity agreements make it difficult or prohibitive for competitors to enter the market.

Inelastic demand: Infrastructure provides essential services that often remain in demand even in periods of economic downturns.

Predictable, inflation-linked cash flows: Infrastructure assets are often regulated or operate under long-term contracts or concession agreements, typically resulting in greater cash flow stability relative to many other businesses.

Secular themes driving opportunities

The infrastructure landscape is experiencing a transformation unlike anything seen in decades. Three powerful trends are reshaping how we power our world, connect our data, and move our goods.

These trends are interconnected and reinforcing, creating unprecedented investment opportunities in a wide range of global listed infrastructure subsectors.

At September 30, 2025. Source: Cohen & Steers.

There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. The views and opinions in this presentation are as of the date of publication and subject to change without notice. There is no guarantee that any market forecast set forth in this presentation will be realized.

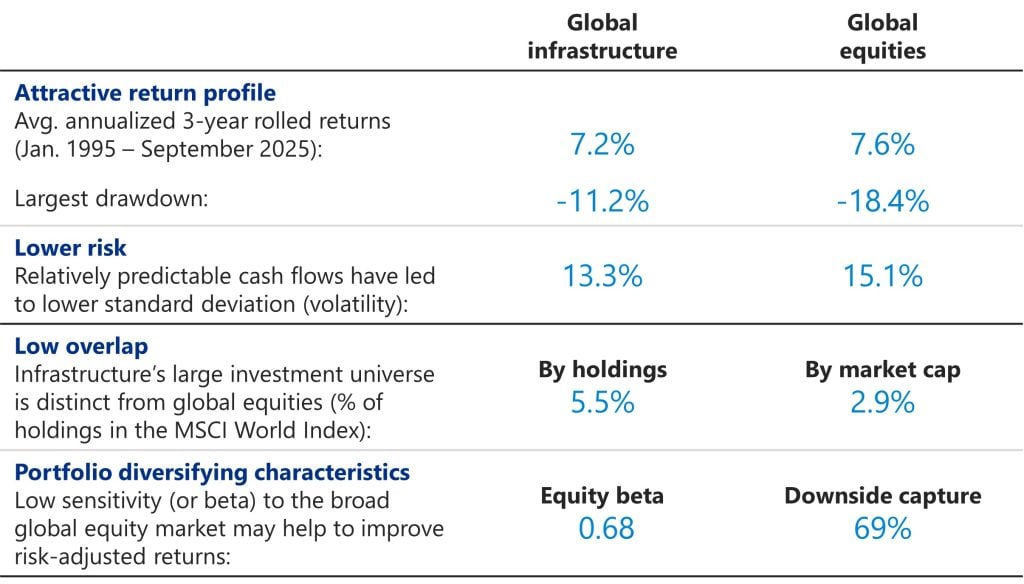

Why invest in listed infrastructure?

Infrastructure has generated consistent, competitive performance relative to global equities over full market cycles, while providing diversifying access to subsectors and investment themes that are typically under-represented in broad equity market allocations.

Notably, infrastructure historically has been a defensive asset class due to the relative cash flow stability of the underlying assets, thereby generally outperforming the broader equity market during business cycle and equity market downturns.

Competitive returns with lower volatility

At September 30, 2025. Source: Cohen & Steers.

Past performance is no guarantee of future results. The information above does not reflect information about any fund or account managed or serviced by Cohen & Steers, and there is no guarantee investors will experience the type of performance reflected above. Diversification cannot ensure a profit or protect against loss in a declining market. Rolled returns measure average annualized investment performance over multiple overlapping time periods, rather than just a single fixed period. This method helps smooth out short-term volatility and gives a more comprehensive view of how an investment performs over time. Largest drawdown refers to the rolled 3-year period with the lowest averaged annualized return over the stated time period. Standard deviation measures the dispersion of returns from the mean; greater the spread, the higher the deviation. Equity beta measures how sensitive a given investment is to movements in the broad equity market. An equity beta of 1.2 means the investment tends to rise or fall 20% more than the market, while a beta of 0.7 reflects greater stability and less sensitivity to market swings. Downside capture ratio shows whether a given investment has outperformed—lost less than—a broad market benchmark during periods of market weakness, and if so, by how much. See end notes for index associations, definitions and additional disclosures.

Given infrastructure’s relatively light representation in the broad equity market, a standalone allocation may benefit overall portfolios.

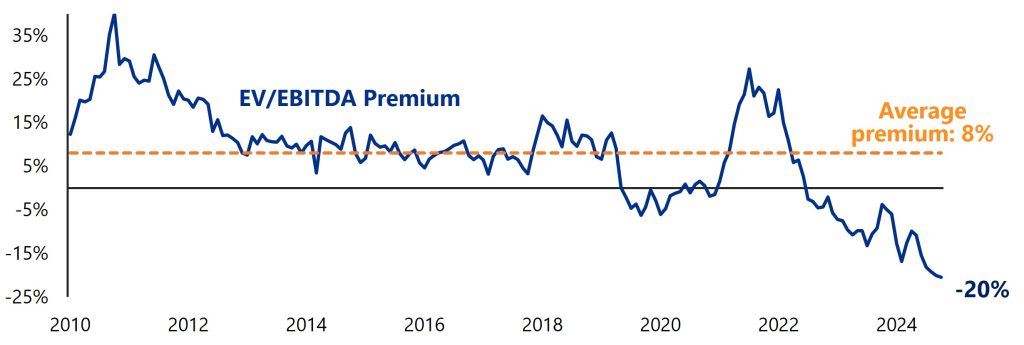

Attractive entry point for investors

Global listed infrastructure historically has traded at about a 9% cash flow multiple premium to broad stocks, due to the relative stability of its cash flows. However, infrastructure is currently priced at an 18% cash flow discount, following several years of underperformance relative to global equities.

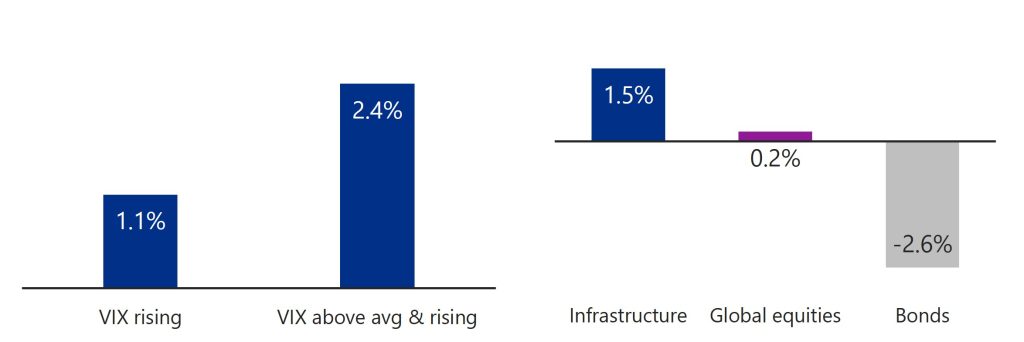

Infrastructure typically outperforms global equities during times of heightened market uncertainty. And it tends to respond positively to unexpected inflation, potentially helping to mitigate the damaging effects of unexpected inflation on stocks and bonds.

Infrastructure is currently trading at a steep discount to global equities

December 2010 – September 2025

At September 30, 2025. Source: MSCI, FTSE, FactSet, Cohen & Steers

Past performance is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee investors will experience the type of performance reflected above. EV/EBITDA compares a company’s enterprise value (EV) to its earnings before interest, taxes, depreciation & amortization (EBITDA). Average represents the historical average based on monthly data starting December 31, 2010. VIX is the CBOE Volatility Index, measuring expected market volatility. Inflation beta measures an asset’s historical sensitivity of real returns to unexpected inflation, defined as the difference between realized annual inflation and survey-based inflation expectations from 12 months prior. An inflation beta of 2 indicates real (inflation-adjusted) returns 2% above average for each 1% surprise in inflation. Inflation beta is estimated via a regression of 1-year real returns on the difference between realized inflation and lagged expectations, as well as the lagged expectation level. Inflation is measured using the Consumer Price Index (CPI) for all urban consumers (U.S. Bureau of Labor Statistics). Expected inflation is the median forecast from the University of Michigan Survey of 1-Year Ahead Inflation Expectations. See end notes for index associations, definitions and additional disclosures.

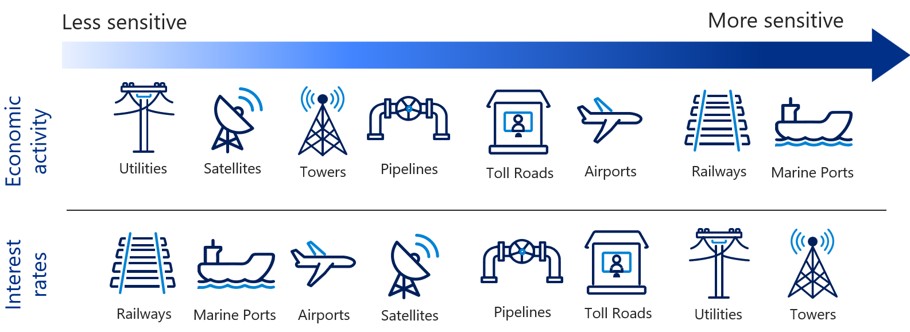

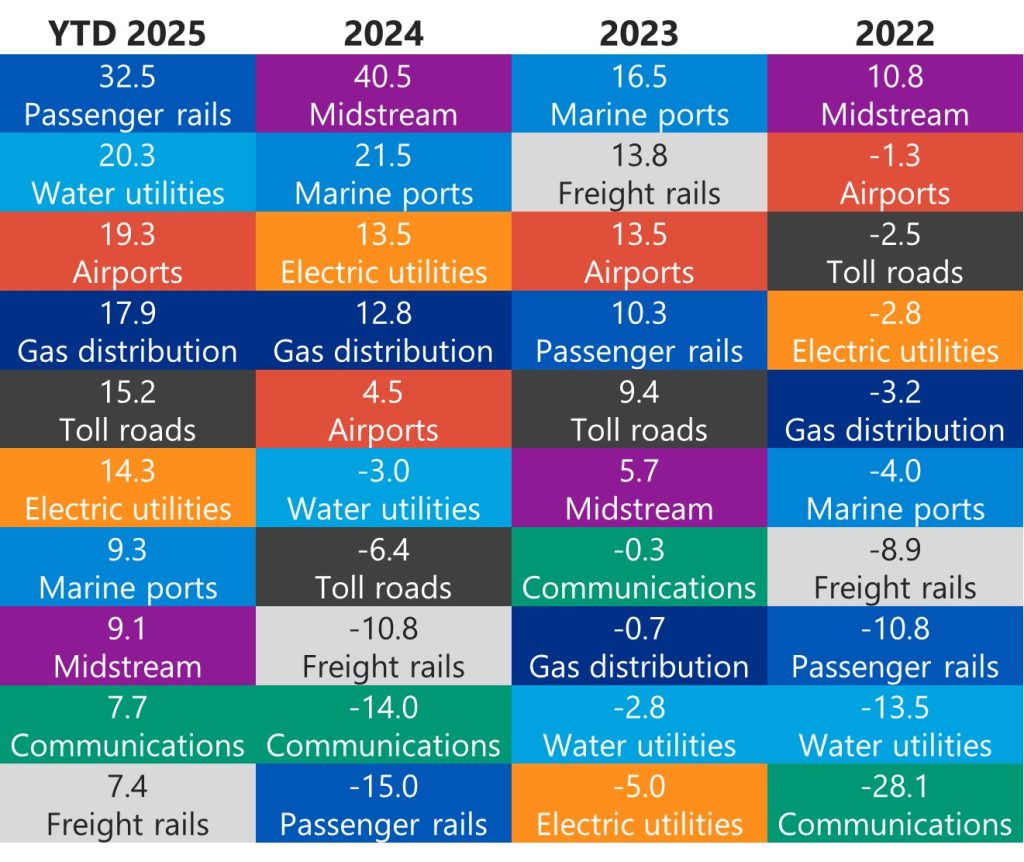

Active management: A tactical advantage

Certain sectors historically exhibit clear defensive properties across the business cycle, while others tend to be more economically sensitive. The variety of sectors also provides flexibility in most interest rate environments.

The dispersion of sector returns from year to year and across varying economic and interest rate environments are opportunities for active managers to enhance returns unavailable to passive investment strategies.

Subsectors offer diverse macroeconomic sensitivities

Wide performance dispersion favors active management

Calendar year returns (%)

At September 30, 2025. Source: Cohen & Steers.

Past performance is no guarantee of future results. The information above is for illustrative purposes only and does not reflect information about any fund or other account managed or serviced by Cohen & Steers.

Index definitions and important disclosures

An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes. Index comparisons have limitations as volatility and other characteristics may differ from a particular investment.

There is no guarantee that any historical trend illustrated in this presentation will be repeated in the future, and there is no way to predict precisely when such a trend might begin. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any market forecast set forth in this presentation will be realized. The views and opinions in this presentation are as of the date of publication and subject to change without notice.

Global listed infrastructure: UBS Global 50/50 Infrastructure & Utilities Index for periods through March 31, 2015; FTSE Global Core Infrastructure 50/50 Net Tax Index thereafter. The UBS Global 50/50 Infrastructure & Utilities Index tracks a 50% exposure to the global developed market utilities sector and a 50% exposure to global developed market infrastructure sector. The index is free-float market-capitalization weighted and reconstituted annually with quarterly rebalances and is net of dividend withholding taxes. The FTSE Global Core Infrastructure 50/50 Net Tax Index is a market-capitalization-weighted index of worldwide infrastructure and infrastructure-related securities and is net of dividend withholding taxes. Constituent weights are adjusted semi-annually according to three broad industry sectors: 50% utilities, 30% transportation, and a 20% mix of other sectors, including pipelines, satellites, and telecommunication towers. Global equities: MSCI World Index, a free-float-adjusted index that measures the performance of large- and mid-capitalization companies representing developed market countries and is net of dividend withholding taxes. U.S. bonds: The Bloomberg U.S. Aggregate Bond Index includes investment-grade government, corporate and mortgage-backed bonds. VIX: CBOE Volatility Index, measures the expected volatility of the S&P 500 over the next 30 days and is used by investors to evaluate market sentiment and perceived risk.

Risks of investing in listed infrastructure. Infrastructure issuers may be subject to regulation by various governmental authorities and may also be affected by governmental regulation of rates charged to customers, operational or other mishaps, tariffs and changes in tax laws, regulatory policies and accounting standards. Foreign securities involve special risks, including currency fluctuations, lower liquidity, political and economic uncertainties and differences in accounting standards. Some international securities may represent small and medium-sized companies, which may be more susceptible to price volatility and less liquidity than larger companies.

Cohen & Steers U.S. registered open-end funds are distributed by Cohen & Steers Securities, LLC and are only available to U.S. residents.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Limited is a private company limited by shares in the Republic of Singapore.