The complexity of the infrastructure universe affords skilled active

managers opportunities to identify and capitalize on market inefficiencies.

KEY TAKEAWAYS

- Active strategies typically outperform diversified passive peers, delivering stronger returns with lower volatility across infrastructure cycles.

- By combining rigorous fundamental analysis, dynamic risk management and forward-looking positioning, active managers have the potential to deliver superior outcomes.

- A generational opportunity in capital formation is occurring, offering active managers a chance to unlock long-term growth for investors.

Global listed infrastructure is a dynamic asset class, comprising shares of companies that own and operate essential services within sectors such as utilities, communications, transportation and energy. Infrastructure’s performance drivers are influenced by many factors: government policy, concession agreements, capital-intensive investments, macroeconomic conditions and technological change. Moreover, it is not a uniform market— constituents span more than a dozen subsectors across geographies, with distinct regulatory and economic environments—and the space continues to evolve.

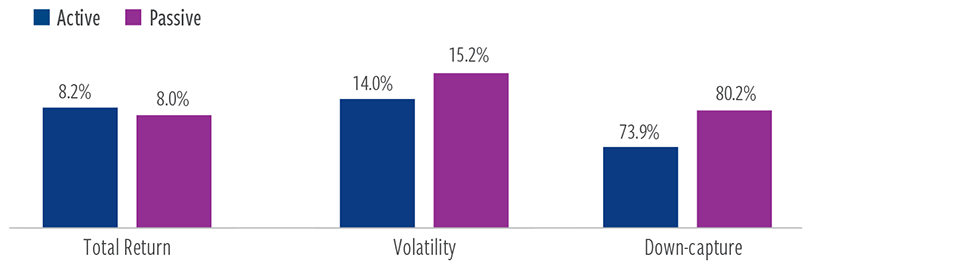

Given the intricacies of the asset class, it is not surprising that active managers focused on core infrastructure have historically delivered results superior to their passive peers (Exhibit 1). Net of fees, active strategies have produced better total returns, with meaningfully less volatility, while providing better risk mitigation during market downturns. We believe this reflects skilled active managers’ ability to discern risk from opportunity—an edge that passive strategies may be structurally unable to replicate.

EXHIBIT 1

Active managers deliver superior outcomes

10-year annualized returns, standard deviation and downside capture

At September 30, 2025. Source: Morningstar.

Data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. Data reflects the 10-year period for core infrastructure funds benchmarked against globally diversified infrastructure indexes, including those from the S&P, MSCI, Dow Jones Brookfield and STOXX global infrastructure benchmark families. Inclusion of all funds in the category may yield different results, as some funds focus on specific subsectors or geographies with different return and risk profiles. Standard deviation is a measure of the dispersion (volatility) of a set of data from its mean. Downside capture shows whether a given strategy has outperformed—lost less than—the broad-based MSCI World NR USD Index during periods of market weakness (and if so, by how much).

Passive infrastructure strategies have historically focused on non-core businesses or narrow, concentrated themes

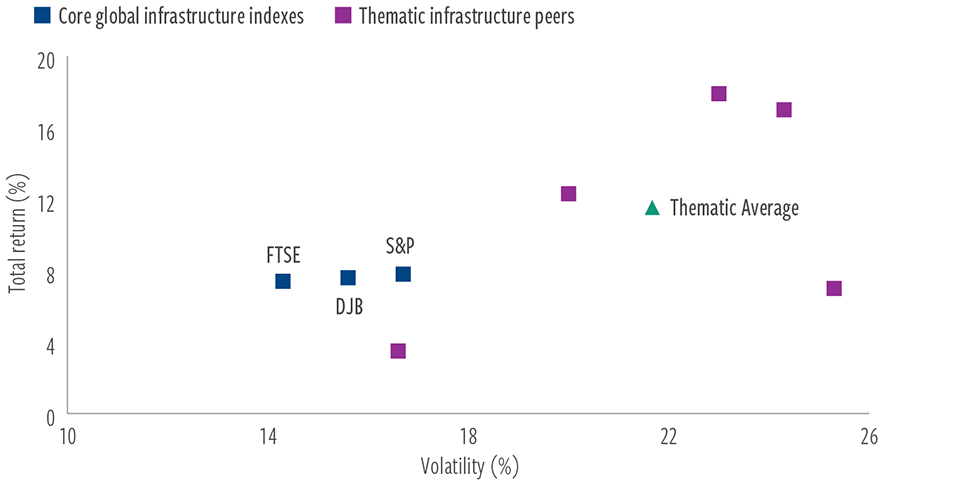

Exhibit 1 excludes a handful of passive funds in the Morningstar infrastructure category that are focused on non-core and/or thematic infrastructure, such as engineering and construction, materials, equipment manufacturing and electrification. While some of these funds have posted strong relative returns in recent years, the tradeoff is that their gains came alongside a meaningful increase in volatility—both in absolute terms and relative to the broad infrastructure market (Exhibit 2). Further, these strategies tend to be much higher beta (have greater sensitivity to movements in the broad equity market) than core infrastructure, while providing materially less downside protection.

These passive strategies may capitalize on current investment trends but lack the ability to rotate as markets and opportunities shift. As a result, the funds may not hold up well in a declining market, as they exhibit greater drawdowns and higher volatility.

Diversified core strategies have more consistently delivered the critical performance characteristics of infrastructure. Although they have generated more modest returns than some non-core passive funds over the past decade, a core, diversified approach can provide important benefits to an equity portfolio, including return consistency, broad market diversification and downside protection.

EXHIBIT 2

Thematic, non-core strategies deliver higher risk and more uncertain outcomes than core infrastructure

Annualized total returns vs. volatility (May 2018 – September 2025)

At September 30, 2025. Source: Morningstar, Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. Data reflects average annualized returns from the common inception (May 2018) for strategies with a minimum 5-year track record. Standard deviation is a measure of the dispersion (volatility) of a set of data from its mean. Core benchmarks reflect the FTSE Global Core Infrastructure 50/50 NR USD, S&P Global Infrastructure NR USD, and Dow Jones Brookfield Global Infrastructure NR USD indexes. Thematic passive infrastructure peers reflect those benchmarked to non-core infrastructure, such as infrastructure builders and development or electrification companies. The thematic, non-core average is AUM weighted. See endnotes for additional disclosures.

How active management can add value

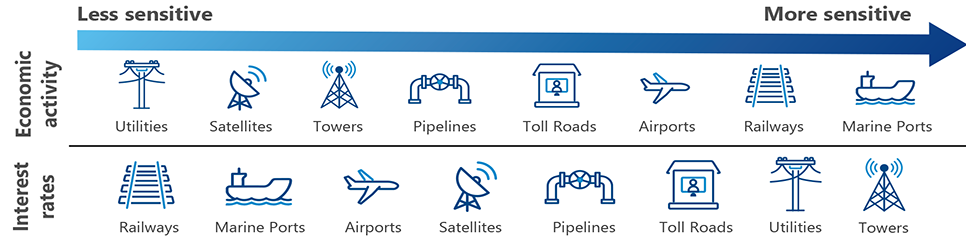

Infrastructure subsectors exhibit differing macroeconomic sensitivities, resulting in wide dispersion of returns depending on where we are in economic, interest rate and inflation cycles (Exhibit 3). Active managers attuned to these macro sensitivities (which can vary across geographies) can adjust holdings as conditions shift, potentially enhancing portfolio returns.

EXHIBIT 3

Infrastructure sectors offer diverse macroeconomic sensitivities

At September 30, 2025. Source: Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. The information above is for illustrative purposes only and does not reflect information about any fund or other account managed or serviced by Cohen & Steers.

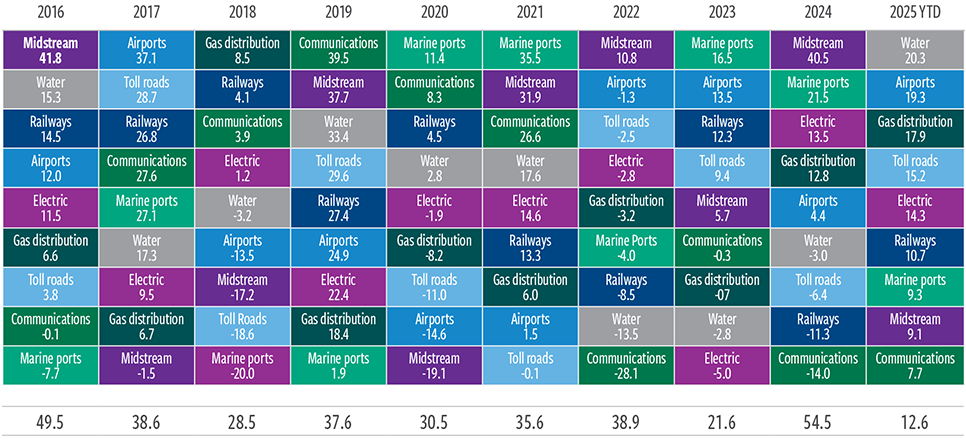

Over the last decade, at least a 20% return dispersion between top- and bottom- performing subsectors has occurred each year (Exhibit 4), creating significant alpha generation opportunities for active managers who incorporate proprietary views on allocation into their portfolio construction processes. They can also adjust subsector positioning as macro views evolve or as relative valuations shift. In contrast, passive strategies remain constrained by static index methodologies.

EXHIBIT 4

Wide performance dispersion favors active management

Global listed infrastructure sector returns and range by calendar year (%)

At September 30, 2025. Source: Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. Sector returns based on the FTSE Developed Core Infrastructure 50/50 Index. Numbers may not sum due to rounding. See endnotes for index associations, definitions and additional disclosures.

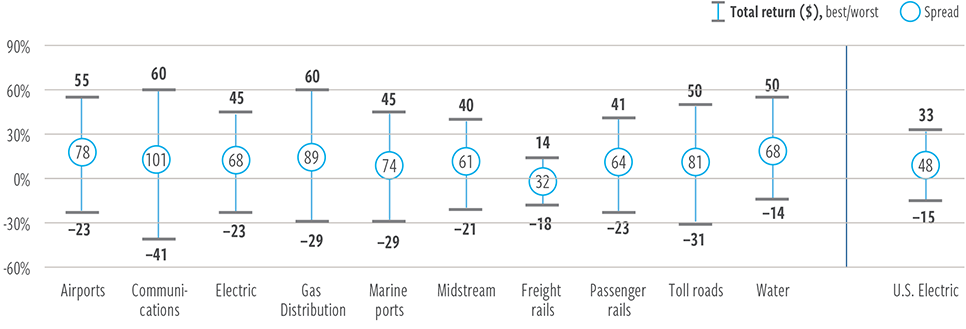

Exhibit 5 further illustrates the alpha potential within infrastructure by highlighting the wide dispersion in returns among individual stocks—even within traditionally defensive sectors, such as utilities. This variability underscores the importance of active management in identifying outperformers and avoiding laggards.

EXHIBIT 5

Return dispersion is pronounced even within relatively defensive sectors

95th and 5th percentile stock returns (%) (September 2024 – September 2025)

At September 30, 2025. Source: Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. Sector returns based on the FTSE Developed Core Infrastructure 50/50 Index. Numbers may not sum due to rounding. See endnotes for index associations, definitions and additional disclosures.

Case study: U.S. electric utilities

Year to date in 2025, we have seen significant dispersion within U.S. electric utilities, a group of companies typically viewed by generalist investors as being relatively homogeneous. Despite that perception, dispersion has reached nearly 50% between stocks in the 95th and 5th percentiles (Exhibit 5).

Multiple factors have driven this dispersion, some of which apply to equities generally and many others that are unique to the subsector. U.S. electric utility stocks with the strongest performance have been those most tied to rising power demand—a theme driving expectations for accelerated earnings growth amid increased capital spending. By contrast, utilities with significant exposure to California have lagged, as early-year wildfires raised concerns about the long-term viability of the state’s wildfire insurance fund.

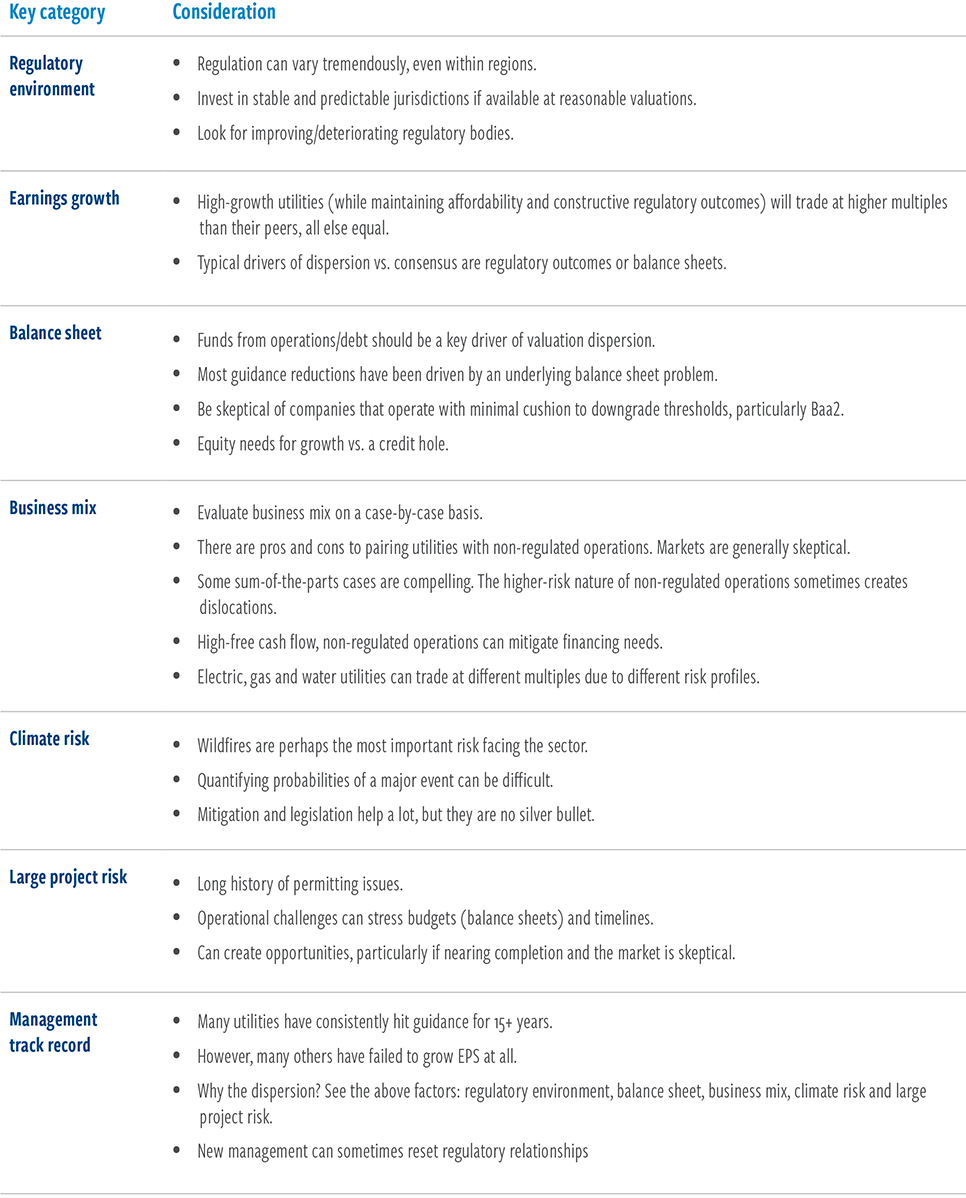

Each infrastructure sector has a distinct set of drivers that active managers evaluate, which passive strategies typically ignore. Some examples of critical drivers for electric utilities are shown on the next page.

Critical electric utilities investment factors

Putting active management into practice

The value of active management in infrastructure lies in the ability to adapt, anticipate and act decisively across market cycles. Active managers apply a range of tools to deliver differentiated outcomes that passive strategies simply cannot replicate, including:

- Proactive risk management: Infrastructure assets carry idiosyncratic risks: regulation in utilities, technological obsolescence in communications and aging transportation infrastructure, for instance. Passive funds cannot adjust when risks loom; rather, they rely on markets to resize positions. Active managers continuously assess position sizes and rebalance portfolios in anticipation of market events—actions that can help preserve capital during downturns and foster more stable long-term returns.

- Deep fundamental analysis: Active infrastructure managers conduct rigorous due diligence, not just on financial metrics but also on qualitative factors like regulation, management track record, project pipeline, asset quality and concession terms. Since policy changes and operational challenges can affect cash flows, bottom-up research is essential. Active managers can also spot mispricings, potentially adding value through proprietary insights and avoidance of troubled assets.

- Capitalizing on structural shifts and market inefficiencies: The infrastructure asset class is at a historic inflection point, shaped by rapidly growing power demand, the digital transformation of economies, and reshoring of manufacturing. Active managers can identify and overweight companies at the vanguard of these structural shifts, which may deliver meaningful outperformance. Active strategies can also exploit short-term dislocations, such as during regulatory changes or market corrections, turning volatility into opportunity.

Bottom-up research and proactive positioning can help unlock value in this evolving—and increasingly growth-oriented— asset class.

A generational opportunity in capital formation is unfolding

Developed markets need to modernize aging infrastructure—a well- known narrative—while emerging economies are racing to build systems to support powerful demographic trends such as rising standards of living and urbanization. And long-term forces are accelerating this global buildout: surging power demand driven by AI and electric vehicles; a shift to renewables, which is expected to triple their share of global generation by 2040; digital transformation, with 5G and AI fueling demand for data centers and towers; and deglobalization, as supply chains move closer to home, impacting the value of ports, airports and freight rails.

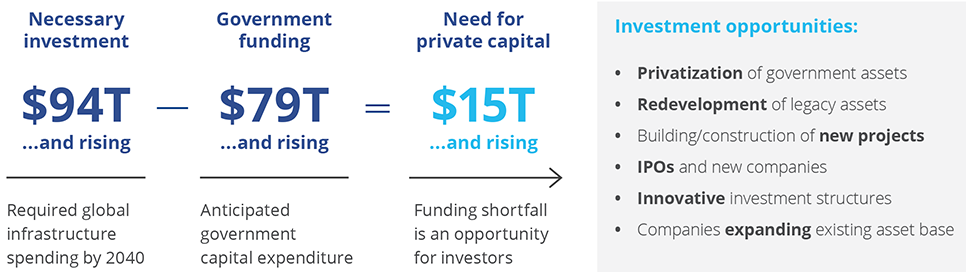

Nearly $100 trillion in infrastructure spending will be needed in the next 15 years to address the trends reshaping the global economy (Exhibit 6). But government spending will not be sufficient: A substantial funding gap is likely, one that the private sector can fill by privatizing government-owned assets, developing new and enhancing existing assets, and forming new companies. These actions, we believe, will create compelling opportunities for investors searching for stable, long-term opportunities in the public markets.

In this evolving investment landscape, active management is essential, in our opinion. The nuances of infrastructure investing—from regulatory navigation to thematic capital allocation to proactive risk management—demand the insights, flexibility and conviction that only active managers can provide. For investors seeking resilient returns, inflation protection, diversification and alignment with global megatrends, a skilled active manager can offer a compelling edge.

EXHIBIT 6

Investor capital will be essential to the infrastructure buildout

Demand for infrastructure exceeds government funding capabilities

At September 30, 2025. Source: World Economic Forum, World Bank Group, Cohen & Steers.

There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin.

ABOUT THE AUTHORS

Benjamin Morton, Executive Vice President, is Head of Global Infrastructure and a senior portfolio manager for Cohen & Steers’ infrastructure portfolios, including those focused on master limited partnerships.

Index definitions / important disclosures

An investor cannot invest directly in an index, and index performance does not reflect the deduction of any fees, expenses or taxes.

Global listed infrastructure: FTSE Developed Core Infrastructure 50/50 Index, a market-capitalization-weighted index of infrastructure and infrastructure-related securities in worldwide developed markets; constituent weights are adjusted semi-annually according to three broad industry sectors: 50% utilities, 30% transportation, and a 20% mix of other sectors, including pipelines, satellites and telecommunication towers. The Dow Jones Brookfield Global Infrastructure Index, a free-float-adjusted market-capitalization-weighted index that measures performance of companies around the world that derive more than 70% of their cash flows from infrastructure lines of business. The S&P Global Infrastructure Index, provides liquid and tradable exposure to 75 companies from around the world that represent the listed infrastructure universe. To create diversified exposure, the index includes three distinct infrastructure clusters: utilities, transportation, and energy. Global equities: MSCI World Index, a free-float-adjusted index that measures the performance of large- and mid-capitalization companies representing developed market countries and is net of dividend withholding taxes.

Past performance is no guarantee of future results. There is no guarantee that any historical trend illustrated/referenced above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. There is no guarantee that any market forecast set forth in this commentary will be realized. The views and opinions in the preceding commentary are as of the date of publication and are subject to change. Diversification does not ensure a profit or guarantee to protect against loss. There is no guarantee that actively managed investments will outperform the broader market.

This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment, and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this presentation to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment.

Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing. The views and opinions expressed are not necessarily those of any broker/dealer or its affiliates. Nothing discussed or suggested should be construed as permission to supersede or circumvent any broker/dealer policies, procedures, rules or guidelines.

Global listed infrastructure risks. Infrastructure issuers may be subject to regulation by various governmental authorities and may also be affected by governmental regulation of rates charged to customers; operational or other mishaps; tariffs; and changes in tax laws, regulatory policies and accounting standards. Foreign securities involve special risks, including currency fluctuations, lower liquidity, political and economic uncertainties, and differences in accounting standards. Some international securities may represent small and medium-sized companies, which may be more susceptible to price volatility and may have lower liquidity than larger companies.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.

For recipients in the Middle East: This document is for informational purposes only. It does not constitute or form part of any marketing initiative or any offer to issue or sell (or any solicitation of any offer to subscribe or purchase) any products, strategies or other services, nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this document wishes to receive further information with regard to any products, strategies or other services, it shall specifically request the same in writing from us.

All investing involves risk. Loss of principal is possible.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus or summary prospectus and other information about Cohen & Steers active ETFs, please call (866) 737-6370; for Cohen & Steers open-end funds, please call (800) 330-7348. Read the prospectus or summary prospectus carefully before investing.

Foreside Fund Services, LLC, is the distributor of Cohen & Steers Active ETFs. Cohen & Steers Securities, LLC, is the distributor of Cohen & Steers funds. Cohen & Steers Capital Management, Inc, is the advisor. Foreside Fund Services, LLC, is not affiliated with Cohen & Steers Securities, LLC, or Cohen & Steers Capital Management, Inc.