2025 was a solid year for preferred securities. And there are ample reasons to believe returns will stay favorable in 2026.

Of course, we entered the year with credit spreads near historically tight levels and unlikely to narrow much further. However, we expect spreads to hold in this low range amid resilient growth and because credit fundamentals are supportive.

For instance, banks—the largest issuer segment of preferreds—are enjoying strong profitability, supported by diversified earnings drivers beyond AI. Plus, bank balance sheets are in the best shape in memory, putting banks in a position to return capital to shareholders. Strong investor demand and limited net new bank preferred issuance are providing a supportive technical backdrop for the preferreds market.

Meanwhile, income levels across the preferreds universe are attractive for long-term buyers, in our view, providing some of the highest yields found among investment-grade securities, ranging from 6 to 7%. Preferreds’ high income component has helped them meaningfully outperform investment-grade bonds on a total return basis over the past 10 years.

Moreover, preferreds currently have higher total return “breakevens” than in recent periods, offering a buffer for unforeseen events. Breakevens represent the amount by which interest rates could rise and/or credit spreads could widen before the total return drops to zero.

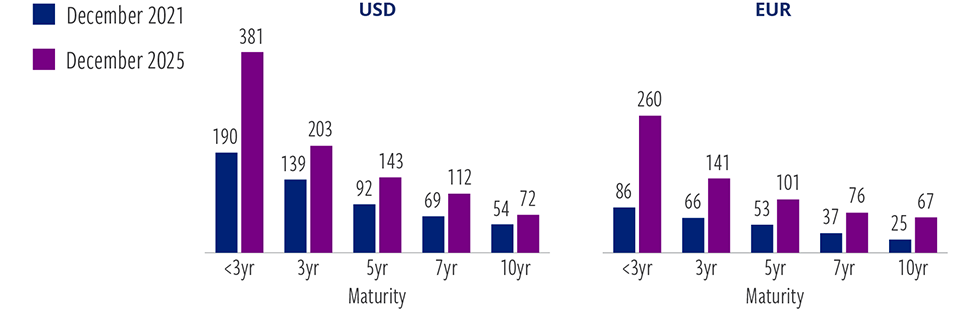

Preferreds are currently well cushioned against uncertainty

U.S. dollar and euro total return breakevens (basis points)

At December 31, 2025. Source: ICE BofA, Cohen & Steers.

Past performance is no guarantee of future results. There is no guarantee that any historical trend illustrated above will be repeated in the future or any way to know in advance when such a trend might begin. Breakevens are based on yield-to-worst and effective duration.

Following the central bank rate-hiking cycle of 2022–23, total return breakevens have risen and are most pronounced on the front end of the maturity spectrum—now two to three times higher compared with late 2021. Despite rate cuts in 2024–25, today’s higher income levels provide more protection and value for fixed income investors. This cushion adds stability to preferreds, guarding against rising rates or widening credit spreads, as there is ample room for breakevens to decline before returns are meaningfully affected.

Data quoted represents past performance, which is no guarantee of future results. The information presented does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this video will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

This video is for informational purposes and reflects prevailing conditions and our judgment as of February 17, 2026, which are subject to change. This material should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this video to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Risks of Investing in Preferred Securities. An investment in a preferred strategy is subject to investment risk, including the possible loss of the entire principal amount that you invest. The value of these securities, like other investments, may move up or down, sometimes rapidly and unpredictably. Our preferred strategies may invest in below-investment-grade securities and unrated securities judged to be below investment grade by the advisor. Below-investment-grade securities or equivalent unrated securities generally involve greater volatility of price and risk of loss of income and principal, and may be more susceptible to real or perceived adverse economic and competitive industry conditions than higher-grade securities.

Contingent capital securities (CoCos). CoCos are debt or preferred securities with loss absorption characteristics built into the terms of the security, for example a mandatory conversion into common stock of the issuer under certain circumstances, such as the issuer’s capital ratio falling below a certain level. Since the common stock of the issuer may not pay a dividend, investors in these instruments could experience a reduced income rate, potentially to zero, and conversion would deepen the subordination of the investor, hence worsening the investor’s standing in a bankruptcy. Some CoCos provide for a reduction in the value or principal amount of the security under such circumstances. In addition, most CoCos are considered to be high yield securities and are therefore subject to the risks of investing in below-investment-grade securities.

Duration risk. Duration is a mathematical calculation of the average life of a fixed-income or preferred security that serves as a measure of the security's price risk to changes in interest rates (or yields). Securities with longer durations tend to be more sensitive to interest rate (or yield) changes than securities with shorter durations. Duration differs from maturity in that it considers potential changes to interest rates, and a security's coupon payments, yield, price and par value and call features, in addition to the amount of time until the security matures. Various techniques may be used to shorten or lengthen a portfolio's duration. The duration of a security will be expected to change over time with changes in market factors and time to maturity.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, endowments, foundations and mutual funds. Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.

For recipients in the Middle East: This document is for informational purposes only. It does not constitute or form part of any marketing initiative or any offer to issue or sell (or any solicitation of any offer to subscribe or purchase) any products, strategies or other services, nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this document wishes to receive further information with regard to any products, strategies or other services, it shall specifically request the same in writing from us.