Energy Knowledge Center

Energy powers the global economy, but today’s system is more complex than ever. A diverse mix of traditional and alternative sources works together to support reliability, affordability and long-term sustainability.

As energy demand surges, no single energy source can meet global demand alone. A holistic understanding of energy—and how it flows from production to end use—reveals a broader investment opportunity.

Understanding the energy universe

Sources of Energy

Energy sources generally fall into two categories: traditional energy, which has historically met most global demand, and alternative energy, which is expanding as technology and infrastructure evolve. Rather than replacing one another, these sources are increasingly expected to coexist, supporting reliability, affordability, and long‑term sustainability.

Traditional energy continues to provide scale, flexibility, and reliability, despite being finite and subject to environmental concerns, geopolitical risk, and global supply dynamics.

Alternative energy supports decarbonization and sustainability but faces practical challenges. Wind and solar are intermittent and rely on storage and grid upgrades, while nuclear requires significant capital, long development timelines, and regulatory oversight. Continued investment and innovation are key to broader adoption.

No single energy source can meet global demand on its own. Each involves trade‑offs, making a diversified energy mix essential.

Traditional Energy Sources

Oil

Oil is a major fuel for transportation, manufacturing, and industrial use. It is extracted and refined into fuels and materials used globally. While prices are influenced by geopolitics and supply dynamics, oil remains essential due to its reliability and established infrastructure.

Natural Gas

Natural gas is widely used for power generation, heating, and industrial activity. Transported by pipelines or as liquefied natural gas (LNG), it is valued for its flexibility and ability to respond quickly to changes in demand.

Coal

Coal has long supported electricity generation because of its availability and energy density. Although its use has declined in many developed markets, it continues to provide reliable power in regions with limited alternatives.

Biomass

Biomass energy comes from organic materials such as wood and agricultural waste. It can be used for power, heating, and fuels, and sits between traditional and alternative energy due to renewable inputs paired with combustion‑based use.

Alternative Energy Sources

Solar

Solar power converts sunlight into electricity and has grown rapidly as costs have fallen. Generation depends on sunlight and weather, requiring grid support or complementary energy sources for reliability.

Wind

Wind energy uses turbines to generate electricity from natural wind patterns. It is cost‑competitive in many regions, though output varies with weather and requires grid integration.

Nuclear

Nuclear energy provides continuous, emissions‑free electricity and supports grid stability. While development involves high upfront costs and long timelines, it remains an important source of reliable baseload power.

Hydropower

Hydropower generates electricity from flowing water and is one of the most established renewable sources. It offers reliable and flexible power but depends on geography and water availability.

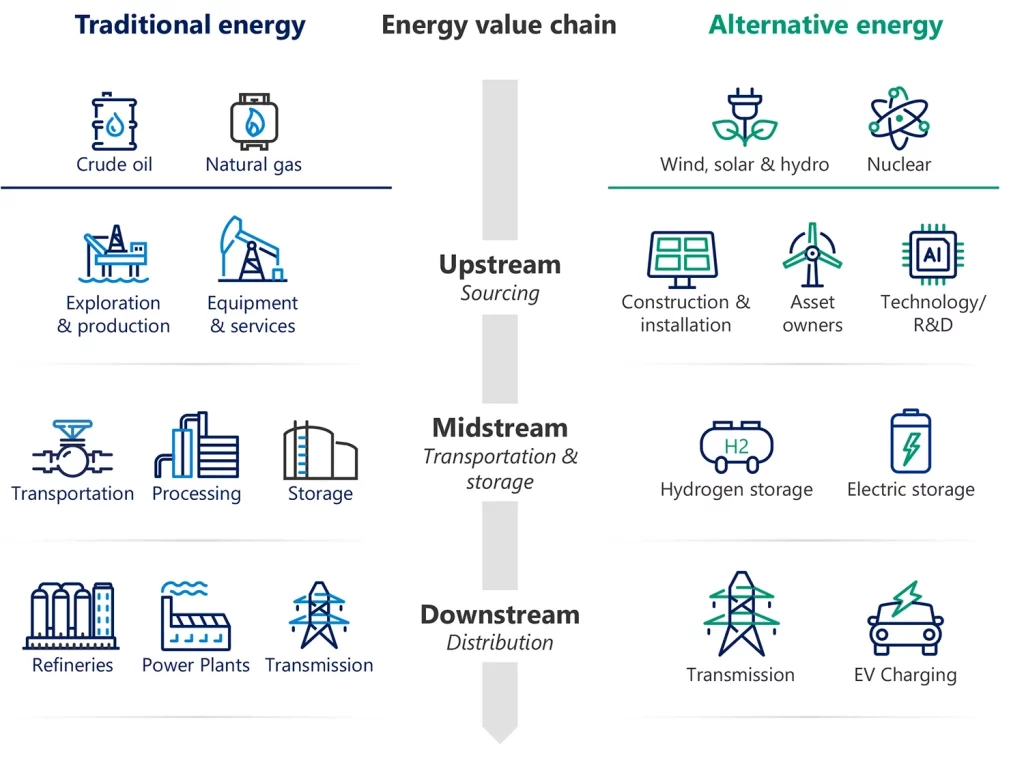

Understanding the Energy Value Chain

Upstream focuses on the exploration and extraction of oil, gas, and minerals, making it highly sensitive to commodity prices and supply conditions. In alternative energy, upstream centers on development, construction, and research and development.

Midstream enables the transportation and storage of energy through pipelines, terminals, and LNG facilities, as well as battery and storage systems in alternative energy markets.

Downstream includes refining, power generation, distribution, and utilities—where energy is delivered to consumers and businesses. In alternative energy markets, downstream also includes transmission buildout and EV charging infrastructure.

The future of energy: A shift in the energy narrative

Global demand for power is accelerating, fueled by long-term secular tailwinds: surging AI adoption, population growth and technological innovation.

Alternative energy is scaling rapidly, but traditional energy remains essential for reliability, infrastructure and baseload supply. Together, they form a more complex and capital-intensive system than in previous cycles.

It’s not longer about an energy transition. Markets need energy addition.

At March 31, 2026. Source: IEA and Cohen and Steers.

Current estimates based on consumption data from 2024

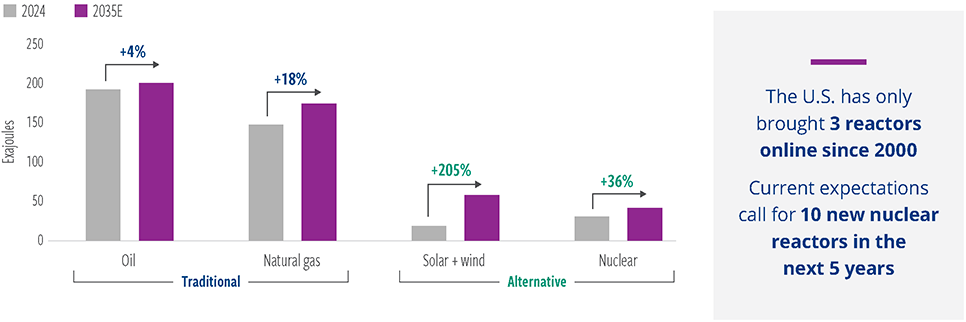

Meeting global energy needs requires growth across all segments of both traditional and alternative energy markets

Total projected global energy consumption by fuel

(2024-2035)

At March 31, 2026. Source: EIA, Department of Energy and Cohen & Steers.

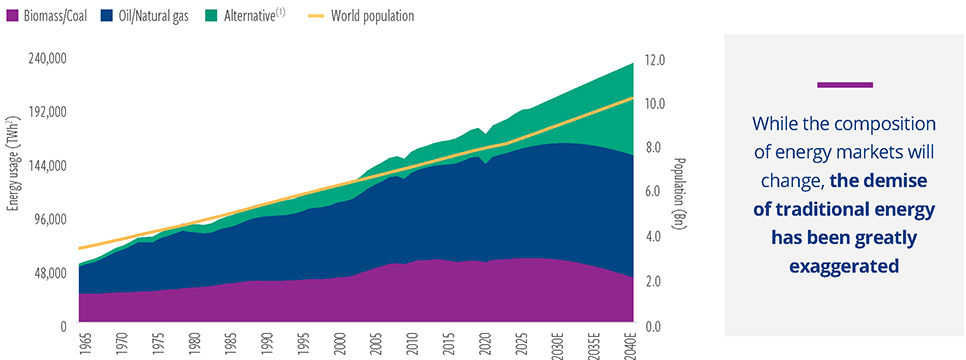

More of everything: the narrative around energy markets has evolved from energy transition to energy addition with both traditional and alternative sources playing a critical role

Forecasted energy demand by source

At March 31, 2026. Source: Our World in Data, Bloomberg and Cohen & Steers estimates.

The views and opinions are as of the date of publication and are subject to change without notice. There is no guarantee that any market forecast set forth in this presentation will be realized. (1) Alternative energy comprised of solar, wind, hydropower, nuclear and other renewable sources (2) Terawatt-hour.

What’s driving energy demand

Global energy consumption is set to reach unprecedented levels in the coming years driven by three factors.

- Population growth. We currently assume 0.9% population growth through 2040 given changing global demographics, resulting in a global population of 9.4 billion people in 2040. More people equals more energy demand.

- Economic growth. We maintain our current long term real GDP growth at 2.7% through 2040. Though growth is slowing, the real economy will continue to rise, again requiring more energy.

- Energy intensity of the economy. The most difficult part of the energy demand equation to estimate is the energy intensity of economic growth. Or said differently, how effective are we at converting a unit of energy input into a unit of economic output? The world has been on a robust, long-term improvement in energy efficiency. In 1965 energy/GDP was 3.66, which improved to 1.93 in 2025. In the last 50 years, energy intensity has declined by almost 50%. We expect that new technologies, government mandates and consumer preferences rewarding efficiency would drive us to 1.58 energy/GDP by 2040.

Population growth, economic expansion and accelerating electrification across households, industry and transportation are collectively driving a sustained increase in energy use across both developed and emerging markets. More recently, the rapid growth of artificial intelligence and need for data centers are powerful contributors. Together, these forces underscore a central reality: global energy demand is rising faster than the capacity of any one fuel or technology to serve it alone. Power systems must scale quickly while maintaining reliability, affordability and progress toward decarbonization objectives.

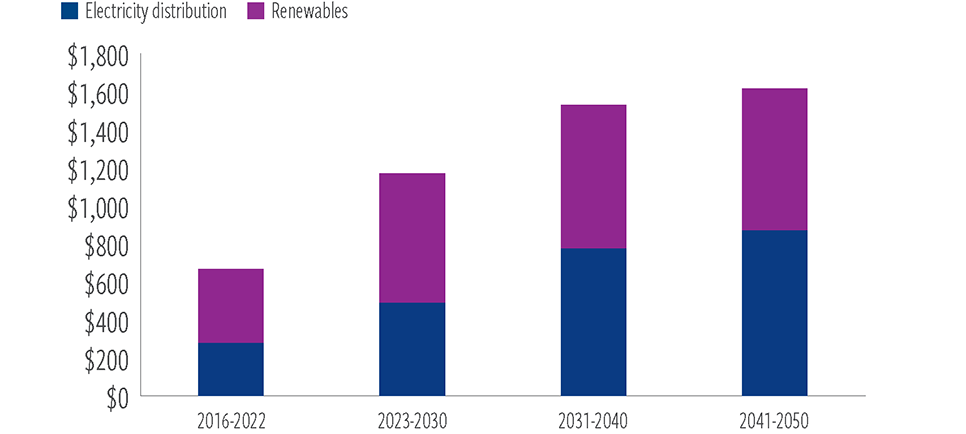

Record levels of capital are being committed to transmission, distribution and grid resilience

Average annual investment in grids and renewables, in $ billions

At September 30, 2023. Source: International Energy Agency, Cohen & Steers. Forecasts are inherently limited. There is no guarantee that any market forecast will be realized.

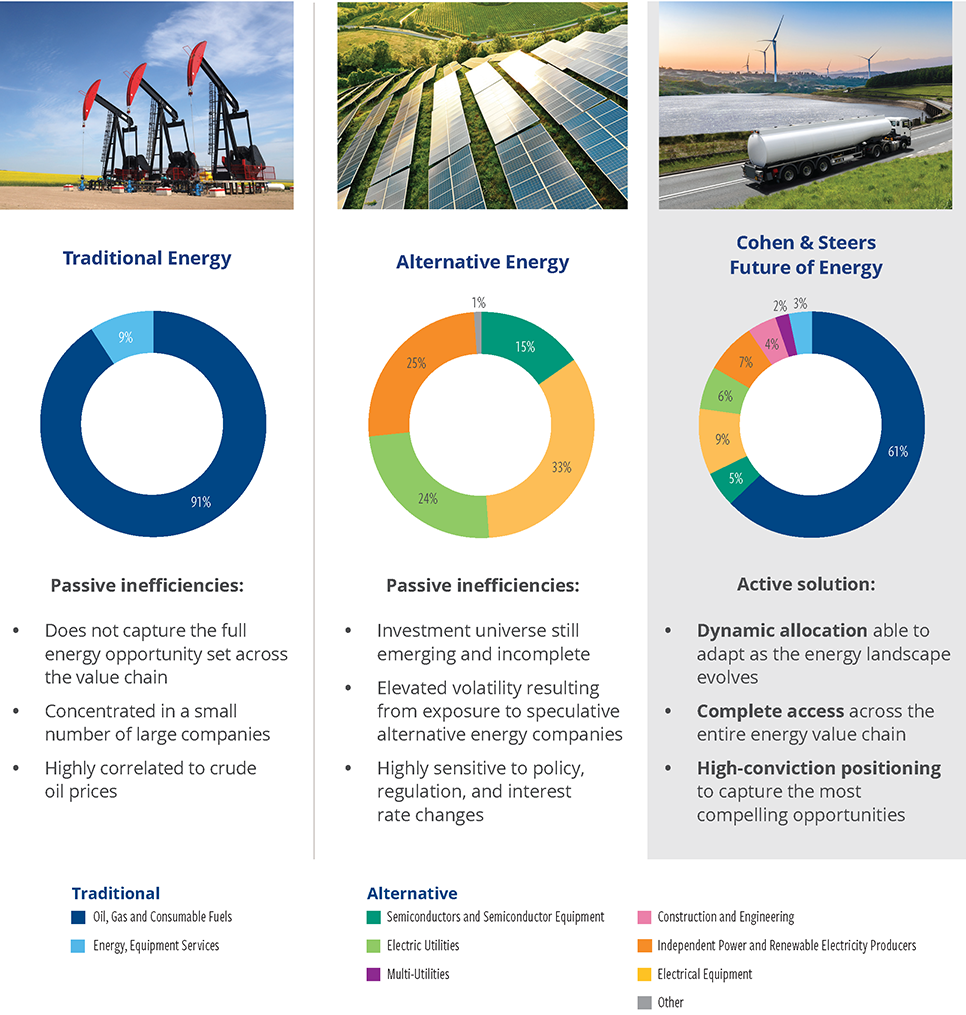

Why invest across the energy universe through active management

Expanding the energy universe to include both traditional and alternative energy allows access to the energy addition megatrend and mitigates single energy market risk factors.

At December 31, 2025. Source: S&P, Morningstar and Cohen & Steers.

News Coverage

How to Make Money From the Booming Demand for EnergyLearn more about our new fund

Index Definitions and Important Disclosures

The views and opinions are as of the date of publication and are subject to change without notice. This material represents an assessment of the market environment at a specific point in time, should not be relied upon as investment advice, is not intended to predict or depict performance of any investment and does not constitute a recommendation or an offer for a particular security. We consider the information in this presentation to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of suitability for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Please consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. A summary prospectus and prospectus containing this and other information may be obtained by calling 1.800.330.7348 or visiting cohenandsteers.com. Please read the summary prospectus and prospectus carefully before investing.

Energy Important Risk Considerations: Investing involves risk, including entire loss of capital invested. There can be no assurance that the investment strategy will meet its investment objectives. Diversification is not guaranteed to ensure a profit or protect against loss. An investment in the energy sector involves risks that differ from a similar investment in equity securities, such as common stock, of a corporation. Investors will subject to more risks related to the energy sector than if the Fund were more broadly diversified over numerous sectors of the economy. A downturn in the energy sector of the economy could have a larger impact on the Fund than on an investment company that does not concentrate in the sector. At times, the performance of securities of companies in the sector has lagged the performance of other sectors or the broader market as a whole. Energy sector investments can be volatile due to fluctuations in commodity prices, availability of resources, slowdowns in construction, reduced demand for energy products, regulatory changes, extreme weather or natural disasters, rising interest rates and geopolitical events. Special risks of investing in foreign securities include (i) currency fluctuations, (ii) lower liquidity, (iii) political and economic uncertainties, and (iv) differences in accounting standards. Certain foreign securities may represent small- and medium-sized companies, which may be more susceptible to price volatility and less liquid than larger companies. The Fund is classified as a "non-diversified" fund under the federal securities laws because it can invest in fewer individual companies than a diversified fund. However, the Fund must meet certain diversification requirements under the U.S. tax laws.