Strong demand is colliding with extremely low supply for open-air, necessity driven shopping centers.

KEY TAKEAWAYS:

- The third quarter of 2024 represented a trough in private real estate, which has now had positive returns four quarters in a row.

- While private real estate continued to reprice in 2024, we determined there was one property sector in particular that bottomed first: open-air, necessity driven shopping centers where strong demand is colliding with extremely low supply.

- Recent retail bankruptcies may be generating interesting headlines, but this is actually an opportunity as strong tenants looking for premium space take over these properties at significantly higher rents.

1) The private real estate cycle

At the start of last year, we said we were entering an attractive point in the real estate cycle. That appears to be playing out in real time.

We’ve long argued that listed REITs are leading indicators to private in both downturns and recoveries, and this cycle has been no exception.

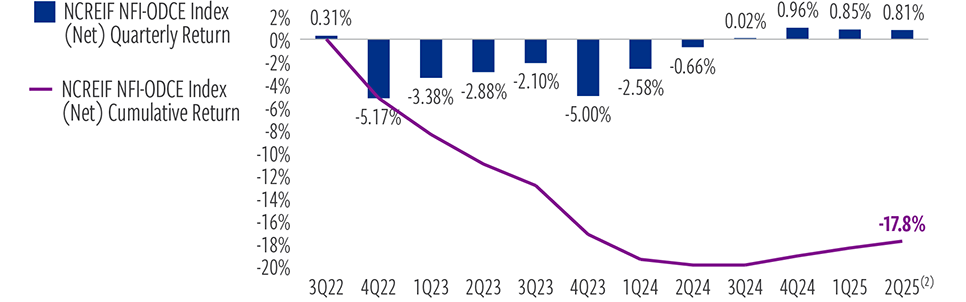

We expected private real estate to lag listed REITs by about a year. And indeed, listed REITs bottomed in October 2023, and private real estate hit bottom about one year later, on average across sectors, which you can see in this chart (Exhibit 1). Private real estate returns, as measured by the NCREIF ODCE index, were negative for seven straight quarters, dating back to the end of 2022. However, modest positive returns in the third quarter of 2024 represented a trough, and the index has since had positive returns four quarters in a row.

EXHIBIT 1

We believe the NFI-ODCE Index bottomed in 2Q 2024

Quarterly returns of the NCREIF NFI-ODCE Index (Net) since 3Q22 (post-Covid peak)(1)

At June 30, 2025. Source: NCREIF, Cohen & Steers. Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict when such a trend might begin. There is no guarantee that any market forecast set forth in this presentation will be realized. (1) Private real estate represented by the NCREIF NFI-ODCE Index (Net). (2) Q2 returns are preliminary.

2) Open-air shopping centers

This leads to the second point we’re watching this month.

While private real estate continued to reprice in 2024, we determined there was one property sector in particular that bottomed before the others: open-air, necessity driven shopping centers.

Strong demand for open-air shopping centers is colliding with extremely low supply, resulting in high occupancy rates and strong and durable rental growth.

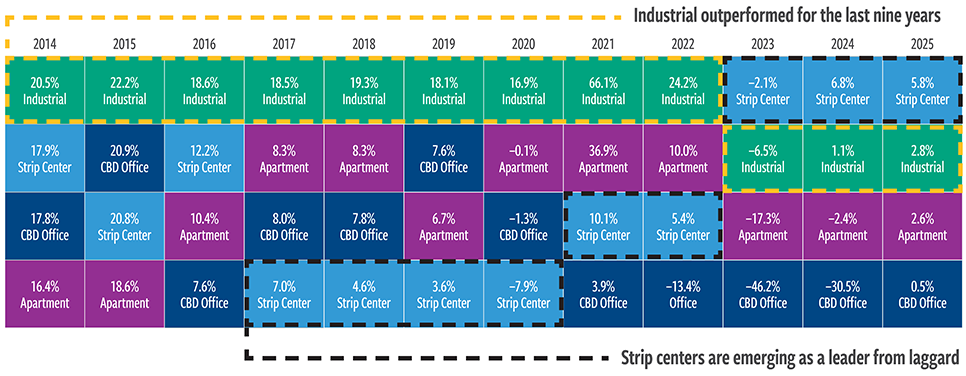

Open-air shopping centers (classified as “strip centers” by NCREIF) have now outperformed other private sectors over the past two and a half years, as you can see in this chart (Exhibit 2).

EXHIBIT 2

Performance patterns in private real estate

At June 30, 2025. Source: NCREIF, Cohen & Steers. Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict when such a trend might begin. There is no guarantee that any market forecast set forth in this presentation will be realized.

This has been consistent with our view that last cycle’s winners (notably, multi-family apartments and industrial warehouses) were likely to give way to last cycle’s laggards, such as shopping centers, that would rebound due to undervaluation and favorable supply/demand dynamics.

That is a stark contrast from nearly a decade ago, when talk of the retail apocalypse dominated the news headlines. However, the pace of new retail shopping center construction has remained the lowest of any major property type.

Meanwhile, retail sales grew reliably, steadily at 3% annually even as store growth, as measured by square footage of stores out there, remained less than 1% for more than a decade.

At the same time, the most adaptable and well-managed retailers, such as Walmart and Target and others, are really thriving today. Grocery stores, the largest component of brick-and-mortar retail, have proven to be impenetrable by warehouse distribution.

As a result, open-air shopping centers are the only major property type with accelerating rental rate growth.

3) Property demand and higher rents

Finally, we’d like to discuss one question we hear from investors who have seen recent retail bankruptcies, like Joann’s, Party City, The Container Store or TGI Friday’s, generating interesting headlines.

But the fact that these potential tenants are closing down doesn’t represent a slowdown in retail property demand overall. This is actually an opportunity due to the extremely high occupancy levels currently in properties in the high 90% range.

Properties that have tenants such as these can improve rents and upgrade the overall credit quality of properties by replacing these tenants. The supply/demand dynamic mentioned earlier means that the retailers that are thriving have limited options in high quality properties in high-growth communities.

In fact, strong tenants looking for premium space are looking to take over properties from these weaker tenants at significantly higher rents. That development contributes to what we already see as a favorable opportunity in the new private real estate cycle to put fresh capital to work.

Watch August 2025 The Real Estate Reel: Three indications private real estate has found its bottom.

Watch all The Real Estate Reel videos.

ABOUT THE AUTHORS

James Corl, Executive Vice President, is Head of the Private Real Estate Group.

Data quoted represents past performance, which is no guarantee of future results. The information presented does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this video will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

This video is for informational purposes and reflects prevailing conditions and our judgment as of June 2025, which are subject to change. This material should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this video to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Risks of Investing in Private Real Estate

Private real estate investments are illiquid and susceptible to economic slowdowns or recessions and industry cycles, which could lead to financial losses and a decrease in revenues, net income and assets. Lack of liquidity in the private real estate market makes valuing underlying assets difficult. Appraisal values may vary substantially from a price at which an investment in real estate may actually be sold.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, U.S. endowments, foundations and mutual funds. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.