Welcome to the Real Estate Reel from Cohen & Steers.

KEY TAKEAWAYS

- Rate hikes are not our base case, but even just with the possibility of additional hikes, investors are once again asking: what does this mean for real estate?

- Periods of rising rates are typically driven by a strengthening economy, typified by improving GDP growth, job creation, and capacity constraints, which can lead to inflationary pressure. Those same forces tend to support real estate fundamentals.

- Rents are the primary driver of REIT cash flows-and ultimately, returns. And today, fundamentals remain strong, supply is tightening, and the economy is resilient. This pricing power translates directly into income through rising rents for property owners.

Sticky inflation and resilient growth have reshaped the outlook for monetary policy.

Rate cuts are now less likely, and watchers of the Federal Reserve are even speculating on the possibility of rate hikes.

In fact, the bond market is pricing in expected hikes by year end.

Rate hikes are not our base case, but even just with the possibility of additional hikes, investors are once again asking: what does this mean for real estate?

At first glance, rising rates may seem like a headwind for REITs.

When interest rates rise, borrowing becomes more expensive, which can pressure earnings and valuations.

As Treasury yields move higher, income-focused investors may compare REIT dividends to “risk-free” yields—and potentially rotate away from REITs.

Higher rates can lead to higher discount rates, which can compress asset values and REIT share prices, particularly in the short term.

Some investors think they should avoid REITs when interest rates are rising.

But history and current fundamentals tell a more nuanced story.

Periods of rising rates are typically driven by a strengthening economy, typified by improving GDP growth, job creation, and capacity constraints, which can lead to inflationary pressure.

And those same forces tend to support real estate fundamentals.

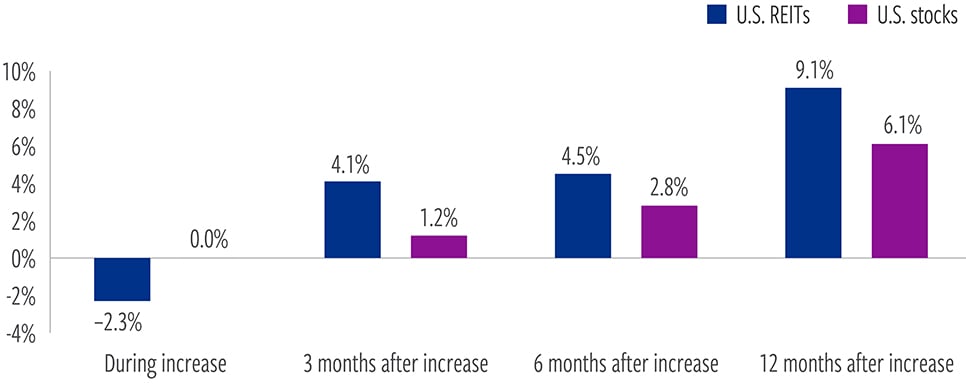

U.S. REITs outperform stocks after real rates rise

At May 31, 2026. Source: Bloomberg, Morningstar, CNS proprietary system. Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin.

In fact, history shows that the direction of the economy and job growth has had a greater impact on REIT performance than interest rates themselves.

That’s because the environment pushing rates higher is often the same environment driving rents higher.

Rents are the primary driver of REIT cash flows—and ultimately, returns.

And today, fundamentals remain strong.

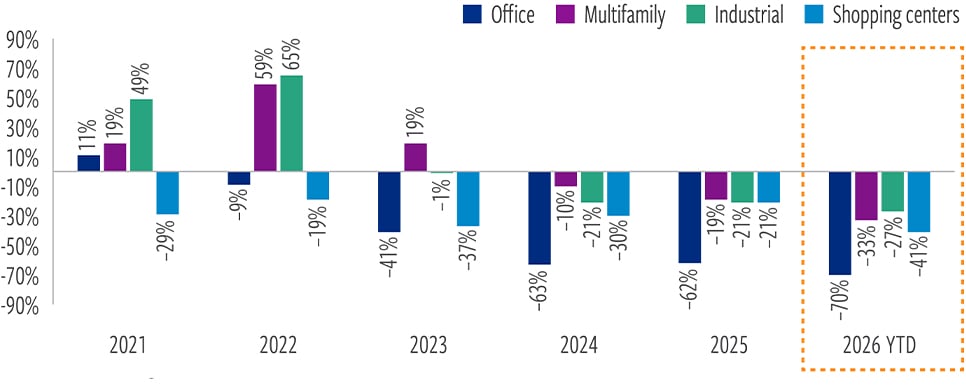

Tight supply should drive rental growth

U.S. construction starts vs. 10-year average by sector (% of inventory)(1)

At March 31, 2026. Source: CoStar, Cohen & Steers.

(1) Average of four quarters construction starts as a percentage of inventory by sector.

Supply is also tightening. In fact, 2026 is shaping up to be the third year in a row in which U.S. construction starts are below their 10-year average.

Meanwhile, unemployment is still near historic lows, job creation continues, and millions of jobs remain unfilled, supporting demand across the economy.

This pricing power translates directly into income through rising rents for property owners.

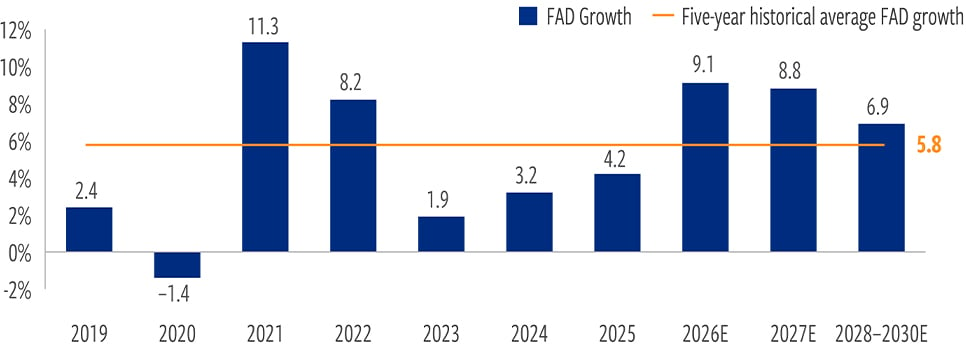

Cash flow growth expected to accelerate

Growth in funds available for distribution (FAD) — US REITs (%)

At March 31, 2026, unless otherwise noted. Source: Bloomberg and Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results.

Historical cash flow growth shows the weighted average funds available for distribution (FAD) growth by year. Data is from Cohen & Steers. Cohen & Steers data excludes FAD growth outliers of =/-100% and is based on the constituents of the FTSE Nareit All Equity REITs Index. The FTSE Nareit All Equity REIs Index contains all tax-qualified REITs with more than 50% of total assets in qualifying real estate assets other than mortgages secured by real property that also meet minimum size and liquidity criteria.

Cash flow growth—measured by funds from operations—is expected to exceed historical averages, highlighting the strength of underlying fundamentals.

Listed real estate also has distinct characteristics that can help provide a buffer to inflation.

For example, sectors with shorter lease durations (such as self storage) have the ability to reset rents promptly as conditions change.

Furthermore, though inflation hurts company profits when costs rise faster than revenues, REITs typically enjoy operating margins of around 60%, reducing the effect of higher costs.

In addition, higher costs for land, materials and labor can reduce the potential profits of development, raising the economic barriers to new supply and reducing potential competition for existing properties.

So while interest rates may dominate the headlines, they are not the primary driver of REIT performance.

Rising rents are.

And in today’s environment where inflation remains elevated and fundamentals remain intact, real estate may be better positioned than many investors expect.

Click here to subscribe to our latest insights.

ABOUT THE AUTHORS

Seth Laughlin, Senior Vice President, is Head of Real Estate Strategy & Research, responsible for identifying allocation opportunities in both listed and private real estate and related thematic and strategic research.

Index definitions / important disclosures.

Rising rate periods are from 1/1/2000 through 6/10/26. These rising-yield periods are 5/4/2000- 6/8/2000, 6/26/2001- 7/27/2001, 11/15/2001- 1/4/2002, 3/18/2003- 4/17/2003, 6/25/2003- 8/28/2003. 4/2/2004- 5/21/2004, 3/7/2005- 4/8/2005, 7/1/2005- 8/12/2005, 9/30/2005- 12/13/2005, 3/3/2006- 5/8/2006, 12/22/2006- 1/30/2007, 5/11/2007- 7/9/2007, 3/31/2008- 5/16/2008, 9/12/2008- 11/7/2008, 11/8/2010- 1/7/2011, 5/1/2013- 7/19/2013, 11/18/2013- 1/3/2014, 5/1/2015- 6/18/2015, 8/21/2015- 9/17/2015, 10/24/2016- 12/30/2016, 1/9/2018- 3/7/2018, 9/10/2018- 11/16/2018, 2/16/2021- 3/24/2021, 9/13/2021- 10/21/2021, 1/3/2022- 2/25/2022, 3/24/2022- 6/3/2022, 8/26/2022- 10/25/2022, 5/1/2023- 6/23/2023, 9/19/2023-11/1/2023, 4/1/2024- 5/13/2024, 10/4/2024-11/27/2024.

Data quoted represents past performance, which is no guarantee of future results. The information presented does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this video will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

This video is for informational purposes and reflects prevailing conditions and our judgment as of June 2026, which are subject to change. This material should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this video to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, U.S. endowments, foundations and mutual funds. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.