Welcome to the Real Estate Reel from Cohen & Steers.

After several years of a real pricing reset, U.S. real estate is showing some pretty encouraging signs these days. And in our view, in particular, shopping centers, we think are going to benefit the most in this environment.

KEY TAKEAWAYS

- Open‑air, necessity‑driven shopping centers are in a profound state of disequilibrium where very resilient demand and high occupancy levels are meeting extremely low supply.

- However, real estate developers are still focused on building industrial warehouses and apartment complexes, which is creating opportunity for owners and investors in these shopping centers.

- Existing shopping centers have become increasingly difficult to replace, scarce, and more valuable, shifting pricing power for rents back to the owners of these well‑located, necessity‑driven centers.

Welcome to the Real Estate Reel from Cohen & Steers.

After several years of a real pricing reset, U.S. real estate is showing some pretty encouraging signs these days. And in our view, in particular, shopping centers, we think are going to benefit the most in this environment.

When we talk about shopping centers, we’re talking about something very specific.

We mean open-air, necessity-driven shopping centers. Not malls. We’re talking about centers anchored by essential retail, like grocery stores, Wal-Marts, Targets, everyday services that drive significant foot traffic, where the stores and parking are all at ground level.

These properties are designed for convenience and the everyday needs of the consumer, and centers that play an essential role in the communities around them.

We believe this segment offers the best combination today of great fundamentals and attractive valuations within the realm of private real estate today.

1. Low supply meeting high demand

Last cycle’s winners—apartments and warehouses—they benefited from strong demand last cycle for a long time, but now those strong demand drivers are fading. And at the same time, they have been overwhelmed by a huge wave of new construction, new supply.

On the other hand, necessity driven shopping centers have not had this new supply wave, so their asset prices do not reflect the positive supply and demand situation that has evolved there.

Today, we would characterize shopping centers as having migrated into this state of what I would call a profound disequilibrium where there’s very resilient demand and high levels of occupancy but with extremely low new construction or new supply.

This is what creates the conditions for an extended period of very strong pricing power for owners of these properties.

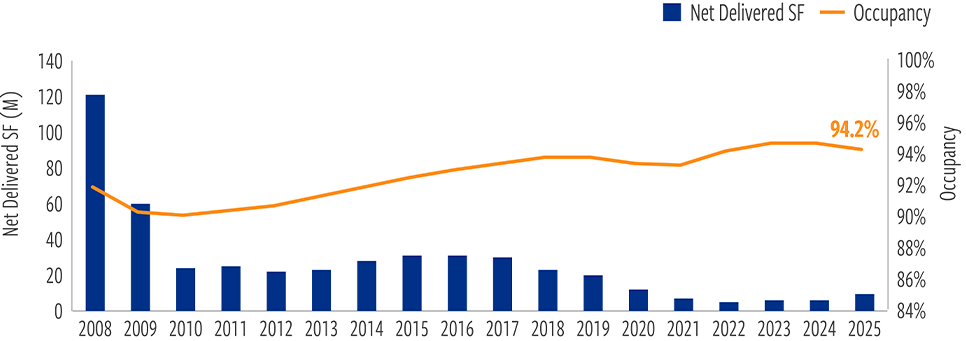

National occupancy in shopping centers has returned to all time highs, around 96%.

At the same time, open air shopping centers have the lowest visible new construction pipeline of any major property type.

Declining retail supply has helped drive higher occupancy

Retail construction vs occupancy (2008–2025)

At December 31, 2025. Source: CoStar. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The views and opinions above are as of the date of this publication and are subject to change without notice.

2. The role of parking lots

This is where the structure of open air, necessity driven shopping centers really matters. Shopping centers make relatively inefficient use of land at a prominent intersection compared with other property types.

These centers require stores and parking to be at ground level. Municipal requirements mandate lots of parking, high parking ratios, which really limit how much rentable space can be built on any given piece of land.

For real estate developers, this creates a clear, inescapable economic reality.

Apartments can stack units vertically. The cars can go in parking garages. Warehouses require minimal parking and generate far more rentable square footage per acre as a result.

At the same time, these property types are trading at much higher multiples than shopping centers, or the income coming off of apartments and warehouses trade at a higher multiple in the marketplace than for a shopping center.

So when developers are evaluating a site, building a new open air shopping center is last on the list. It simply doesn’t make sense. You can make more money doing something else, building more rental space that will trade at a higher multiple, and we expect that to persist for some time.

And that’s exactly where the opportunity lies for owners and investors in these shopping centers. If it doesn’t make sense to build a new one, then the existing centers, they are increasingly difficult to replace, they are scarce, and they’re more valuable.

Successful retailers that are looking to expand, of which there are many today, now have very limited options to try to reach the customers they want to front face in person.

As demand continues and alternatives remain limited, pricing power shifts back to the owners of these well located, necessity driven centers.

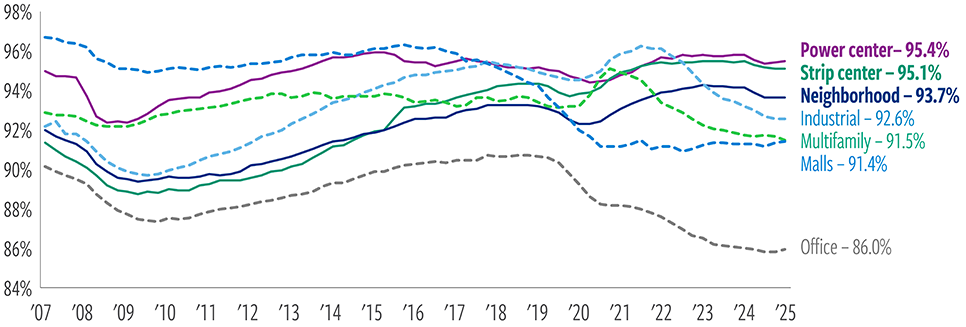

Open air shopping center occupancy is the highest of major property types

Successfully rebounded from the retail apocalypse

At December 31, 2025. Source: CoStar. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The views and opinions above are as of the date of this publication and are subject to change without notice.

3. Last-mile delivery

At the same time, retail is also evolving. Many necessity-based retailers now use physical stores to fulfill their online orders, effectively turning these locations into last mile pieces of infrastructure, or last-mile warehouses. That further reinforces the value of open-air shopping centers that serve everyday needs

That’s why we continue to focus on open air, necessity driven shopping centers—properties we believe are positioned for durable cash flow growth, supported by limited new supply, strong tenant demand, and favorable demographic trends.

Watch April 2026 The Real Estate Reel: Listed REITs: A strong start to 2026 and what’s driving performance

Watch all The Real Estate Reel videos.

ABOUT THE AUTHORS

James Corl, Executive Vice President, is Head of the Private Real Estate Group.

Data quoted represents past performance, which is no guarantee of future results. The information presented does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this video will be realized. There is no guarantee

that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

This video is for informational purposes and reflects prevailing conditions and our judgment as of June 2025, which are subject to change. This material should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this video to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Risks of Investing in Private Real Estate: Private real estate investments are illiquid and susceptible to economic slowdowns or recessions and industry cycles, which could lead to financial losses and a decrease in revenues, net income and assets. Lack of liquidity in the private real estate market makes valuing underlying assets difficult. Appraisal values may vary substantially from a price at which an

investment in real estate may actually be sold.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, U.S. endowments, foundations and mutual funds. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.