REIT fundamentals are accelerating and earnings are strong

KEY TAKEAWAYS:

- Listed REITs are off to a strong start for the first two months of 2026, meaningfully outperforming broader equity markets in the U.S. and globally.

- Three forces are driving this performance: Accelerating fundamentals, strong earnings, and a supportive macroeconomic backdrop.

- One risk we are watching closely is the conflict involving Iran. We believe listed real estate is an attractive allocation in an environment defined by lower growth and greater uncertainty.

Welcome to the real estate reel from Cohen & Steers.

1. Early 2026 performance

Listed REITs are off to a strong start for the first two months of 2026, meaningfully outperforming broader equity markets in the U.S. and globally.

In February alone, U.S. REITs gained roughly 7.5%, well ahead of broader equities.

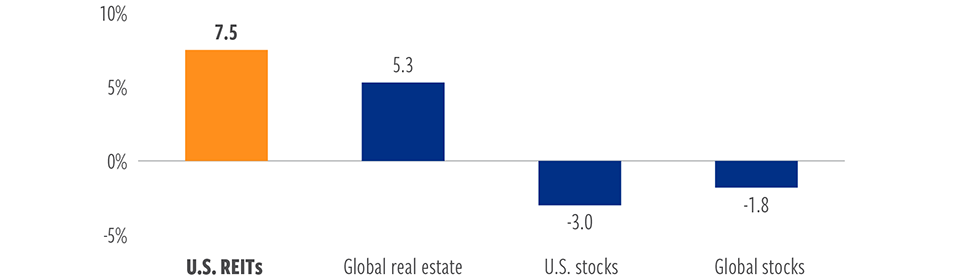

Real estate has outperformed equities to start the year

YTD performance through 3/18/26

At March 18, 2026. Source: Bloomberg. Data quoted represents past performance, which is no guarantee of future results.

Year-to-date returns through mid-March of 6.4% are solid, particularly compared to 2025 when U.S. REITs returned 2.3% overall.

On a global basis, real estate stocks rose 7.0% in February, and have a year-to-date return of 5.3%, after gaining nearly 10% in 2025.

And while the initiation of hostilities in Iran has driven lower, which I will discuss a little later, REITs have maintained their initial lead over broader equities.

2. Three forces driving REIT performance

First, fundamentals are accelerating where supply is constrained.

Data centers and health care led the market to start the year as earnings and outlooks surprised to the upside.

Data center REITs benefited from clear evidence of rising hyperscaler spending tied to AI and cloud demand, while senior housing continued to see strong growth and pricing power amid demand from aging baby boomers.

Second, earnings have been solid.

Roughly half of U.S. REITs beat consensus expectations during the recent reporting season, reinforcing confidence in the durability of cash flows even as economic growth moderates.

And third, the macro backdrop turned more supportive prior to the conflict in the middle east.

Bond yields had moved lower during the month, and investors increasingly recognize that REIT valuations are compelling relative to broader equities—particularly given their lease based, largely domestic income streams.

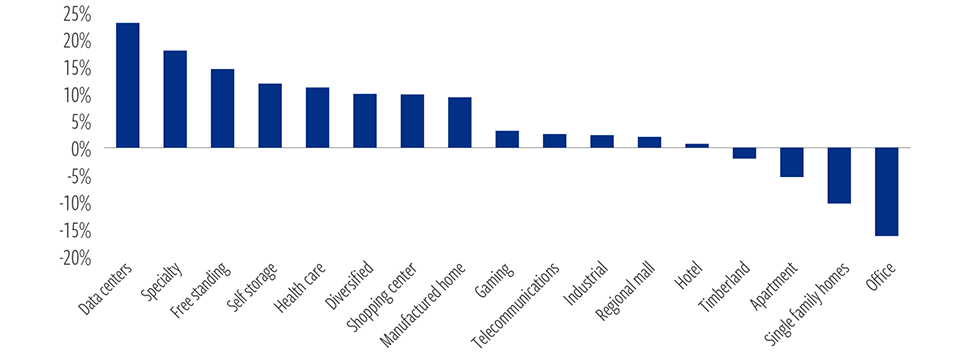

YTD performance has varied widely by sector

Performance through 3/25/26

At March 15, 2026. Source: Bloomberg. Data quoted represents past performance, which is no guarantee of future results.

Leadership has been concentrated in sectors where fundamentals are improving or cash flows remain defensive, including data centers, senior housing, self-storage and retail, particularly shopping centers, benefiting from resilient consumer spending.

At the same time, dispersion has remained pronounced. Apartments, single‑family rentals, and office have underperformed as investors remain cautious around supply overhangs, slower rent growth, and longer‑term demand uncertainty, particularly in sectors most exposed to potential impacts to employment from AI.

The dispersion we’re seeing across sectors reinforces why selectivity matters and why active positioning is critical.

3. Conflict in Iran

One risk we are watching closely is the intensifying conflict involving Iran.

Recent developments have disrupted energy markets and global supply chains, driving sharp swings in oil and natural gas prices and introducing inflation volatility.

Historically, energy price shocks pass quickly into headline inflation, and if sustained, can influence interest‑rate expectations and financial conditions. Visibility remains limited, and volatility across global markets has increased.

For listed real estate, the impact is indirect but important. REITs are relatively well positioned in periods of lower growth and macro uncertainty due to stable, lease‑based cash flows and limited exposure to global trade.

The primary risk — consistent with broader markets — would be a prolonged conflict that increases stagflationary pressures and delays expected rate cuts.

Looking ahead, we believe listed real estate is an attractive allocation in an environment defined by lower growth and greater uncertainty because of its durable income profile I mentioned but also due to its exposure to long‑term secular themes like digital infrastructure and demographics.

Subscribe to the Real Estate Reel via the link on screen and tune in next month to see what we’re watching next.

Watch January 2026 The Real Estate Reel: Next-Gen real estate is driving growth in the REIT market

Watch all The Real Estate Reel videos.

ABOUT THE AUTHORS

Seth Laughlin, Senior Vice President, is Head of Real Estate Strategy & Research, responsible for identifying allocation opportunities in both listed and private real estate and related thematic and strategic research.

Data quoted represents past performance, which is no guarantee of future results. The information presented does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this video will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

This video is for informational purposes and reflects prevailing conditions and our judgment as of June 2025, which are subject to change. This material should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this video to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, U.S. endowments, foundations and mutual funds. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.