Data storage, changing demographics and a revolution in retail shopping are reshaping real estate.

Key Takeaways:

- The data storage and infrastructure market is expected to grow by 160% by 2034, driven by significant trends including the growth of artificial intelligence and cloud platforms.

- The population of Americans over 85 years in age is expected to double by 2040, driving strong occupancy growth and pricing power for senior housing and nursing facilities.

- In 2010, only 2 percent of ecommerce sales were fulfilled at stores rather than at warehouses. By the end of this year, that figure is forecast to rise to 34%, driving a renewed supply-demand imbalance in select retail properties.

This month, we’re looking closer at three trends driving real estate investing today.

Welcome to the Real Estate Reel from Cohen & Steers.

1) Data storage

First, the data storage and infrastructure market is expected to grow by 160% by 2034, driven by significant trends including the growth of artificial intelligence and cloud platforms.

In fact, one of our analysts referred to the demand for data centers as nearly “insatiable.”

This is coming from hyperscalers, such as Microsoft, META, Google, Amazon and Oracle, many of whom continue to increase cap ex spending, which is driving data center demand.

According to Green Street, capital expenditure guidance for 2025 increased by a combined $30 billion versus last quarter. And these companies signaled next year’s capital spending will handily outpace this year’s record pace.

At the same time, supply is constrained by limitations on power infrastructure to key data center markets. This has resulted in the strongest rent growth in a decade and vacancy rates that are still less than 3% on average nationally.

Market expectations for data centers have driven strong recent performance of the sector, with 25% and 30% returns in 2024 and 2023, respectively, but this year data centers have declined 6.5% through the third quarter as valuations have climbed. Supply will eventually meet demand, but given the cost, power constraints and lead times needed, we expect to see demand to exceed supply for the next several years.

2) Changing demographics

Second, the population of Americans over 85 years in age is expected to double by 2040.

That’s nearly 15 million people who will likely need senior housing and care.

We expect that to translate to strong occupancy growth and pricing power, as occupancy continues to climb above its pre-pandemic levels and supply remains constrained.

Let’s take a closer look at recent results from Q3, which underscore this momentum.

Assisted living occupancy rose 90 basis points quarter-over-quarter and 240 basis points year-over-year. Independent living communities also posted solid occupancy gains of +50bps quarter over quarter and +200bps year over year.

This growing demand is meeting constrained new supply. Assisted living construction activity is at its lowest level in 14 years, down -25% year over year, while independent living supply also declined -6% year over year.

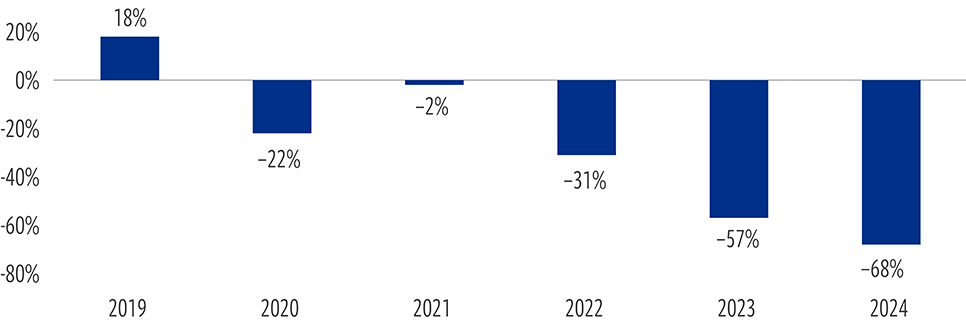

In fact, senior housing construction starts have declined every year since 2020 with a 68% drop in 2024 and a 57% drop in 2023, according to CoStar, which you can see in this chart.

This tightening pipeline supports pricing power. As one measure, for example, revenue per occupied room continues to climb.

This is particularly notable in skilled nursing facilities. Reimbursement growth, which refers to the increase in payments received from government programs (like Medicare and Medicaid) and private insurers for the care provided to residents, is at its highest level in the 18-year history of this data.

That’s significant because reimbursements are the primary revenue source for skilled nursing facilities. Q3’s reimbursement growth of 5.2% is up significantly from Q2’s growth of 4.8%, which at the time was a record.

Stronger-than-normal occupancy gains, rising revenues, and limited new inventory—highlight how demographic shifts are not only fueling demand but also creating a favorable operating environment for senior housing operators and investors.

Tight supply should benefit rent growth for senior housing

U.S. construction starts vs. 10-year average (% of inventory)(1)

At December 31, 2024. Source: CoStar. Data quoted represents past performance, which is no guarantee of future results.

(1) Average of four quarter construction starts as a percentage of inventory by sector.

3) Retail revolution:

Third, I want to share a stat on a key trend in retail, but let’s first take a look back in time.

The outlook for retail stores darkened over the course of the 2000s when sales started slowing. Then construction financing dried up in 2008.

The proliferation of ecommerce followed and accelerated during the pandemic.

But reports of the death of the store were greatly exaggerated.

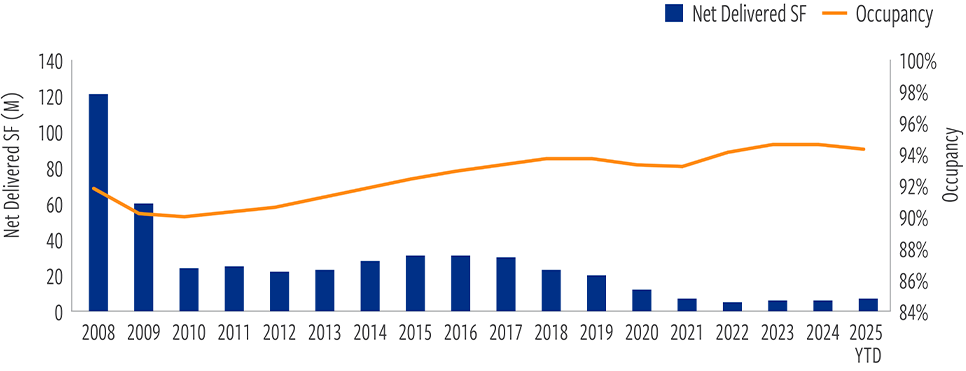

For starters, the pace of new retail shopping center construction has remained the lowest of any major property type.

Meanwhile, retail sales grew steadily at 3% annually even as store growth, as measured by square footage of stores, remained less than 1% for more than a decade.

Strong demand is now colliding with extremely low supply growth, resulting in high occupancy rates and strong rent growth for select retail properties. In fact, Bank of America just reported retail had record leasing for the second year in a row.

At the same time, the strongest retailers didn’t just survive the apocalypse. They have shifted to models more resilient to e-commerce threats.

Omni-channel retailing—including “click-and-collect,” with physical stores supporting online order fulfillment—has become the new reality.

A majority of Target’s and Walmart’s online orders are now fulfilled from its stores, and Home Depot, has shown that nearly half of its online orders are fulfilled in its stores.

The key stat I alluded to earlier? In 2010, only 2 percent of ecommerce sales were fulfilled at stores rather than at warehouses. By the end of this year, that figure is forecast to rise to 34%.

Customers are more willing than ever to walk or drive to the stores themselves to pick up their orders, and warehouse fulfillment has stopped taking volume from store-based fulfillment. This benefits not only the major retailers themselves but the entire shopping centers around them.

We expect accelerating rent growth as strong demand meets very limited supply, though at present valuations for many retail REITs have become a little stretched.

Declining retail supply has helped drive higher occupancy

Retail construction vs occupancy (2008-3Q25)

As of September 30, 2025. Source: CoStar. Reflects Neighborhood Centers, Power Centers and Strip Centers. Data quoted represents past performance, which is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The views and opinions above are as of the date of this publication and are subject to change without notice.

Watch October 2025 The Real Estate Reel: Why global real estate is now outperforming the U.S.

Watch all The Real Estate Reel videos.

ABOUT THE AUTHORS

Brian Cordes, CAIA, Senior Vice President, is the head of Cohen & Steers’ Portfolio Specialist Group, which represents the company’s investment teams in interactions with institutional and retail clients.

Data quoted represents past performance, which is no guarantee of future results. The information presented does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this video will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

This video is for informational purposes and reflects prevailing conditions and our judgment as of June 2025, which are subject to change. This material should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this video to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Risks of Investing in Private Real Estate

Private real estate investments are illiquid and susceptible to economic slowdowns or recessions and industry cycles, which could lead to financial losses and a decrease in revenues, net income and assets. Lack of liquidity in the private real estate market makes valuing underlying assets difficult. Appraisal values may vary substantially from a price at which an investment in real estate may actually be sold.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, U.S. endowments, foundations and mutual funds. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.