After years of U.S. dominance, global real estate is staging a comeback—reshaping investor expectations and allocations.

KEY TAKEAWAYS:

- International REITs are outperforming the U.S. for first time since 2017, led by Asia and Europe.

- Discounted valuations, maturing sectors, and supportive policies are driving global real estate’s strong rebound.

- Diversification is essential amid varied macro trends and secular growth drivers.

1) Outperformance of international real estate

Global real estate is on pace to outperform U.S. real estate for the first time since 2017.

Through the third quarter of this year, global REITs are up 10.4%, compared with U.S. REITs, which are up 4.5% over the same period.

What’s notable, given that U.S. markets account for over 60% of global real estate, is how strongly Asia Pacific, Europe and emerging markets have performed.

Asia Pacific leads with a 27.4% gain, followed by Europe at 17.9% and emerging markets at 16.2%.

This is in stark contrast to recent history, when the U.S. served as a safe haven, offering solid growth compared with global markets. Asia faced political turmoil, and Europe struggled with slower growth.

Over the past five years, U.S. REITs returned 7% annually, while Europe and emerging markets had negative annual returns, and Asia posted just 3.5% returns.

This year marks a reversal of recent trends.

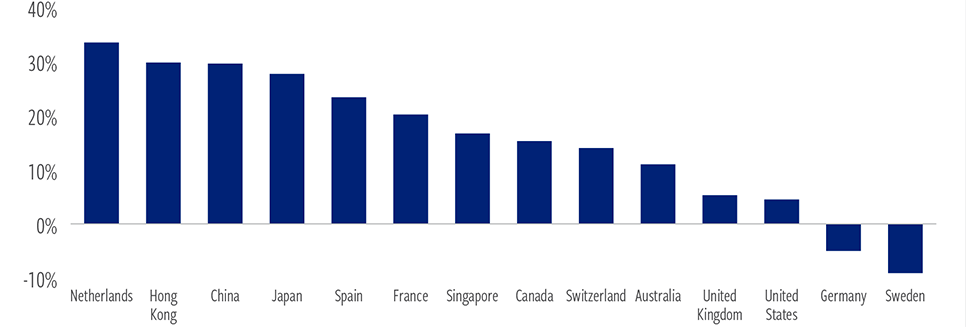

While political uncertainty has dampened U.S. growth expectations, international markets are benefiting from a significantly improved outlook. For example, after four consecutive years of double-digit negative returns, China has returned nearly 30% on indications growth there has bottomed. Japan, Spain, Hong Kong, and the Netherlands have also all posted returns of more than 20% this year.

Dispersion of country returns

Country total returns in local currency-YTD 2025(1)

At September 30, 2025. Source: Cohen & Steers.

Data quoted represents past performance, which is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin.

(1) The FTSE EPRA Nareit Developed Real Estate Index – net is an unmanaged market-capitalization-weighted total-return index, which consists of publicly traded equity REITs and listed property companies from developed markets and is net of dividend withholding taxes.

2) What’s driving global outperformance

Favorable valuations, improving fundamentals, and a positive macroeconomic backdrop for many countries are behind the comeback in international markets.

First, Europe and Asia were trading at glaringly discounted valuations at the start of the year.

U.S. REITs began the year trading at a slight premium to net asset values. By comparison, our European and Japanese universe was trading at 23 and 29% discounts, respectively.

Those discounts have since narrowed slightly, but we believe international REITs are still relatively attractive.

Second, in Europe and Asia, most alternative sectors—such as data centers, storage, towers, and health care— are still maturing, creating favorable supply-demand dynamics.

Heightened external uncertainty is also prompting governments across Europe and Asia to adopt more proactive policies to stimulate domestic consumption to support economic growth. And in Japan specifically, companies are placing greater emphasis on corporate governance and reform initiatives aimed at enhancing shareholder returns. We see this theme broadening out across Asia.

3) Our real estate outlook

Where do we go from here?

While some uncertainty remains, such as whether Europe can increase productivity and promote economic growth, we believe global REITs are well positioned.

Most countries still trade at significant discounts to NAV. Balance sheets remain strong. And we believe investors have been overallocated to the U.S., so some normalization can continue.

None of this is to say we believe U.S.-listed real estate is expected to underperform. Global markets are just catching up.

In fact, some of the same tailwinds we see internationally are trends that are favorable for U.S. REITs that are still trading at notable discounts relative to the broader equities market.

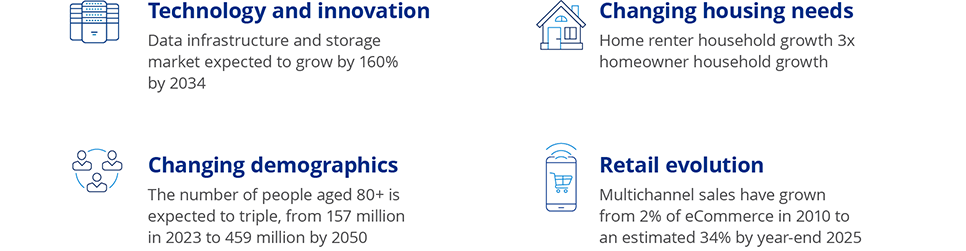

That includes secular drivers such as AI and data centers, the needs of an aging population for more senior living facilities, and the evolution and reemergence of brick-and-mortar retail.

Secular themes are driving long-term growth

At September 30, 2025. Source: Cohen & Steers, Evercore ISI.

The views and opinions are as of the date of publication and are subject to change without notice. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. There is no guarantee that any market forecast set forth in this presentation will be realized.

A favorable macroeconomic backdrop, in which growth slows and yields decline, has historically benefited commercial real estate. This is the backdrop in many markets across the globe, though notably not all, so it’s critical to embrace active management given those differences.

Recent performance reinforces our long-term view: diversification globally is essential amid diverging economic, technological, and policy cycles.

Watch September 2025 The Real Estate Reel: As private real estate bottoms, an opportunity emerges in retail

Watch all The Real Estate Reel videos.

ABOUT THE AUTHORS

Ji Zhang, CFA, Senior Vice President, is a portfolio manager for global real estate portfolios

Data quoted represents past performance, which is no guarantee of future results. The information presented does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this video will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

This video is for informational purposes and reflects prevailing conditions and our judgment as of June 2025, which are subject to change. This material should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this video to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Risks of Investing in Real Estate Securities. Risks of investing in real estate securities are similar to those associated with direct investments in real estate, including falling property values due to increasing vacancies or declining rents resulting from economic, legal, political or technological developments, lack of liquidity, limited diversification and sensitivity to certain economic factors such as interest rate changes and market recessions. Foreign securities involve special risks, including currency fluctuations, lower liquidity, political and economic uncertainties, and differences in accounting standards. Some international securities may represent small- and medium-sized companies, which may be more susceptible to price volatility and may be less liquid than larger companies. No representation or warranty is made as to the efficacy of any particular strategy or fund or the actual returns that may be achieved.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, U.S. endowments, foundations and mutual funds. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.

For investors in the Middle East: This document is for informational purposes only. It does not constitute or form part of any marketing initiative or any offer to issue or sell (or any solicitation of any offer to subscribe or purchase) any products, strategies or other services, nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this document wishes to receive further information with regard to any products, strategies or other services, it shall specifically request the same in writing from us.