Energy strategies in recent years have largely taken a binary approach to investing—either all

“traditional” or all “alternative”—leading to concentrated and potentially volatile portfolios. But there’s a growing recognition of the merits of a balanced, active strategy combining both forms.

KEY TAKEAWAYS

- Most energy investment options today limit the opportunity set to either traditional or alternative energy. We think this narrow framing is flawed.

- We believe a fundamentally driven investment strategy that reflects the reality of global energy demand and blends traditional and alternative sources can deliver improved risk- adjusted returns.

- We expect winners and losers to emerge across the energy landscape. Active management can play

a critical role by helping investors avoid structural laggards while focusing on companies best positioned to benefit from long-term energy trends.

Today’s energy landscape

Energy investors have typically been forced to take an either/or approach to investing, as the existing suite of investment strategies limits their investment choice to either traditional or alternative energy companies. We believe this is a flawed approach, a view being increasingly embraced.

A binary view does not reflect the energy future we see. Population and economic growth, and, increasingly, AI-related power needs, will drive higher global energy consumption through 2040 and beyond, even after factoring in improving energy efficiency.

To meet this growing demand, the marketplace will need every source of reliable energy it can generate. We see significant growth coming from alternative energy, but the majority of the energy supply will still come from traditional. That is why we believe the future of energy is an “energy addition” story, not an either/or choice.

You can read more on this topic in our paper: The reality of energy addition.

Many existing strategies that provide exposure to energy markets suffer from a fundamental flaw: They are designed to track either traditional energy or alternative energy benchmarks, but not both. As a result, these approaches fail to adapt to the realities of how energy is evolving.

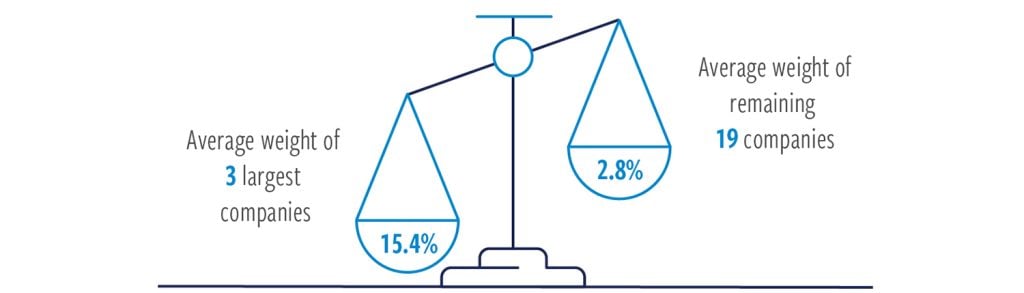

Consider the S&P Energy Select Sector Index, the largest benchmark for traditional energy. This index only offers exposure to companies focused on traditional energy, as determined by the Global Industry Classification Standard (GICS) for the sector, which is limited to energy equipment and services alongside oil, gas and consumable fuels. Further, we observe that the largest three stocks in the index make up nearly 50% of the total index by weight, and this concentration has increased from 37% in 2014. We have also seen the number of index constituents decline from 43 to 22 over the same period (Exhibit 1).

Put simply, the S&P Energy Select Sector Index is highly concentrated and only represents legacy traditional energy businesses. Though many traditional energy companies are investing capital in alternative technologies, the exposure to alternatives in the index is not representative of where we believe the energy market is headed.

EXHIBIT 1

Largest traditional index dominated by three companies

At April 30, 2026. Source: State Street Global Advisors.

By comparison, many alternative energy markets are represented by the S&P Global Clean Energy Transition Index, which serves as a benchmark for a range of strategies investors use to access the space. While we are optimistic about technological innovation and the significant growth outlook for alternative energy, we see important limitations in this universe. Clean energy equities can be highly volatile and are often sensitive to factors such as technological execution, policy support, and tax incentives—variables that can be difficult to predict. In our view,

the evolving energy system is not “all renewable,” but rather an “energy addition” model that incorporates multiple sources.

Alternative energy may offer the most compelling long-term growth within the sector, but not all technologies or business models will succeed. Unit costs, consumer preferences and tax policies can have an outsized influence on outcomes. Passive indexes cast a wide net across technologies and issuers, giving investors exposure not just to the best companies of the future, but also the structural losers—an inclusion that can weigh substantially on long-term returns.

Moreover, there are many companies participating in the value chain excluded from both benchmarks, despite providing essential services to the energy industry. Key examples include engineering & construction and uranium mining companies and other names we will target for investment when they appear attractive.

A blended approach reflects the reality of the energy future

We believe combining traditional forms of energy, such as crude oil and natural gas, with alternatives, such as wind, solar and nuclear can lead to better investment outcomes. A blended approach smooths returns as technological advancements and government policy support ebb and flow (Exhibit 2).

More specifically, we project traditional resources will generate approximately 70% of global energy supply by market share by 2036, with alternatives comprising the remaining 30%. This acknowledges that traditional energy will remain essential for decades to come, while recognizing that alternative energy plays an increasingly meaningful—and growing—role in meeting global demand.

With this in mind, we constructed a blended index consisting of 70% traditional energy and 30% alternatives. Historically, this combination generated more attractive absolute returns than either approach on its own, while also reducing annualized volatility.

In our view, a dynamic allocation across both traditional and alternative energy will maximize opportunities along the energy value chain while providing exposure to the ongoing evolution of energy markets.

While we maintain a strategic 70/30 mindset, as active managers we are tactically flexible, and will adjust our allocations based on valuations, market conditions, geopolitical risks and other factors, with a goal of achieving more attractive risk-adjusted results over time.

EXHIBIT 2

Historically higher returns, lower risk

Blended approach is poised to provide strong returns with less risk

At March 31, 2026. Source: Morningstar

Data quoted represents past performance, which is no guarantee of future results. The information presented above does not reflect the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected above. The index blend represented above is not reflective of an investment strategy employed by an active investment manager. The illustrative index blend is provided for reference purposes of historical sector level performance only. 70/30 index blend composed of 70% traditional energy (represented by S&P Energy Select Sector Index) and 30% alternative energy (represented by S&P Global Clean Energy Index). (1) Traditional Energy represented by S&P Energy Select Sector Index; (2) Alternative Energy represented by S&P Global Clean Energy Transition Index; (3) Index blend represented by 70% S&P Energy Select Sector Index and 30% S&P Global Clean Energy Transition Index.

Why active management matters

We believe investors need to redefine what constitutes the energy market—moving away from a zero-sum framework toward a broader opportunity set. A high- conviction, actively managed approach that spans both traditional and alternative companies better reflects the future of the energy system.

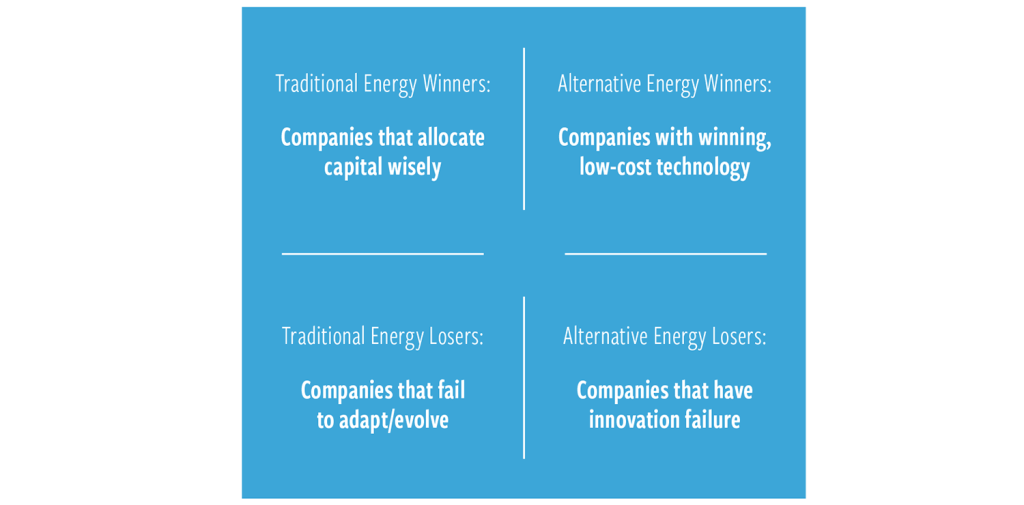

The disparity between the winners and losers within energy indexes can be great, reflecting the rapidly evolving and often misperceived energy industry. In our view, active management is better suited to navigating this dispersion—allowing investors to emphasize higher-quality companies while avoiding persistent underperformers.

Moreover, passive approaches tend to track market-capitalization-weighted indexes, meaning the largest constituents disproportionately shape performance, irrespective of underlying fundamentals.

Adopting an either/or approach, investing exclusively in traditional or alternative energy, can exclude companies benefiting from the world’s energy demands, potentially resulting in significant missed opportunities. We believe that actively allocating across the full energy value chain—spanning producers, enablers and developers shaping both traditional and alternative energy markets—can smooth and improve returns.

Winners and losers across the energy landscape

Case for active management

Index definitions / important disclosures

An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes. S&P Energy Select Sector Index seeks to provide a representation of the energy sector of the S&P 500 Index. The Index includes companies from the following industries: oil, gas and consumable fuels; and energy equipment and services. S&P Global Clean Energy Index measures the performance of 30 largest companies in global clean energy related businesses from both developed and emerging markets.

Data quoted represents past performance, which is no guarantee of future results. This material is for informational purposes and reflects prevailing conditions and our judgment as of this date, which are subject to change. There is no guarantee that any market forecast set forth in this presentation will be realized. This material represents an assessment of the market environment at a specific point in time and should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment.

This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this presentation to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Active management does not ensure a profit or guarantee to protect against a loss and actively managed strategies may underperform passively managed strategies.

Risks of Investing in Energy: Investing involves risk, including entire loss of capital invested. There can be no assurance that the investment strategy will meet its investment objectives. Diversification is not guaranteed to ensure a profit or protect against loss. The portfolio will be subject to more risks related to the energy sector than if the portfolio were more broadly diversified over numerous sectors of the economy. A downturn in the energy sector of the economy could have a larger impact on the portfolio than on an investment company that does not concentrate in the sector. Investments within the energy industry may be highly volatile due to significant