Next-generation real estate has fundamentally reshaped the REIT landscape

KEY TAKEAWAYS:

- Next-generation real estate, which includes data centers, industrial, senior housing, self storage, and newer categories such as single-family rentals and towers, now represent more than half of the REIT investing universe.

- These sectors have powerful, long run tailwinds, such as AI infrastructure, data proliferation, e commerce supply chains, and population shifts from both aging demographics and the demand drivers from the large Gen Z population.

- We believe next gen sectors (notably data centers and senior housing) are positioned for leadership given supply remains constrained, while demand is accelerating, with those tailwinds driving that demand.

Welcome to the real estate reel from Cohen & Steers.

This month, we’re focused on a shift that has fundamentally reshaped the REIT landscape over the last two decades – the rise of next generation real estate.

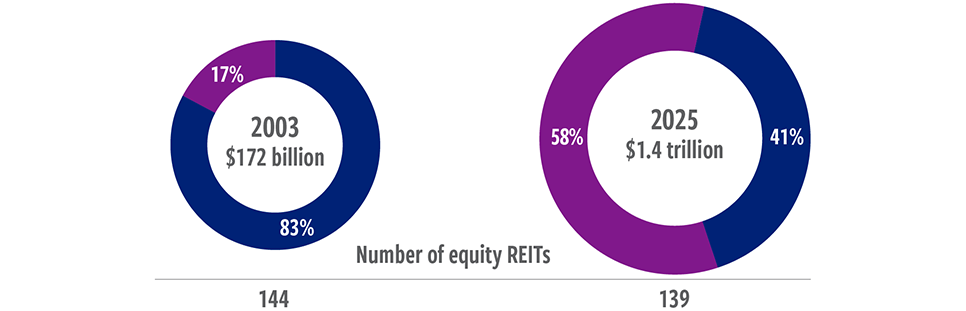

Next generation real estate (1) has driven growth of the U.S. REIT market

Twenty years ago, sectors like data centers, industrial, senior housing, self storage, and newer categories such as single-family rentals and towers were small pieces of the real estate investing universe.

Market capitalization (2)

At December 31, 2025. Source: Nareit, Factset, Cohen & Steers.

These charts are for illustrative purposes only and do not reflect information about any fund or other account managed or serviced by Cohen & Steers. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend will begin.

(1) Next-generation real estate sectors include health care, data centers, industrial, manufactured homes, self storage, single-family rental and cell tower REITs within the FTSE Nareit All Equity REITs Index.

(2) Sectors of the FTSE Nareit All Equity REITs Index. The FTSE Nareit All Equity REITs Index contains all tax-qualified REITs with more than 50% of total assets in qualifying real estate assets other than mortgages secured by real property that also meet minimum size and liquidity criteria.

These sectors, collectively referred to as next gen real estate, have expanded to more than half the market today.

And it’s not just the growth in size of next gen real estate that’s remarkable.

It’s the growth in importance of these sectors that’s also worth noting.

Today, these businesses sit at the center of the modern economy while benefiting from notable secular changes from the rise of AI, cloud computing and e-commerce to large-scale demographic shifts.

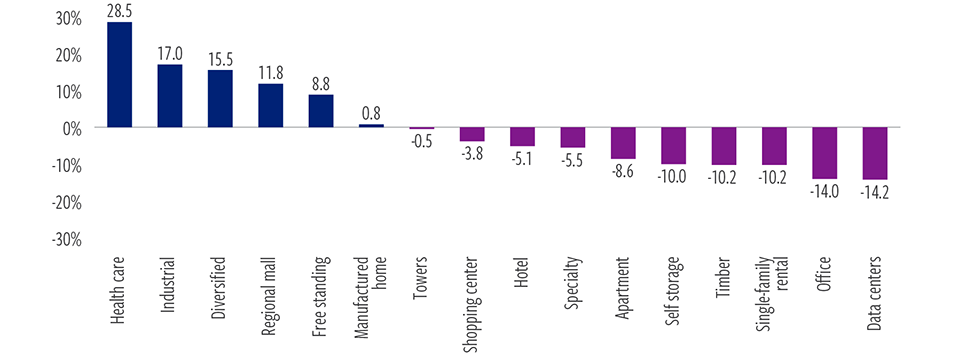

Before we look forward, it’s worth reflecting briefly on 2025.

REIT returns at the index level were modest overall at 2.3%.

Large dispersion across sectors

At December 31, 2025, unless otherwise noted. Source: Morningstar Direct and Cohen & Steers

But the year was defined by extraordinary dispersion by property type, which you can see in this chart.

The top-performing property type – health care – outperformed the worst-performing sector – data centers—by more than 40 percentage points.

I’ll touch on these two sectors in more detail in a bit.

1. The 2026 real estate outlook

First, I want to walk through why we believe that 2026 is set up to be a strong year for REITs, with both traditional and next-gen sectors playing a significant role in that set up.

Two things are happening at the same time.

First, next gen real estate has powerful, long run tailwinds, such as AI infrastructure, data proliferation, e commerce supply chains, and population shifts from both aging demographics and the demand drivers from the large Gen Z population.

Those dynamics are not cyclical; they’re structural.

Second, the broader real estate environment entering 2026 is turning increasingly supportive.

Our firm is above consensus expectations for economic growth and inflation, and are calling for stable interest rates.

Combined with a more accommodative monetary policy, these conditions have historically favored real estate.

And as we touched on in our December Reel, valuations have reset and liquidity needs are driving greater listed allocations.

We also expect economic activity and market returns to broaden after several years of highly concentrated gains, moving away from the so-called K-shaped recovery that favored only certain stocks to a broader recovery that, among other allocations, will favor real estate

But let’s focus on next gen real estate.

Overall, as investors, we favor assets that have strong secular growth profiles and good pricing power.

It’s these same attributes that have driven the rapid growth of next-gen real estate for a couple of decades now, which I mentioned earlier.

This year, we believe next‑gen sectors continue to be positioned for leadership.

Supply remains constrained for many of these property types, while demand is accelerating, with key trends driving that demand:

Two sectors stand out: data centers and senior housing.

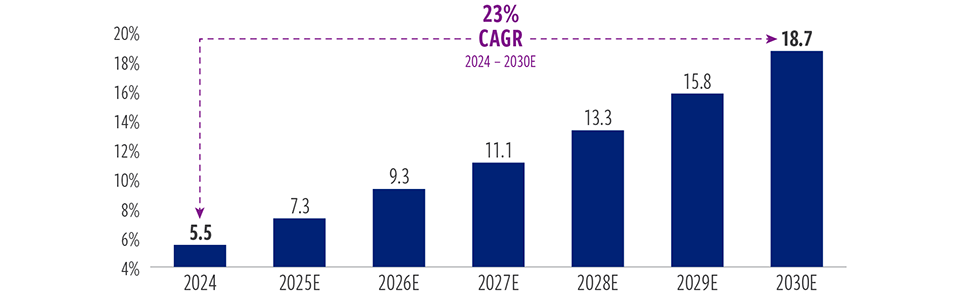

2. Data Centers

Data centers underperformed in 2025 despite massive AI-driven capital expenditure by large tech companies.

Investors preferred direct tech stocks over data center REITs as they looked to invest in the AI trend.

Deep seek concerns hit the market first, then a key tech firm paused new leasing… and several operators ran out of available power capacity, creating short term questions about the sector.

But the underlying trend hasn’t changed.

Data centers: AI innovation driving demand growth, attractive relative value

Global AI data center demand (Gw)

2024-2030E

At June 30, 2025. Source: Bloomberg, Altman Solon, and Cohen & Steers

If anything, it’s strengthened amid the underperformance last year.

AI related data demand is projected to grow more than 20% annually through 2030.

Rents continue to rise. Development margins remain healthy.And REITs have been deploying capital into power‑constrained, high‑value markets where pricing power is strongest.

Yes, month‑to‑month headlines may fluctuate, but the fundamentals remain one of the most attractive secular growth stories in global real estate.

3. Senior housing

That imbalance of surging demand and limited supply is driving higher occupancy and improved rent growth.

Senior housing operators are consolidating, cost pressures are easing, and the sector is experiencing its most sustained recovery in years.

Put simply: both the demographic math and the competitive dynamics are improving.

The main risk is future supply growth if construction costs fall or new entrants emerge.

But new supply will take time to have an impact. In the meantime, we will several more years of baby boomers turning 80.

So when you combine the favorable 2026 environment for real estate overall

… with the powerful secular growth behind next generation sectors

… and a 2025 reset that has created clear valuation and performance dispersion…

you get one of the most supportive backdrops for real estate investing that we’ve seen in years.

Watch December 2025 The Real Estate Reel: Three data points driving our 2026 real estate outlook

Watch all The Real Estate Reel videos.

ABOUT THE AUTHORS

Seth Laughlin, Senior Vice President, is Head of Real Estate Strategy & Research, responsible for identifying allocation opportunities in both listed and private real estate and related thematic and strategic research.

Data quoted represents past performance, which is no guarantee of future results. The information presented does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this video will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

This video is for informational purposes and reflects prevailing conditions and our judgment as of June 2025, which are subject to change. This material should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this video to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Risks of Investing in Private Real Estate

Private real estate investments are illiquid and susceptible to economic slowdowns or recessions and industry cycles, which could lead to financial losses and a decrease in revenues, net income and assets. Lack of liquidity in the private real estate market makes valuing underlying assets difficult. Appraisal values may vary substantially from a price at which an investment in real estate may actually be sold.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, U.S. endowments, foundations and mutual funds. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.