Real estate has lagged listed equities in 2025, and 2026 offers a reprieve on multiple fronts.

Key takeaways:

- Real estate has lagged listed equities for the year, and 2026 offers a reprieve on multiple fronts. We do expect listed real estate to outperform private given listed has access to higher growth property types.

- Delinquencies may rise as a result of aggressively underwritten deals in the last cycle, but increased real estate transaction volumes should limit a wide impact on the market and overall valuations.

- Apartments have the highest gap between public and private valuations in commercial real estate, which we believe will drive cap rates higher and values lower for private apartment properties.

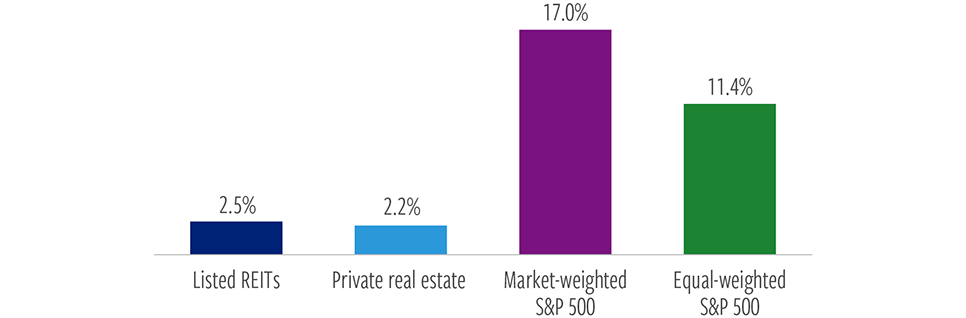

With less than 10 days of trading left in 2025, real estate has lagged listed equities for the year, with REITs returning 2.5% vs. the S&P 500, which was up 17%.

Real estate lagged listed equity markets in 2025

Year-to-Date performance

At December 16, 2025. ODCE net returns as of September 30, 2025. Listed REIT returns represented by FTSE Nareit All Equity REITs Index. Private real estate represented by NCREIF Value-Weighted Fund Index – Open-end Diversified Core Equity Index (NFI-ODCE). Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might emerge.

Private market returns (as represented by the NFI-ODCE Value Weighted Index) of 2.2% were below the 25-year average of 5.2% through the third quarter of this year.

Notably, however, when we look back, we can see that private real estate bottomed in the third quarter of last year.

The ten rate hikes that began in 2022 were compounded by the degree with which the move was driven by real rates vs. inflation expectations.

At the same time, strong post-pandemic rent growth drove elevated supply.

The result: Listed real estate had a peak-to-trough decline of 33% and private was down 20%.

This year’s returns since those bottoms have been positive but modest.

2026 offers a reprieve on multiple fronts.

As investors look to a new year, there are three key themes we are focused on.

Improving credit availability. Why we believe listed real estate is likely to outperform private. And one sector where we see notable price dislocation between listed and private markets.

1. Credit availability

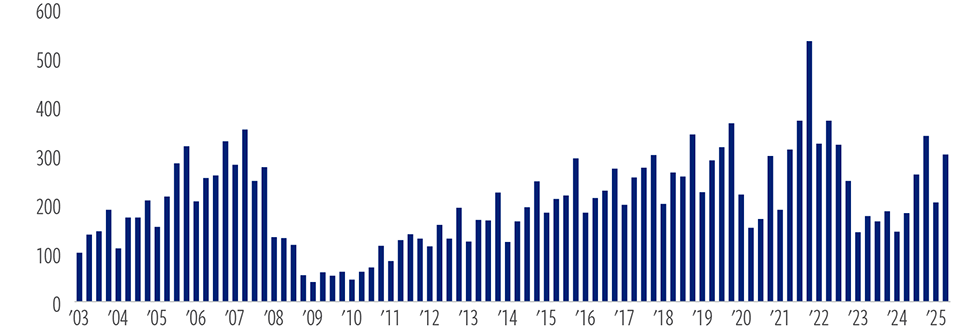

First, credit availability.

Credit availability has started to improve

CRE debt origination volume index by quarter (2001 Avg Q = 100)

At June 30, 2025. Source: Mortgage Bankes Association. Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin.

After spending the last two years digesting the impact of the Fed hiking cycle on their loan books, banks have begun to reenter the CRE debt markets.

During their absence, life insurance companies and the CMBS market stepped in, which should also continue to grow.

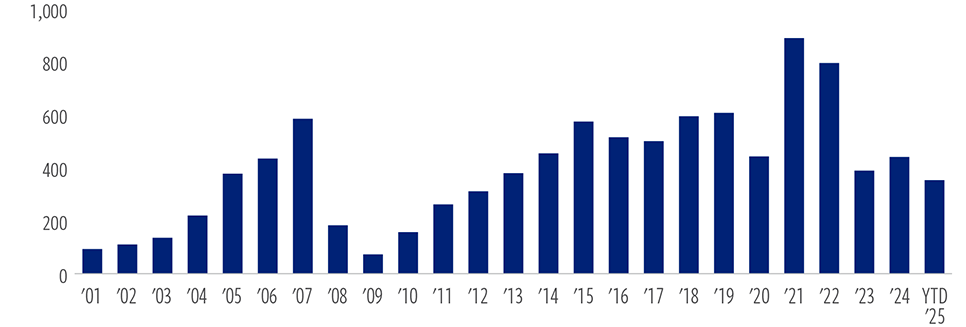

Transaction volume expected to grow for third consecutive year

CRE Transaction Volumes ($B) (As of Q325)

At November 18, 2025. Source: MSCI. Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin.

Given the combination of debt availability and idle capital that has been raised but not deployed, we expect ’26 transaction volumes to grow for the third consecutive year.

Delinquencies, as a result of aggressively underwritten deals in the last cycle, will likely accelerate particularly in office, but given the capital willing to step in, we do not see a wider impact on the market and overall valuations.

2. 2026 forecasts

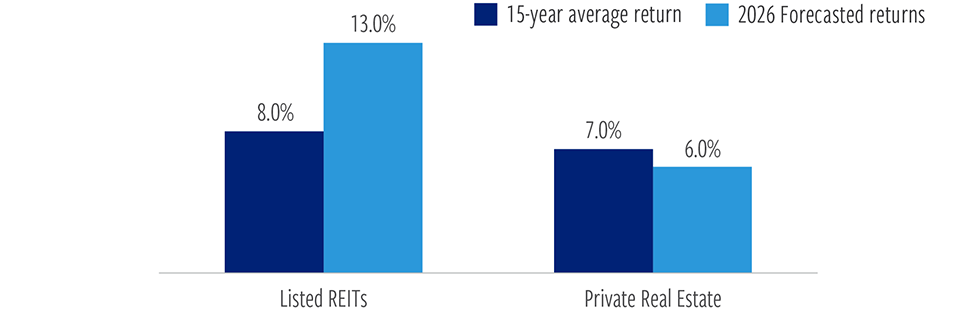

The second theme: We forecast listed REITs to return lower to mid-double digits at the index level in ’26 after a lackluster 2.0% in ’25.

Listed real estate expected to outperform private in 2026

Historical and forecasted returns

At June 30, 2025. Source: Cohen & Steers, Evercore ISI. Listed REIT returns represented by FTSE Nareit All Equity REITs Index. Private real estate represented by NCREIF Fund Index – Open-end Diversified Core Equity Index (NFI-ODCE). The views and opinions are as of the date of publication and are subject to change without notice. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin. There is no guarantee that any market forecast set forth in this presentation will be realized.

This compares to our forecast of mid single-digit returns in the ODCE index, which is more exposed to apartments and industrial sectors, which we believe are less likely to accelerate from here compared to other property types.

Listed real estate provides access to higher growth property types vs. the NCREIF index. This includes senior housing, towers and data centers.

At the same time, despite the market’s forecast for additional rate cuts in ‘26, we expect 10-year yields to remain close to current levels or slightly higher, reducing the potential for cap rate compression.

2026 will see a similar trend of muted asset value growth and income driving a significant portion of returns in the private market.

As is often the case, the listed market was earlier to price higher debt costs and are set to see earnings growth reaccelerate next year.

3. Valuation gap in apartments

Finally, we see a gap between public and private valuations in commercial real estate.

Perhaps the largest is in the apartment sector, which we believe will drive cap rates higher and values lower for private apartment properties.

The listed sector has traded at sizable discounts to gross asset value for the better part of the last two years.

Higher cap rates expected for apartments

Applied vs implied apartment nominal cap rate

At December 1, 2025. Source: Green Street. Data quoted represents past performance, which is no guarantee of future results. The information presented above does not represent the performance of any fund or other account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance listed above. There is no guarantee that any historical trend illustrated above will be repeated in the future, and there is no way to predict precisely when such a trend might begin.

Bulls on the sector are hopeful that once record levels of supply subside, internal growth rates will reaccelerate above long-term averages.

The cost of homeownership and slowing supply are undeniable positives for operating fundamentals, but we believe those benefits are priced in.

We expect more pedestrian growth as the renter-age demographic shrinks and recent graduate unemployment reduces demand, a weaker job growth forecast will also weigh on landlord pricing power.

However, chasing last cycle’s winners is a common practice, but as ’26 shows weaker than expected demand and fundamentals that disappoint, cap rates should rise and values should decline as the year progresses, which has already been reflected in the listed market.

Watch November 2025 The Real Estate Reel: Three big trends driving real estate investing returns today

Watch all The Real Estate Reel videos.

ABOUT THE AUTHORS

Seth Laughlin, Senior Vice President, is Head of Real Estate Strategy & Research, responsible for identifying allocation opportunities in both listed and private real estate and related thematic and strategic research.

Data quoted represents past performance, which is no guarantee of future results. The information presented does not reflect the performance of any fund or account managed or serviced by Cohen & Steers, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this video will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

This video is for informational purposes and reflects prevailing conditions and our judgment as of June 2025, which are subject to change. This material should not be relied upon as investment advice, does not constitute a recommendation to buy or sell a security or other investment and is not intended to predict or depict performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or take into account the specific objectives or circumstances of any investor. We consider the information in this video to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment. Please consult with your investment, tax or legal professional regarding your individual circumstances prior to investing.

Risks of Investing in Private Real Estate

Private real estate investments are illiquid and susceptible to economic slowdowns or recessions and industry cycles, which could lead to financial losses and a decrease in revenues, net income and assets. Lack of liquidity in the private real estate market makes valuing underlying assets difficult. Appraisal values may vary substantially from a price at which an investment in real estate may actually be sold.

Cohen & Steers Capital Management, Inc. (Cohen & Steers) is a U.S. registered investment advisory firm that provides investment management services to corporate retirement, public and union retirement plans, U.S. endowments, foundations and mutual funds. Cohen & Steers UK Limited is authorized and regulated by the Financial Conduct Authority (FRN458459). Cohen & Steers Asia Limited is authorized and regulated by the Securities and Futures Commission of Hong Kong (ALZ367). Cohen & Steers Japan Limited is a registered financial instruments operator (investment advisory and agency business and discretionary investment management business with the Financial Services Agency of Japan and the Kanto Local Finance Bureau No. 3157) and is a member of the Japan Investment Advisers Association. Cohen & Steers Ireland Limited is regulated by the Central Bank of Ireland (No.C188319). Cohen & Steers Singapore Private Limited is a private company limited by shares in the Republic of Singapore.